Without a plan, you risk turning a great benefit into a tax headache. This guide will break down the essential tax rules you need to know. We'll walk through clear, practical examples of different selling strategies and show you how to make your ESPP a cornerstone of your broader financial goals, not just an afterthought.

TL;DR: Key ESPP Tax Strategies

- An ESPP lets you buy company stock at a discount, commonly up to 15%.

- The tax outcome depends on whether your sale is a "Qualifying Disposition" or a "Disqualifying Disposition."

- A Qualifying Disposition requires holding stock for over two years from the offer date and one year from the purchase date, resulting in lower long-term capital gains rates on most of your profit.

- Failing to adjust your cost basis on your tax return is a common mistake that leads to double taxation.

- Your ESPP strategy should align with your overall financial plan, balancing tax savings with portfolio diversification.

Understanding the Mechanics of Your ESPP

To build an effective tax strategy, you first need to understand how your ESPP works. These plans have a few key components and terms that set the stage for your financial decisions.

The Offering Period and Purchase Period

Your ESPP operates on a set schedule. The two most important timelines are:

- Offering Period: The set timeframe, often six months, when you enroll and contribute money through payroll deductions. The first day is the "offering date" or "grant date."

- Purchase Period: The day your accumulated funds are used to buy company stock. For an offering period ending June 30, the purchase would happen on that date.

The Discount and the "Lookback" Provision

The financial benefit of an ESPP comes from two key features: the discount and the lookback provision.

The discount is straightforward: your plan allows you to buy company stock for less than its market price, typically at a discount of up to 15%.

The lookback provision makes this even better. It allows your company to apply the 15% discount to the stock price at either the start of the offering period or the end, whichever is lower.

Here’s an example:

- Offering Date (Jan 1): Stock price is $100.

- Purchase Date (June 30): Stock price is $120.

With a lookback, your 15% discount is applied to the lower price—$100. You get to buy shares for just $85, even though the stock is currently trading at $120. This combination immediately creates a significant paper gain.

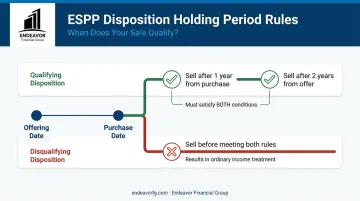

The Core Tax Rules: Qualifying vs. Disqualifying Dispositions

How and when you sell your ESPP shares is the single biggest factor determining your tax bill. The IRS defines two types of sales, or "dispositions," each with its own set of rules.

What is a Qualifying Disposition?

A qualifying disposition allows you to receive the most favorable tax treatment. To achieve this, you must meet both of these holding period requirements:

- The sale date must be at least two years after the offering (grant) date.

- The sale date must be at least one year after the purchase (exercise) date.

When you meet these conditions, your profit is split into two parts. A small portion, known as the "bargain element," is taxed as ordinary income. The rest of your profit is taxed at the lower long-term capital gains rate. This structure is designed to reward long-term investors.

What is a Disqualifying Disposition?

This is any sale that fails to meet both of the holding period requirements for a qualifying disposition. Selling your shares immediately or within a year of purchase is the most common example.

With a disqualifying disposition, the entire discount you received is taxed as ordinary income. This is calculated as the spread between the fair market value (FMV) on the purchase date and your discounted purchase price.

Any additional profit is then treated as a capital gain. Depending on how long you held the shares, this gain can be either short-term (held one year or less) or long-term (held more than one year).

ESPP Tax Scenarios in Action: A Practical Breakdown

Let's put these rules into practice with a consistent example. Seeing the math side-by-side makes the financial impact of your timing crystal clear.

Scenario Assumptions:

- Company Stock Price (Offering Date): $50

- Company Stock Price (Purchase Date): $60

- ESPP Discount: 15% (with a lookback provision)

- Your Purchase Price: $42.50 per share (15% off the $50 offering date price)

- Your Sale Price: $80 per share

- Your Tax Bracket (for this example): 24% ordinary income, 15% long-term capital gains

Scenario 1: Disqualifying Disposition (Selling within one year)

You decide to sell your shares three months after the purchase date to lock in your gains quickly. This does not meet the holding period rules, making it a disqualifying disposition.

- Calculate Ordinary Income: The spread between the FMV on the purchase date ($60) and your actual purchase price ($42.50) is taxed as ordinary income.

- $60.00 - $42.50 = $17.50 per share (Ordinary Income)

- Calculate Short-Term Capital Gain: Your cost basis is adjusted to include the amount taxed as income ($42.50 + $17.50 = $60). The remaining profit is a short-term capital gain.

- $80.00 (Sale Price) - $60.00 (Adjusted Cost Basis) = $20.00 per share (Short-Term Capital Gain)

Scenario 2: Qualifying Disposition (Meeting both holding periods)

You wait patiently, selling your shares two and a half years after the offering date and 18 months after the purchase date. This meets both rules for a qualifying disposition.

- Calculate Ordinary Income: The ordinary income portion is the lesser of two amounts: the discount calculated at the offering date (15% of $50 = $7.50) or your actual profit ($80 - $42.50 = $37.50).

- The lesser amount is $7.50 per share (Ordinary Income)

- Calculate Long-Term Capital Gain: Your cost basis is adjusted by the ordinary income amount ($42.50 + $7.50 = $50). The rest is a long-term capital gain.

- $80.00 (Sale Price) - $50.00 (Adjusted Cost Basis) = $30.00 per share (Long-Term Capital Gain)

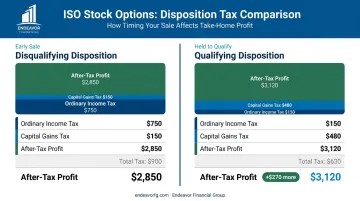

Comparing the After-Tax Profit

Here’s how the two scenarios stack up after taxes, assuming you sell 100 shares.

| Metric (per 100 shares) | Disqualifying Disposition | Qualifying Disposition |

|---|---|---|

| Pre-Tax Profit | $3,750 | $3,750 |

| Ordinary Income Tax | $420 ($1,750 x 24%) | $180 ($750 x 24%) |

| Capital Gains Tax | $480 ($2,000 x 24%) | $450 ($3,000 x 15%) |

| Total Tax Bill | $900 | $630 |

| After-Tax Profit | $2,850 | $3,120 |

In this example, the qualifying disposition puts an extra $270 in your pocket for every 100 shares sold, simply by strategically timing your sale.

Key Strategies to Maximize Your ESPP (and Avoid Common Pitfalls)

Understanding the rules is half the battle. Applying them strategically is what maximizes your benefit. Here are some essential tips to keep in mind.

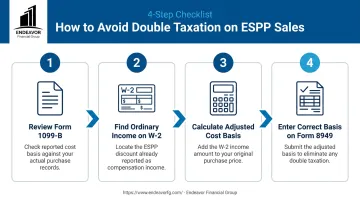

How to Avoid Double Taxation on Your ESPP Sale

This is the single most common and costly mistake ESPP participants make. When you sell your shares, your brokerage firm will send you a Form 1099-B. However, the "cost basis" reported on this form is often just your discounted purchase price. It does not include the portion of your gain that was already taxed as ordinary income on your W-2.

If you use this incorrect basis when filing your taxes, you will pay capital gains tax on money that has already been taxed. To fix this, you must manually adjust your cost basis on IRS Form 8949. Add the amount of ordinary income reported on your W-2 to your purchase price. This ensures you only pay capital gains tax on the actual capital gain. According to guidance from major brokerages like Schwab, this adjustment is often necessary to avoid overpaying.

Balancing Tax Benefits with Concentration Risk

Waiting two years to get a better tax rate sounds great, but it's not without risk. Holding a large amount of your company's stock for an extended period exposes you to concentration risk.

As Morgan Stanley at Work notes, having too much of your net worth tied to your employer’s performance can be a high-stakes gamble. A significant drop in the stock price could easily wipe out any potential tax savings.

Create a disciplined selling strategy that works for you. Some options include:

- Sell immediately to lock in the gain from the discount, accepting the higher tax rate to reinvest the proceeds into a diversified portfolio.

- Sell a portion to recoup your initial investment, then hold the remaining shares to aim for a qualifying disposition on the "house money."

Plan for Your Cash Flow

Remember that your ESPP contributions are deducted directly from your paycheck, which reduces your take-home pay. Before enrolling or increasing your contribution percentage, make sure you can comfortably afford it without straining your monthly budget or neglecting other financial goals like paying down debt or contributing to your 401(k).

Beyond the Sale: Integrating Your ESPP into a Holistic Financial Plan

Your ESPP isn't just a standalone perk; it's a powerful tool that should be integrated with your comprehensive financial strategy. The proceeds from a sale can be a catalyst for achieving major goals, like paying down high-interest debt, funding a down payment, or boosting retirement savings.

Understanding the complexities of equity compensation—from ESPPs and RSUs to stock options—is a key part of financial planning. Each type of equity has a different "tax clock" and requires careful coordination with your overall investment and tax strategy.

At Endeavor Financial Group, we help clients build a cohesive plan that integrates all pieces of their financial puzzle. Our five-step process ensures that decisions about your ESPP align with your long-term goals for retirement, diversification, and tax efficiency.

By balancing the concentration risk of company stock with secure, diversified investments, we help you build a resilient financial future.

Frequently Asked Questions

How are ESPPs taxed and what are the tax benefits?

You owe taxes when you sell your shares, not when you buy them. The key benefit of a qualifying disposition is that a larger portion of your profit may be taxed at lower long-term capital gains rates.

How do I avoid double taxation on ESPP shares?

To avoid double taxation, you must manually adjust the cost basis on Form 8949. Add the discount amount, reported as compensation on your W-2, to your purchase price. This corrects the cost basis provided on your Form 1099-B.

What is the two-year rule for ESPP qualifying dispositions?

To qualify, you must sell your shares at least two years after the offering date, which is the start of the contribution period. This is a different date than the purchase date, so it's critical to track both.

Should I sell my ESPP shares immediately?

Selling immediately locks in your gain but triggers higher taxes as a disqualifying disposition. While you lose the tax advantages, this strategy is common for reducing the risk of holding too much company stock.

What happens if the stock price drops after I buy my ESPP shares?

Yes, the tax rules still apply even if the price drops. According to the IRS, you can have ordinary income from the discount and a capital loss on the same sale in a disqualifying disposition.