Introduction: Why Wealth Transfer Planning Can't Wait

Imagine spending 30 years building a manufacturing company worth $8 million — only to have your heirs face a $2 million estate tax bill due within nine months of your death, no liquid assets to pay it, and three children who disagree about whether to sell. The business gets auctioned off below market value. The family fractures. The legacy disappears.

This isn't a rare scenario. According to the Family Business Association, only about 30% of family businesses survive to the second generation, 12% reach the third, and just 3% make it to the fourth. Poor planning — or no planning at all — is the common thread.

The good news: these outcomes are largely preventable. This guide walks through the specific challenges business owners face, the strategies that address them, and how to build a coordinated plan that protects both your business and your family's financial future.

Key Takeaways

- 80–90% of a business owner's wealth is typically tied to the business — making concentration risk a serious planning problem

- Estate taxes of up to 40% apply above the federal exemption, with payment due nine months after death

- Five core documents underpin every plan: revocable trust, buy-sell agreement, power of attorney, will, and survivor income strategy

- Gifting strategies, IDGTs, and GRATs can reduce transfer taxes significantly — but acting before the 2025 exemption sunset closes a major window

- Wealth transfer requires a coordinated advisory team — financial planner, estate attorney, and CPA each handle distinct pieces

Why Business Owners Face Unique Wealth Transfer Challenges

Most financial planning challenges can be addressed with time and discipline. Business owners face a different category of problem — one where the planning failure and the financial consequence happen simultaneously.

The Concentration Risk Problem

The Exit Planning Institute reports that 80–90% of a business owner's net worth is typically tied up in the value of the business itself. That means a single adverse event — death, disability, a key customer departure — can destroy personal wealth and business value at the same time.

Unlike a stock portfolio, there's no diversification buffer and no way to trim positions when conditions shift.

The Liquidity Gap

Unlike a stock portfolio, a private business cannot be sold in a week. Yet the IRS requires Form 706 and any estate tax payment within nine months of the date of death. An estate holding $10 million in illiquid business interests may face a tax bill with no obvious way to pay it — short of a forced sale at an unfavorable price.

The Estate Tax Exposure

The federal estate tax hits hard above the exemption threshold. For 2025, the IRS sets the basic exclusion amount at $13.99 million per individual, with a top marginal rate of 40% on the taxable portion. A business worth $20 million, combined with other assets, can push an estate well into taxable territory — creating a multi-million dollar obligation the family may not be prepared for.

The Family Dynamics Problem

Many owners assume heirs want the business, or that children will divide it without conflict. Neither assumption tends to hold. The Kreischer Miller 2022 Family Business Survey found that 45.9% of surveyed family-owned companies had no management succession plan — and identified family dynamics and people issues as a leading barrier to planning.

When intentions go undisclosed and expectations diverge, the business itself can fail at the moment of transition.

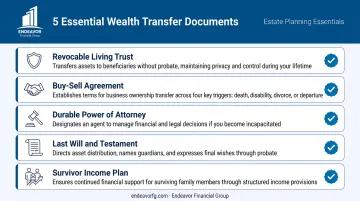

The Foundation: Essential Wealth Transfer Documents Every Business Owner Needs

Most wealth transfer strategies fail not because of bad intentions — but because the paperwork wasn't in order. These five documents form the legal backbone of any solid plan.

Revocable Living Trust

A revocable trust holds legal title to business interests and personal assets during the owner's lifetime. The owner retains full control and can modify it at any time. At death, assets transfer directly to named beneficiaries — privately, without going through probate.

For business owners, this means continuity. A successor trustee can step in and manage or transfer business interests immediately, without waiting for a court process that can drag on for months.

Buy-Sell Agreement

This is a legally binding contract that determines what happens to an owner's business interest when a triggering event occurs — death, disability, retirement, or divorce. A well-drafted agreement covers four key elements:

- Which circumstances activate the agreement (death, disability, divorce, retirement)

- How the business will be valued — fixed price, formula, or independent appraisal

- How the buyout will be paid — lump sum, installments, or a combination

- How the purchase is funded, most commonly through life insurance on each owner

Without a buy-sell agreement, a deceased owner's interest may pass to a spouse or children who have no role in the business — and no obligation to sell at a fair price.

Durable Financial Power of Attorney

This document authorizes a trusted individual to manage both personal and business affairs if the owner becomes incapacitated. That includes voting shares, executing contracts, accessing business accounts, and signing agreements on the owner's behalf.

Without it, a court must appoint a guardian — a process that can take months and leave the business in limbo.

Last Will and Testament

A will directs asset distribution and names executors — useful, but limited for business owners in three specific ways:

- It does not override beneficiary designations on retirement accounts or life insurance

- It does not govern jointly held assets

- It is subject to public probate, which delays transfer and exposes the estate to challenges

A will should work alongside a trust, not replace it. Together, they cover both what probate touches and what it doesn't.

Survivor Income Planning

When a business owner dies, the paycheck stops. This is one of the most overlooked gaps in estate planning. Three approaches address it directly:

- Earmarking life insurance proceeds specifically for income replacement

- Establishing deferred compensation plans payable to a surviving spouse

- Creating a written dividend policy so the business continues generating cash flow for the family

Transferring the business without addressing the surviving spouse's income leaves a critical gap — one that no amount of legal documentation can fix after the fact.

Key Strategies to Transfer Your Business to the Next Generation

There's no single "right" way to transfer a business. The best approach depends on the owner's goals, family situation, and how much tax exposure needs to be managed.

Transferring Through Your Estate Plan

The simplest option: include the business in a revocable trust or will, specify who inherits, and outline whether the business should be continued or sold. Heirs who later sell receive a stepped-up cost basis at death, resetting the asset's tax basis to fair market value and potentially eliminating capital gains taxes on decades of appreciation.

The key risk: if the estate is subject to estate tax and lacks liquidity, the business may need to be sold to pay the bill. Pre-arranging liquidity through life insurance or a line of credit is essential for illiquid estates.

Direct Gifting of Business Interests

Owners can gift portions of the business — directly or into an irrevocable trust — to remove value from the taxable estate over time.

Current gifting thresholds (from the IRS):

- 2025 annual gift tax exclusion: $19,000 per recipient

- 2025 lifetime gift and estate tax exemption: $13.99 million per individual

Gifting minority interests or non-voting shares creates an additional advantage: valuation discounts. Because minority stakes lack control and are difficult to sell, the IRS recognizes discounts for lack of marketability (DLOM) and lack of control, potentially reducing the reported gift value by 15–35% compared to the pro-rata business value.

Installment Sale to Family

Rather than gifting, the owner sells the business (or interests in it) to a family member or trust in exchange for a promissory note. Done correctly, the structure:

- Creates a steady income stream for the seller's retirement

- Freezes the business's current value in the estate

- Transfers all future appreciation to the buyer tax-free

The interest rate on the note must meet IRS minimum requirements, but when structured correctly, this strategy can shift significant wealth with minimal gift or estate tax consequences.

Advanced Trust Strategies: IDGTs and GRATs

For high-growth businesses, two trust structures stand out when the goal is moving future appreciation out of the taxable estate.

| Strategy | How It Works | Key Advantage |

|---|---|---|

| IDGT (Intentionally Defective Grantor Trust) | Owner sells or gifts interests into the trust; continues paying income taxes on trust earnings | Tax payments reduce the owner's estate without counting as additional gifts |

| GRAT (Grantor Retained Annuity Trust) | Owner transfers interests, receives fixed annuity payments for a set term | Appreciation above the IRS Section 7520 hurdle rate (5.0% for June 2025) passes to beneficiaries gift-tax-free |

Both strategies work best when the business is expected to grow faster than the hurdle rate. A zeroed-out GRAT — structured so annuity payments return the full transfer value — can also eliminate gift tax risk entirely if the business underperforms.

Minimizing Estate and Gift Taxes: Tools for Business Owners

Transferring a business efficiently requires more than just choosing the right structure. Tax minimization tools should be layered into the plan.

Irrevocable Life Insurance Trusts (ILITs)

Life insurance held inside an ILIT is excluded from the insured's taxable estate. The death benefit becomes available immediately, providing liquidity to:

- Pay estate taxes without a forced business sale

- Fund a buy-sell agreement buyout

- Equalize inheritances when one heir receives the business and others receive cash

An ILIT is one of the most practical tools for solving the liquidity gap problem that threatens so many business estates.

Spousal Lifetime Access Trusts (SLATs)

A SLAT allows a married business owner to gift assets — including business interests — into a trust for the spouse's benefit. This removes the assets and their future growth from the taxable estate while the spouse retains access to trust distributions.

Both strategies work best when implemented before your business grows further in value — which makes the current exemption landscape especially relevant.

Act Before Exemptions Change

The 2017 Tax Cuts and Jobs Act temporarily doubled exemption levels. While P.L. 119-21 has set the 2026 basic exclusion amount at $15 million, future legislative changes remain a real possibility. Business owners with estates approaching or exceeding that threshold should review their plans now. Gifting and trust strategies lose effectiveness as valuations rise, so earlier action preserves more of the estate.

Aligning Wealth Transfer with Business Succession Planning

Estate planning and succession planning are related but distinct. Estate planning governs what happens to business assets when the owner dies or becomes incapacitated. Succession planning determines who will run the business and how the transition unfolds. When the two aren't coordinated, the result can be conflicting instructions — an estate distributing ownership to heirs who have no plan for running or exiting the business.

The Active vs. Inactive Heir Problem

When some children work in the business and others don't, equal ownership distribution rarely produces equal outcomes. The child running daily operations has fundamentally different needs than a sibling collecting passive distributions — and that tension can surface quickly, with non-operating heirs pushing for buyouts or dividends the business can't easily support. Common solutions include:

- Creating separate share classes (voting vs. non-voting)

- Using life insurance to provide equivalent value to non-business heirs

- Separating economic ownership from management control entirely

Keep Documents Current

A buy-sell agreement drafted at business formation may list a valuation method that no longer reflects reality, reference a former business partner, or fail to account for a new co-owner. The same applies to trusts and powers of attorney. Plan to review all documents at least every three to five years, and immediately after any of these events:

- A new business partner joins or departs

- A divorce or remarriage in the ownership group

- A significant shift in business value

- A death in the family

Building Your Wealth Transfer Team

Wealth transfer planning for business owners isn't a single-advisor job. The complexity requires coordinated expertise across legal, tax, and financial domains.

The Core Advisory Team

| Role | Primary Responsibility |

|---|---|

| Estate attorney | Drafts and updates legal documents (trusts, wills, buy-sell) |

| CPA / tax advisor | Models tax scenarios, structures transitions for efficiency |

| Financial planner | Coordinates overall strategy, integrates all components |

The financial planner acts as the integrating force. That means ensuring the estate attorney's documents align with the tax advisor's recommendations, that business succession logistics match what the estate plan describes, and that the investment and retirement income strategy supports the overall transfer goals.

How Endeavor Financial Group Approaches This

Endeavor Financial Group's structured five-step planning process, from initial discovery through ongoing support and monitoring, is designed for exactly this kind of coordinated, multi-layered work. Eric Bilitz and the team serve business owners across Indiana as a core client segment, and their fee-only fiduciary model means product commissions never influence their recommendations.

Where a typical asset manager handles investments in isolation, Endeavor integrates wealth transfer, business succession, tax strategy, and retirement income into a single coherent roadmap. The firm coordinates directly with estate attorneys and CPAs, acting as the quarterback that keeps the overall plan on track and flags when documents need updating as circumstances change.

For business owners ready to start the conversation, Endeavor offers a complimentary initial consultation.

Frequently Asked Questions

When should a business owner start wealth transfer planning?

Start as soon as the business reaches meaningful value — typically $1 million or more. Strategies like GRATs, gifting programs, and IDGTs lose effectiveness as the business grows in value or as the owner ages, so earlier action preserves the most options.

What is the difference between estate planning and succession planning for a business owner?

Estate planning governs the legal transfer of ownership and assets at death or incapacity. Succession planning determines who manages and operates the business going forward. Both must be coordinated — a gap between them is the most common cause of failed business transitions.

How can I transfer my business to my children without triggering a large tax bill?

Gifting minority interests with valuation discounts, using IDGTs or GRATs, and making full use of lifetime gift tax exemptions can significantly reduce transfer taxes. The right combination depends on the business's structure, current value, and the owner's retirement income needs.

What happens to my business if I die without a wealth transfer plan?

Without a plan, state intestacy laws determine who inherits, probate delays the transfer, and a large estate tax bill may arrive with no liquidity to pay it. The most common outcome is a forced sale under unfavorable conditions — often far below market value.

How does a buy-sell agreement protect my family and business partners?

It pre-establishes who can buy an owner's interest, at what price, and under what conditions. Typically funded with life insurance, this gives surviving owners immediate cash to complete the purchase — preventing outside parties from inheriting a stake and providing everyone a clear, predictable exit.

Do wealth transfer strategies apply to smaller businesses?

Any business with meaningful value — and any family that depends on it for income or retirement security — benefits from a transfer plan. The tools scale to any size, and a $3 million business faces the same forced-sale risk as a $30 million one if no plan is in place.