These aren't just minor disputes; excessive fee lawsuits resulted in $203.3 million in settlements in 2024, holding fiduciaries personally accountable for plan losses. This guide provides a clear, comprehensive overview of your responsibilities under the Employee Retirement Income Security Act (ERISA). Understanding these duties is the first step in protecting your plan participants, your company, and yourself.

TL;DR: Your Key Fiduciary Takeaways

- As a plan sponsor, you are almost certainly a fiduciary and must act solely in the best interests of your plan participants.

- Your core duties include acting with prudence, diversifying investments, ensuring fees are reasonable, and following plan documents.

- Failing to meet these responsibilities can result in personal liability to restore any losses to the plan.

- You can mitigate risk by establishing a prudent process, documenting decisions, and hiring qualified professionals for guidance.

What Is a Retirement Plan Fiduciary? (And Are You One?)

Under ERISA, your title doesn’t make you a fiduciary—your actions do. The Department of Labor (DOL) clarifies that fiduciary status is based on the functions you perform for the plan. If you exercise discretionary control over plan management, administration, or assets, you are a "functional fiduciary."

This means if you select the investment options, choose the service providers, or approve distributions, you are acting as a fiduciary and are subject to ERISA’s strict standards.

Common Types of Fiduciaries

Most retirement plans have several fiduciaries, each with a distinct role:

- Named Fiduciary: The person or entity identified in the plan document—typically the employer or a specific committee.

- Plan Administrator: The entity responsible for day-to-day operations, such as enrolling participants and processing transactions.

- Trustee: The person or entity with authority and control over the plan's assets.

- Investment Advisor: Anyone who provides investment advice for a fee regarding the plan’s assets.

Settlor vs. Fiduciary Functions

It’s important to distinguish between business decisions and fiduciary actions. "Settlor" functions are business decisions made for the company, not the plan. For example, the decision to establish, amend, or terminate a retirement plan is a settlor function.

However, the actions you take to implement that decision are fiduciary in nature. Deciding to terminate the plan is a business choice, but the process of liquidating assets and paying out benefits to participants must be handled according to strict fiduciary standards.

The Core Fiduciary Duties Mandated by ERISA

All your actions as a fiduciary are governed by a set of fundamental duties defined by ERISA. These aren't suggestions; they are legal requirements that are the foundation for responsible plan management.

Duty of Loyalty (Acting Solely in the Interest of Participants)

This is your primary duty. Every decision must be for the exclusive purpose of providing benefits to participants and their beneficiaries, ensuring plan assets cover only reasonable and necessary expenses. The interests of participants must always come before those of the company.

Duty of Prudence

ERISA’s "prudent person" rule requires you to act with the care, skill, and diligence a knowledgeable person in a similar role would use. This means having a documented, objective process for making decisions, even if you are not a financial expert.

If you lack the necessary expertise, you have a duty to hire an expert who does. The Department of Labor (DOL) provides guidance on this responsibility.

Duty to Diversify

You must diversify the plan's investments to minimize the risk of large losses. This is why most 401(k) plans offer a broad menu of options across different asset classes, such as stocks, bonds, and capital preservation funds, allowing participants to build a portfolio that fits their risk tolerance.

Duty to Follow Plan Documents

Your plan has official documents that outline its rules and operations. You have a legal duty to operate the plan in strict accordance with these documents, unless a specific provision is inconsistent with ERISA law. Adhering to the plan document is critical for maintaining compliance.

Duty to Avoid Prohibited Transactions

Fiduciaries are forbidden from engaging in transactions that create a conflict of interest. This includes any form of self-dealing, such as using plan assets for personal or company benefit.

You must also avoid improper transactions with a "party in interest," like the business owner or major shareholders. For example, the plan cannot lend money to the company at a below-market interest rate.

Key Fiduciary Responsibilities in Practice

Understanding the core duties is one thing; applying them is another. Here’s how these principles translate into day-to-day responsibilities for managing your company’s retirement plan.

Prudent Investment Selection and Monitoring

Your first task is to select a diversified menu of investment options for participants. This process should be guided by an Investment Policy Statement (IPS), a formal document that outlines the criteria for selecting, monitoring, and replacing plan investments.

Your duty doesn't end once the funds are selected. You must continuously monitor their performance, fees, and ongoing suitability. Best practice is to conduct and document a formal review at least annually to ensure the investment lineup remains appropriate for your participants.

Ensuring Fees Are Reasonable

Excessive fees are one of the most common reasons for ERISA litigation. As a fiduciary, you must ensure that all plan fees—for administration, recordkeeping, and investment management—are "reasonable" for the services provided.

This requires you to periodically benchmark your plan’s fees against industry averages. For example, according to the 25th edition of the 401k Averages Book, the average total cost for a $5 million plan is around 1.08% of assets. A formal fee review and benchmarking process should be conducted and documented every 2-3 years.

Timely and Accurate Plan Administration

Operational errors can easily lead to a fiduciary breach. One of the most critical duties is depositing employee contributions on time. The general rule is to deposit contributions as soon as they can be reasonably segregated from company assets.

This deposit must occur no later than the 15th business day of the following month. For small plans (fewer than 100 participants), a 7-business-day safe harbor also exists.

Other key administrative duties include:

- Processing distributions and loans correctly and on time.

- Providing required notices to participants, like the Summary Plan Description (SPD).

- Filing the annual Form 5500 with the federal government.

Maintaining an ERISA Fidelity Bond

You are required to have an ERISA fidelity bond, which is insurance that protects the plan from losses due to fraud or dishonesty by those who handle plan assets. The bond must cover at least 10% of the plan assets handled, with a maximum requirement of $500,000 for most plans.

This is not the same as fiduciary liability insurance; it protects the plan, not the fiduciaries themselves.

Common Pitfalls and How to Avoid Fiduciary Breaches

Even with the best intentions, fiduciaries can make mistakes. Understanding the most common errors is the first step toward avoiding them.

Failing to Document the Process

When regulators or courts review a fiduciary’s actions, their primary focus is on the process, not the outcome. An investment can lose money without it being a fiduciary breach, as long as the decision to include it was made through a prudent, documented process. The biggest mistake is having no records to prove your diligence, such as:

- Meeting minutes

- Fee benchmarking reports

- An Investment Policy Statement (IPS)

The "Set It and Forget It" Mentality

Fiduciary duty is an ongoing responsibility. Many plan sponsors select a provider or an investment lineup and then fail to monitor them regularly. Markets change, fees evolve, and a provider’s service level can decline. A passive approach is a direct violation of the duty of prudence.

Ignoring Participant Complaints or Questions

Fiduciaries have a duty to respond to participant inquiries in a timely manner. Ignoring complaints about fees, investment performance, or administrative errors is a breach of duty and a major red flag. Often, a single participant's question can uncover a larger operational issue that needs to be addressed.

How to Mitigate Your Fiduciary Risk and Liability

While you can't eliminate fiduciary risk entirely, you can take concrete steps to manage it effectively and demonstrate a commitment to your responsibilities.

Establish and Follow a Prudent Process

Create a formal process for all plan-related decisions. This often involves forming a retirement plan committee that meets regularly (e.g., quarterly or annually) to review investments, fees, and plan administration. Document everything.

Keep detailed minutes of every meeting, including who was present, what was discussed, the data reviewed, and the rationale for every decision.

Hire Qualified Professional Help

While you can delegate tasks, you cannot delegate your ultimate fiduciary responsibility. However, hiring qualified experts is a key part of demonstrating prudence. You can engage professional fiduciaries to share the burden.

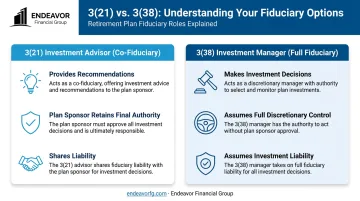

- A 3(21) Investment Advisor acts as a co-fiduciary, providing recommendations and guidance, but the plan sponsor retains the final decision-making authority.

- A 3(38) Investment Manager takes on full discretionary control and legal responsibility for selecting, monitoring, and replacing the plan's investments.

A fee-only fiduciary firm like Endeavor Financial Group can serve as a dedicated partner in this process. Our team of credentialed professionals, including CFP® and CFA® charterholders, helps you establish a prudent framework to fulfill your duties with confidence.

Purchase Fiduciary Liability Insurance

Unlike the required fidelity bond that protects the plan’s assets, fiduciary liability insurance protects the fiduciaries themselves. This insurance covers legal costs and potential settlements arising from claims of mismanagement or a breach of fiduciary duty. While not required by ERISA, it is a critical tool for protecting your personal assets.

Frequently Asked Questions

Who is the fiduciary on a retirement plan?

Anyone who exercises discretionary control over the plan's management or assets is considered a fiduciary. This can include the employer, company officers, plan administrators, trustees, and investment committee members.

What are the three types of retirement plan fiduciaries?

Retirement plan fiduciaries generally fall into three categories: the Plan Administrator (overseeing operations), the Trustee (overseeing assets), and the Investment Fiduciary (providing investment advice or management, such as a 3(21) or 3(38) advisor).

What is the average cost of a retirement plan fiduciary?

Costs vary widely based on the level of service, plan size, and complexity. As a benchmark, total advisor compensation for a $5 million plan averages around 0.37% of assets annually. The key is documenting why the fees paid are reasonable for the services received.

Can I be held personally liable for a fiduciary breach?

Yes. Fiduciaries can be held personally liable to restore any losses to the plan that result from a breach of their duties. This means your personal assets could be at risk.

What is an ERISA fidelity bond?

An ERISA fidelity bond is a type of insurance that protects the plan's assets from losses caused by acts of fraud or dishonesty. It is a legal requirement for anyone who handles plan funds.

How often should I review my plan's investments and fees?

Plan investments should be formally reviewed against the Investment Policy Statement at least annually. Plan fees should be benchmarked against the market every two to three years to ensure they remain reasonable.