Effective stock portfolio management isn't about chasing hot stocks or timing the market. It's the disciplined process of building and maintaining a collection of investments that are strategically aligned with your specific financial goals.

This guide provides a clear, actionable framework for the best practices in portfolio management. We'll walk through the foundational steps, execution strategies, and ongoing discipline required to turn your investments into a powerful engine for achieving what matters most to you.

TL;DR: Key Portfolio Management Practices

- Start with a plan: Define your specific financial goals, time horizon, and personal risk tolerance before investing a single dollar.

- Asset allocation is king: How you divide your portfolio among stocks, bonds, and other assets drives most of your long-term results.

- Diversify intelligently: Spread investments across different asset classes, industries, and geographic regions to reduce volatility.

- Stay disciplined: Regularly review and rebalance your portfolio to its target allocation, forcing you to buy low and sell high.

- Minimize costs and taxes: Keep investment fees low and use tax-efficient strategies to ensure you keep more of what you earn.

What is Stock Portfolio Management? (And Why It’s Crucial for Your Goals)

A stock portfolio is simply a collection of financial assets you own, such as stocks, bonds, Exchange-Traded Funds (ETFs), and mutual funds. Portfolio management is the art and science of selecting and overseeing these assets to maximize returns for a given level of risk.

Think of it like being the general manager of a sports team. You don't just pick all-star quarterbacks. You select different players with unique skills—offense, defense, special teams—that work together to win championships. In your portfolio, stocks are your high-growth offense, while bonds might provide stable defense.

This strategic approach is crucial for hitting your long-term goals for a few key reasons:

- Takes advantage of compounding. When you reinvest earnings, they generate their own returns. A $10,000 investment earning 6% annually becomes nearly $32,000 after 20 years with compounding—not just $22,000 if you withdraw the earnings.

- Protects your purchasing power. Cash in a savings account loses value to inflation over time. A well-managed portfolio is designed to outpace inflation, making sure your money grows in real terms.

- Provides a reliable roadmap. A clear strategy prevents emotional, reactive decisions during market volatility, keeping you on track toward financial milestones like a comfortable retirement or funding a business expansion.

The Foundation: 3 Steps to Build Your Portfolio Strategy

Before you buy a single stock or fund, you need a solid foundation. This three-step process ensures your portfolio is built to serve your unique life goals.

Step 1: Define Your Financial Goals and Time Horizon

Every sound investment strategy begins with clear, measurable goals. "Get rich" is a wish, not a plan. A real goal sounds like: "Retire in 20 years with an annual income of $100,000" or "Accumulate $250,000 for a business down payment in seven years."

Next, segment these goals by their time horizon:

- Short-term (< 3 years): Money for a house down payment or a near-term capital expense. These funds should be in low-risk assets, not volatile stocks.

- Mid-term (3-10 years): Goals like funding a child's college education. This allows for a more balanced mix of growth and stability.

- Long-term (10+ years): Retirement is the classic example. A longer time horizon allows you to take on more risk for potentially higher returns, as you have time to recover from market downturns.

Step 2: Assess Your Personal Risk Tolerance

Risk tolerance is your ability and willingness to handle swings in your portfolio's value. It comes down to two distinct factors: your financial capacity for risk and your emotional willingness to take it.

Your risk capacity is your financial ability to withstand losses without jeopardizing your goals. A young professional with stable income has a higher capacity than someone nearing retirement. In contrast, your risk willingness is your emotional comfort with volatility—some people sleep soundly through a 20% drop, while others panic.

A high-net-worth individual might have a high capacity to take risks but a low willingness to do so, making them a conservative investor. Understanding both sides of this equation is key to building a portfolio you can stick with.

Step 3: Create a Formal Investment Policy Statement (IPS)

An Investment Policy Statement (IPS) is a formal document that acts as the "constitution" for your portfolio. It outlines your goals, risk tolerance, time horizon, and target asset allocation.

A written IPS is a powerful tool. When the market gets choppy and financial news channels are screaming "sell," your IPS acts as a rational anchor. It grounds your decisions in your long-term plan, preventing emotional mistakes that can derail your financial future.

Executing Your Plan: Asset Allocation and Diversification

With your foundational strategy in place, it's time to build the portfolio. This stage centers on two core principles: asset allocation and diversification.

Determining Your Ideal Asset Allocation

Asset allocation is the practice of dividing your portfolio among different asset categories like stocks, bonds, and cash. It’s not about picking individual winning stocks; it’s about getting the big-picture mix right. In fact, research from Vanguard suggests that asset allocation is responsible for around 90% of a portfolio's return variability over time.

While your specific allocation should be tailored to you, here are some general models:

- Aggressive (e.g., 80% stocks / 20% bonds): Suitable for investors with a long time horizon and high risk tolerance.

- Moderate (e.g., 60% stocks / 40% bonds): A classic balanced approach for those with mid-to-long-term goals who want growth with less volatility.

- Conservative (e.g., 30% stocks / 70% bonds): Designed for investors prioritizing capital preservation, such as those nearing or in retirement.

The Power of Diversification

Diversification builds on this by ensuring you don't concentrate your risk in a single investment. Its goal is to reduce portfolio volatility because different assets react differently to the same economic news. When tech stocks are down, for example, consumer staples or healthcare stocks might be up.

True diversification happens on multiple levels:

- Across asset classes: Holding both stocks and bonds.

- Within asset classes: Owning stocks from various sectors (technology, healthcare, industrial, financial) and bonds of different types (government, corporate).

- Geographically: Including both U.S. and international stocks in your portfolio to capture global growth and reduce country-specific risk.

Selecting Your Investments

While you can build a portfolio with individual securities, most investors use tools like mutual funds or Exchange-Traded Funds (ETFs) to achieve diversification efficiently. These funds hold hundreds or thousands of stocks or bonds, providing a broad market footprint in a single investment.

However, choosing the right funds and ensuring they align with your specific asset allocation model requires careful planning. This is where working with a financial advisor can help translate your strategy into a well-executed, disciplined portfolio.

Ongoing Management: Key Practices to Keep Your Portfolio on Track

Building a portfolio is not a "set it and forget it" activity. Disciplined, ongoing management is what separates successful investors from the rest.

Monitor and Review Your Performance

You don't need to check your portfolio daily. That's a recipe for anxiety and rash decisions. Instead, set a regular schedule—quarterly or semi-annually—to review your performance.

During this review, compare your returns to relevant benchmarks (like the S&P 500 for U.S. large-cap stocks) and, more importantly, check if you are still on track to meet the goals outlined in your IPS.

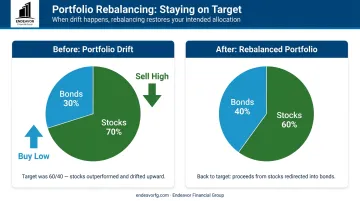

Rebalance Your Portfolio

Over time, market movements will cause your portfolio's allocation to drift. In a strong bull market, a 60/40 portfolio might become 70/30 as your stocks outperform your bonds.

Rebalancing is the process of selling some of your outperforming assets and using the proceeds to buy underperforming ones, bringing your portfolio back to its original target. This imposes a crucial discipline: it forces you to systematically sell high and buy low.

Practice Tax-Efficient Investing

Your after-tax return is what truly matters. Two key strategies can significantly improve your after-tax returns:

- Use strategic asset location. Place tax-inefficient investments (like corporate bonds) in tax-advantaged accounts like a 401(k) or IRA, and keep tax-efficient ones in taxable brokerage accounts.

- Practice tax-loss harvesting. Sell an investment that has lost value to "harvest" the loss. You can then use that loss to offset capital gains on winning investments, reducing your overall tax bill.

Keep Costs Low

Investment fees, like expense ratios on mutual funds and trading commissions, are a direct drag on your returns. While a 1% fee might sound small, its impact over time is enormous.

According to Investor.gov, on a $100,000 portfolio earning 4% annually over 20 years, a 1% annual fee would reduce your final account value by nearly $30,000 compared to a 0.25% fee. Keeping costs down is one of the most effective ways to improve your long-term results.

The Endeavor Advantage: Integrating Your Portfolio with a Comprehensive Wealth Plan

Effective stock portfolio management doesn't happen in a vacuum. It must be fully integrated with your entire financial life—tax planning, retirement income strategies, estate planning, and insurance. A great investment portfolio that creates a massive tax bill or conflicts with your business succession plan isn't a great plan at all.

At Endeavor Financial Group, we take a holistic approach. Our team of certified professionals, including CFP® and CFA® charterholders, acts as your financial quarterback. We don't just manage assets; we build comprehensive wealth plans where your portfolio is a powerful tool that supports every part of your financial life.

Our structured five-step process—from discovery and analysis to implementation and ongoing monitoring—provides a clear roadmap for your financial future.

This approach is especially valuable for our clients, including pre-retirees and business owners facing complex financial decisions. We ensure your portfolio is always aligned with your broader goals, giving you the clarity and confidence to move forward.

Ready to build a portfolio that truly aligns with your life's goals? Schedule a consultation with our team today.

Frequently Asked Questions

What are the 7 steps of portfolio management?

The core process involves: 1) Defining your goals, 2) Assessing your risk tolerance, 3) Setting your asset allocation, 4) Diversifying your holdings, 5) Selecting your investments, 6) Monitoring performance, and 7) Rebalancing regularly.

Is 70/30 better than 60/40?

Neither is inherently "better." A 70% stock / 30% bond portfolio is more aggressive and generally suited for investors with a longer time horizon and higher risk tolerance. The classic 60/40 mix offers a more balanced approach between growth and stability. The right choice depends entirely on your personal IPS.

How often should I rebalance my stock portfolio?

Most financial advisors recommend rebalancing on a set schedule (annually or semi-annually) or whenever your allocation drifts by a predetermined amount, such as 5%. The key is to be consistent and disciplined.

What is the difference between active and passive portfolio management?

Active management attempts to beat a market index through stock picking, which often involves higher fees. Passive management aims to match an index (like the S&P 500) using low-cost funds. Historically, most active managers have failed to outperform their passive benchmarks over time.

Can I manage my own portfolio without a financial advisor?

Yes, it is possible for investors who are knowledgeable, disciplined, and have the time to do so. However, a qualified financial advisor can provide expertise, objectivity during volatile markets, and comprehensive planning that integrates your portfolio with taxes, retirement, and estate goals.

How important are low fees in portfolio management?

Fees are critically important. Because they compound over time just like returns, even a small difference in fees can lead to a tens or even hundreds of thousands of dollars difference in your final portfolio value over a long investment horizon.