The high-income potential of the medical profession comes with a significant tax burden. Without a proactive strategy, taxes can erode your ability to build wealth, pay off debt, and retire comfortably. This guide provides a clear, actionable roadmap for tax planning and retirement strategies specifically for physicians—whether you're an employee, practice owner, or independent contractor.

TL;DR: Key Tax Strategies for Physicians

- Maximize Retirement Accounts: Fully fund your 401(k), 403(b), and 457(b) if employed. Practice owners should use a Solo 401(k) or SEP IRA.

- Use Advanced Plans: High-earners can use Cash Balance Plans to contribute and deduct an additional six figures annually.

- Leverage HSAs: A Health Savings Account offers a triple-tax advantage and can function as a "stealth IRA" for medical costs in retirement.

- Optimize Your Business Structure: Practice owners can use an S-Corp election to reduce self-employment taxes on distributions.

- Integrate Your Financial Team: The most effective strategy involves your financial planner and CPA working together to align tax decisions with long-term goals.

Why Tax Planning is Different (and More Critical) for Physicians

Standard tax advice often falls short for medical professionals. Your financial landscape is unique and requires a specialized approach for several key reasons.

High-Income Brackets

Physicians quickly climb into the highest federal tax brackets. For 2024, a married couple filing jointly enters the 32% bracket at $383,901 and the 35% bracket at $487,451. At these levels, every deduction and tax-deferred contribution has a significant impact on your overall tax bill, making strategic planning essential.

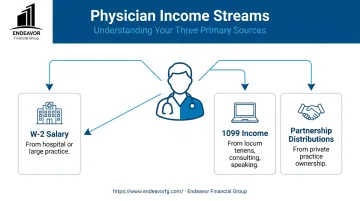

Complex Compensation Structures

Your income rarely comes from a single, simple source. Many physicians juggle a mix of:

- W-2 Salary: From a hospital or large practice group.

- 1099 Income: From locum tenens work, consulting, speaking engagements, or side gigs.

- Partnership Distributions: From owning a share in a private practice.

Each income stream has different tax implications, requiring a coordinated strategy to manage your liability effectively.

Significant Student Loan Debt

The path to becoming a doctor is expensive. According to the AAMC, the median education debt for medical school graduates in the Class of 2023 was $200,000. Managing this substantial debt influences your cash flow, investment decisions, and overall financial strategy, adding another layer of complexity to your tax planning.

Core Retirement Strategies to Lower Your Taxable Income

Your most powerful tool for reducing taxable income is maximizing tax-advantaged retirement accounts. The right strategy depends on your employment structure.

For Employed (W-2) Physicians: Your First Line of Defense

If you work for a hospital or a large medical group, your employer-sponsored plans are the foundation of your retirement savings.

- 401(k) or 403(b) Plans: Your primary goal should be to max out your pre-tax contributions each year. For 2024, the employee contribution limit is $23,000. Every dollar you contribute reduces your taxable income for the year.

- 457(b) Plans: Often available at non-profit hospitals and government institutions, these plans are a huge advantage. A 457(b) allows you to contribute an additional $23,000 (for 2024) on top of your 401(k) or 403(b) contributions, effectively doubling your tax-deferred savings potential.

For Practice Owners & Independent Contractors

If you're self-employed or run your own practice, you have access to even more powerful retirement vehicles.

- Solo 401(k): This is often the best choice for independent physicians. It allows you to contribute as both the "employee" (up to $23,000 in 2024) and the "employer." As the employer, you can contribute up to 25% of your compensation. The total combined contributions for 2024 cannot exceed $69,000.

- SEP IRA: A Simplified Employee Pension (SEP) IRA is another option. It's easy to set up, but you can only make contributions as the "employer" (up to 25% of compensation, not to exceed $69,000 for 2024). This often results in a lower maximum contribution than a Solo 401(k) for high earners.

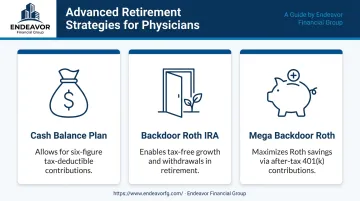

Advanced Strategies for Maximizing Savings

Once you've maxed out the standard accounts, it's time to explore advanced strategies to accelerate your savings and tax deductions.

- Cash Balance Plan: This is a powerful tool for high-income practice owners. A cash balance plan is a type of defined benefit plan that allows for massive tax-deductible contributions, often exceeding six figures annually. Contribution limits are based on age and income, allowing older physicians to save aggressively for retirement.

- Backdoor Roth IRA: Most physicians earn too much to contribute directly to a Roth IRA. The Backdoor Roth IRA is a process where you make a non-deductible contribution to a Traditional IRA and then immediately convert it to a Roth IRA. This allows your money to grow and be withdrawn tax-free in retirement.

- Mega Backdoor Roth: If your 401(k) plan allows for after-tax contributions, you may be able to use the Mega Backdoor Roth strategy. This involves making non-Roth after-tax contributions to your 401(k) and then converting them to a Roth IRA or a Roth 401(k), creating another stream of tax-free retirement income.

Navigating these advanced options requires careful planning to ensure compliance and alignment with your overall financial goals.

Tax-Efficient Tools Beyond Retirement Accounts

Optimize Retirement Tax Strategies with Expert Financial Planning

Request a quote and our experts will contact you within 24 hours with tailored solutions and pricing.

For immediate assistance, feel free to give us a direct call at 463-273-4062. You can also send us a quick email at team@endeavorfg.com.

For immediate assistance, feel free to give us a direct call at 463-273-4062. You can also send us a quick email at team@endeavorfg.com.