The core fear for many is simple: outliving their savings. You need a reliable income stream you can count on, but building one in today's environment requires a more dynamic and strategic approach. This guide will walk you through creating a resilient retirement income strategy for 2026, from optimizing Social Security to building a tax-efficient withdrawal plan.

TL;DR: Your 2026 Retirement Income Checklist

- Maximize guaranteed income: Carefully time your Social Security benefits to capitalize on the 2.8% COLA for 2026.

- Adopt a dynamic withdrawal strategy: Use a method like the bucket strategy to protect your portfolio from market volatility.

- Proactively manage major expenses: Plan for 2026 Medicare premium changes and explore tax-advantaged savings for long-term care.

- Review your asset allocation: Ensure your portfolio aligns with your risk tolerance in the current economic climate.

- Consult a professional: Work with a financial advisor to build a personalized plan that adapts to the unique challenges of 2026.

The Retirement Landscape in 2026: What's New and What It Means for You

Retirement planning for 2026 requires a clear understanding of the economic factors at play. Persistent inflation, while moderating, continues to be a major concern. In fact, a 2025 survey from EBRI/Greenwald found that 53% of retirees were worried they would have to make substantial cuts to their spending due to inflation.

This economic pressure makes it more important than ever to take advantage of opportunities to boost your savings. The IRS has announced updated contribution limits for 2026, allowing you to maximize contributions to your retirement accounts.

2026 Retirement Account Contribution Limits:

- 401(k), 403(b), and TSP: The employee contribution limit is $24,500.

- IRA (Traditional & Roth): The annual contribution limit is $7,500.

- 401(k) Catch-Up (Age 50+): An additional $8,000 for those 50 or older.

- IRA Catch-Up (Age 50+): An additional $1,100 for those 50 or older.

Beyond higher contribution limits, the SECURE 2.0 Act introduced a new provision effective after December 29, 2025. You can now take a penalty-free withdrawal of up to $2,600 from your retirement plan to pay for long-term care insurance premiums, offering a new way to manage future healthcare costs.

Foundational Income Sources: Maximizing Social Security and Pensions in 2026

Your guaranteed income sources are the bedrock of your retirement plan. They provide a predictable monthly "paycheck" that isn't subject to market swings.

Optimizing Your Social Security Benefits

When you claim Social Security is one of the most significant financial decisions you'll make. The timing affects your monthly benefit for the rest of your life.

- Claiming Early (Age 62): You receive a smaller check but get payments for a longer period.

- Claiming at Full Retirement Age (FRA): You receive your full, standard benefit. Your FRA is between 66 and 67, depending on your birth year.

- Delaying (Age 70): Your benefit increases by about 8% for each year you wait past your FRA, maxing out at age 70. This provides the largest possible monthly check.

While official numbers are released annually, the 2026 Cost-of-Living Adjustment (COLA) is projected to be around 2.8%. This adjustment helps your benefits keep pace with inflation.

If you plan to work while receiving benefits before your full retirement age (FRA), be aware of the annual earnings test. For 2026, the income limit is estimated to be $24,480. Your benefits will be reduced by $1 for every $2 you earn above that amount.

The limit increases significantly in the year you reach FRA, projected at $65,160, with a gentler $1 for $3 reduction. This rule only applies to earnings in the months before your birthday. Once you reach FRA, the earnings limit is removed entirely.

The Role of Pensions and Annuities

If you are fortunate enough to have a pension, it provides another layer of stable income. Before you retire, review your payout options carefully. A "single life" option provides a larger monthly payment, but a "joint and survivor" option ensures your spouse continues to receive income after you pass away.

For those without a pension, an annuity can serve a similar purpose. By converting a portion of your savings into a contract with an insurance company, you can create your own personal pension that guarantees income for life.

Building Your Distribution Plan: Smart Withdrawal Strategies for 2026

Once your foundational income is set, the next step is determining how to draw from your investment portfolio. This is where a smart withdrawal strategy becomes critical.

Moving Beyond the 4% Rule

The 4% rule—withdrawing 4% of your portfolio in the first year of retirement and adjusting for inflation annually—has long been a popular guideline. However, higher inflation and volatile market forecasts are challenging its reliability for new retirees.

Modern research suggests a more flexible approach is needed. For instance, Morningstar's latest analysis projects a highest safe starting withdrawal rate of 3.9% for 2026, assuming a 30-year retirement. Other strategies, like a "guardrails" approach that adjusts withdrawals up or down based on portfolio performance, are gaining traction.

These modern strategies require ongoing adjustments, which is why many retirees work with a financial advisor to create a personalized distribution plan that adapts to changing market conditions.

Implementing a Bucket Strategy for Income Stability

The bucket strategy is a practical method for structuring your assets to provide income while protecting your portfolio from market downturns. It involves dividing your money into three distinct pools.

- Bucket 1 (Short-Term: 1-2 years): This bucket holds cash and cash equivalents (like a high-yield savings account) to cover your immediate living expenses. You can draw from this fund without worrying about selling investments in a down market.

- Bucket 2 (Mid-Term: 3-7 years): This bucket contains more conservative investments, such as bonds and low-volatility funds. Its purpose is to periodically refill Bucket 1.

- Bucket 3 (Long-Term: 8+ years): This is your growth engine. It holds the rest of your portfolio in assets like stocks and ETFs, designed to outpace inflation and ensure your money lasts.

Navigating Required Minimum Distributions (RMDs)

Once you reach age 73, the IRS requires you to start taking Required Minimum Distributions (RMDs) from your tax-deferred retirement accounts (like traditional 401(k)s and IRAs). Failing to take your RMD can result in a steep penalty.

If you don't need the RMD for living expenses, you can reinvest it in a taxable brokerage account. Another popular strategy is the Qualified Charitable Distribution (QCD), which allows you to donate your RMD (up to a certain limit) directly to a charity. This strategy not only satisfies your RMD requirement but also allows you to support a cause you care about while potentially lowering your taxable income.

Reviewing Your Investment Mix for a Changing Market

Your asset allocation—the mix of stocks, bonds, and cash in your portfolio—should evolve as you approach and enter retirement. A common guideline is the "Rule of 110," where you subtract your age from 110 to find a suggested stock allocation. For a 65-year-old, this would suggest a 45% allocation to stocks.

However, it's crucial to avoid being too conservative. With inflation, a portfolio heavily weighted toward cash and fixed-income assets can lose purchasing power over time. You still need growth to ensure your money lasts for a 20- or 30-year retirement.

This is especially important for mitigating sequence of returns risk—the danger of experiencing poor market returns in the first few years of retirement. Withdrawing money from a declining portfolio can permanently damage its long-term potential.

Your best defenses against this risk include:

- A well-designed "bucket" strategy to segment your funds

- A balanced asset allocation that can adapt to market conditions

Shielding Your Wealth: Navigating Taxes, Healthcare, and Inflation

Managing your income is only half the battle; protecting it from taxes, healthcare costs, and inflation is just as important.

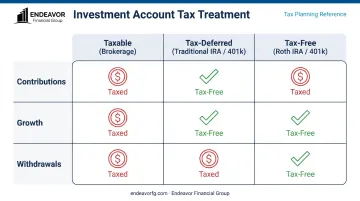

Proactive Tax Planning for Retirement Income

A key to tax efficiency in retirement is having savings in different types of accounts:

- Taxable: Brokerage accounts.

- Tax-Deferred: Traditional 401(k)s and IRAs.

- Tax-Free: Roth 401(k)s and Roth IRAs.

This diversification gives you flexibility. For example, you might withdraw from taxable accounts first, allowing your tax-deferred funds to continue growing. You could also consider a Roth conversion in 2026, especially if it's a lower-income year for you. This involves paying taxes on the converted amount now to create a source of tax-free income for the future.

While managing taxes is a critical part of preserving your wealth, healthcare costs represent another major financial hurdle in retirement.

Managing Healthcare and Long-Term Care Costs

Healthcare is one of the largest and most unpredictable expenses in retirement. For 2026, the standard Medicare Part B monthly premium is set to rise to $202.90, and the annual deductible will be $283.

But that's just the beginning. According to Fidelity's 2025 Retiree Health Care Cost Estimate, an average 65-year-old couple may need $345,000 after tax to cover healthcare expenses in retirement—and this figure doesn't even include long-term care. Integrating tools like Health Savings Accounts (HSAs) and Long-Term Care (LTC) insurance into a cohesive financial plan is essential for managing these significant costs.

Why a Personalized Plan Matters More Than Ever in 2026

The complexities of the 2026 retirement landscape make a generic, DIY approach risky. A simple asset manager might help you with investments, but they often can't provide the holistic guidance needed to navigate taxes, healthcare, Social Security, and RMDs in a coordinated way.

This is where comprehensive financial planning provides a clear roadmap. At Endeavor Financial Group, we specialize in creating personalized, strategic wealth plans for pre-retirees and small business owners.

As fiduciaries, we are legally obligated to act in your best interest. Our consultative, team-based approach ensures every part of your financial life—from investments to tax strategy—is working together.

We achieve this through a structured process designed to give you clarity and confidence. Our goal is to build a plan that not only addresses today's challenges but also adapts to future market shifts and personal milestones.

Frequently Asked Questions

What retirement rules are changing for 2026?

Key changes include updated contribution limits for 401(k)s ($24,500) and IRAs ($7,500), the 2.8% Social Security COLA, and a new SECURE 2.0 provision allowing penalty-free withdrawals for LTC insurance premiums.

How is Social Security going to be taxed in 2026?

Up to 85% of Social Security benefits are federally taxable based on your "combined income." Since the income thresholds ($25k single, $32k joint) don't adjust for inflation, more retirees face this tax each year.

Is 2026 going to be a good year to retire?

The "right" year depends on your personal financial readiness, not just market conditions. While 2026 presents challenges like inflation, a solid, flexible income plan can make any year a good year to retire with confidence.

What is a safe withdrawal rate for my retirement savings in 2026?

The classic 4% rule is being revised, with many experts suggesting a more flexible or lower rate around 3.9%. Your ideal rate is personal and must account for your portfolio, spending needs, and expected longevity.

How can I protect my retirement portfolio from inflation and market volatility?

Employ a bucket strategy to avoid selling assets during downturns and consider inflation-resistant investments like TIPS, real estate, and certain equities. A balanced asset allocation remains your best long-term defense.