This is where advisory portfolio management services (PMS) find their sweet spot. It's a collaborative model that bridges the gap between DIY investing and fully delegating control. It provides the professional expertise you need while ensuring you always have the final say. This article explores what advisory PMS is, how it differs from other models, and the best practices for making it a successful part of your financial strategy.

TL;DR: Advisory Portfolio Management Services

- You get expert investment advice but keep the final say on all trades.

- Gain tailored strategies and pro-level research while retaining full control.

- This model is ideal for hands-on investors, business owners, and pre-retirees.

- Success hinges on clear communication with a transparent, qualified advisor.

What is Advisory Portfolio Management? A Collaborative Approach

Advisory portfolio management is a service where a professional portfolio manager or financial advisor provides customized investment advice and recommendations based on your unique goals, risk tolerance, and financial situation.

The core of this relationship is partnership. Your advisor handles the heavy lifting—researching markets, analyzing securities, and identifying opportunities that align with your strategy. They then present these ideas to you with a clear rationale.

For example, they might suggest selling X stock and purchasing a Y bond ETF to increase your portfolio’s income stream. However, no transaction occurs without your explicit approval, ensuring you always remain in control.

How the Process Works Step-by-Step

A disciplined advisory relationship follows a clear and structured path to ensure your strategy is comprehensive and aligned with your life. At Endeavor Financial Group, we use a five-step process to build a financial roadmap for our clients.

- Introductory Meeting & Discovery: The journey begins with an in-depth analysis of your financial health, long-term goals (like retirement or a business sale), and comfort with risk. This is a chance to see if the partnership is a good fit and to lay the groundwork for your plan.

- Exploration & Preliminary Planning: With a clear understanding of your objectives, the advisor explores your situation in greater detail. This involves more detailed conversations to begin sketching a preliminary plan that reflects your unique circumstances.

- Detailed Planning & Recommendation: Based on the discovery phase, the advisor develops a tailored investment policy statement (IPS) and presents specific, actionable investment ideas designed to move you toward your goals.

- Client Approval & Implementation: You review the recommendations, ask clarifying questions, and give the final approval. Once you give the green light, the trades are executed.

- Ongoing Support & Monitoring: The partnership doesn't end after the initial setup. Your advisor continually monitors the portfolio and market conditions, providing regular performance reports and suggesting adjustments as your life and the economy evolve.

Advisory vs. Discretionary Management: What's the Difference?

The most critical distinction between investment management styles is who has the authority to place trades in your account. Understanding this difference is key to choosing the right model for your needs.

In an advisory management relationship, you retain full control. Your advisor proposes trades and strategies, but you must approve them before any action is taken. This collaborative, "do-it-with-me" model is built on partnership.

Conversely, discretionary management involves delegating trading authority to your portfolio manager. This "do-it-for-me" approach allows them to act on your behalf without seeking approval for each transaction, enabling faster execution.

Here’s a simple breakdown of the key differences:

| Feature | Advisory Management | Discretionary Management |

|---|---|---|

| Decision-Making Power | Client | Portfolio Manager |

| Client Involvement | High | Low |

| Speed of Execution | Slower (requires approval) | Faster (no approval needed) |

| Best For | Investors wanting control and expert partnership | Investors preferring to delegate decisions |

The Core Benefits of an Advisory Approach for Investors

For investors who want to stay engaged, the advisory model offers several distinct advantages that align with their desire for control, transparency, and tailored guidance.

Complete Control and Transparency

Because every transaction requires your approval, you always know exactly what is happening in your portfolio and why. This structure eliminates surprises, builds trust, and ensures the strategy remains aligned with your comfort level.

The securities are held in your name in your own account, giving you direct ownership and a clear view of your holdings at all times.

Access to Professional Expertise and Research

With an advisory service, you gain access to institutional-quality market research, analytical tools, and the seasoned experience of professionals—without spending your own time sifting through data.

Working with an advisor who holds designations like the CFP® (Certified Financial Planner) or CFA® (Chartered Financial Analyst) means you get guidance from someone who has met rigorous standards for ethics and expertise.

Highly Customized and Flexible Strategies

Advisory services are the opposite of a one-size-fits-all approach. The strategy is built from the ground up to fit your unique circumstances.

For example, a business owner with irregular cash flow might need a flexible contribution plan. A pre-retiree's focus, however, might shift entirely to capital preservation and generating a reliable income stream.

A Partnership for Financial Education

The collaborative nature of the advisory relationship provides a powerful learning opportunity. By reviewing and discussing each recommendation with your advisor, you become more knowledgeable and confident about your financial decisions over time. It’s an ongoing dialogue that empowers you to better understand the "why" behind your investment strategy.

Understanding the Potential Drawbacks and How to Mitigate Them

While the advisory model offers significant benefits, it's important to acknowledge the potential challenges to can help you and your advisor build a stronger, more effective partnership.

- Execution Delays: The need for client approval can slow down execution in fast-moving markets. To mitigate this, establish clear communication protocols and expected response times with your advisor from day one.

- Emotional Decision-Making: During market volatility, fear and greed can lead investors to reject sound advice. Research from firms like Vanguard shows that behavioral coaching is one of the most significant ways an advisor adds value. To avoid this pitfall, trust your advisor to provide an objective perspective when markets are turbulent.

- Higher Fees than DIY: Professional advice has a cost, typically a percentage of assets under management (AUM), which is more expensive than a DIY approach. Ensure you have a crystal-clear understanding of the fee structure and that the value—in time saved, strategic planning, and mistakes avoided—justifies the cost.

Best Practices for a Successful Advisory Partnership

A successful advisory partnership requires active participation and a commitment to a few key principles.

Vet Credentials and Fiduciary Commitment

Look for advisors with reputable, rigorous certifications like CFP® (Certified Financial Planner) or CFA® (Chartered Financial Analyst). These designations signal a deep level of expertise and a commitment to ethical conduct. Most importantly, ensure your advisor is a fiduciary—someone legally and ethically bound to act in your best interest at all times. You can verify a firm's registration and an advisor's background through the SEC's Investment Adviser Public Disclosure (IAPD) website.

Prioritize a Firm with a Structured Process

A firm that follows a documented process for discovery, analysis, and monitoring brings discipline and consistency to your financial life. For example, the five-step process we use at Endeavor Financial Group ensures that every client receives a comprehensive plan that is built, implemented, and reviewed with the same high level of care. This structure provides a clear roadmap and eliminates guesswork.

Establish Clear Communication Expectations

A strong partnership is built on proactive and transparent communication. At the outset, discuss and agree upon the frequency and mode of contact. Will you have quarterly review meetings? How will market updates be delivered? Setting these expectations early prevents misunderstandings down the road.

Be an Engaged and Honest Partner

The success of the advisory model depends heavily on you. To get the most out of the relationship, you must be willing to:

- Provide complete and accurate financial information.

- Be honest about your goals, concerns, and risk tolerance.

- Ask questions when you don't understand a recommendation.

- Respond to your advisor in a timely manner.

Look Beyond Just Investment Picks

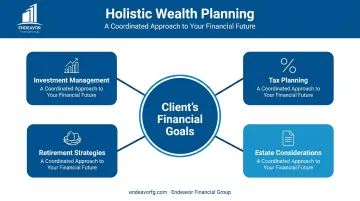

The best advisory relationships offer comprehensive wealth planning, not just stock picking. Your investments are just one piece of a larger puzzle, so it’s vital to choose an advisor who examines your entire financial picture.

This includes tax planning, retirement income strategies, and estate considerations. A holistic approach—like the one we use at Endeavor Financial Group—ensures all parts of your financial life work together efficiently.

Frequently Asked Questions

What are advisory portfolio management services in simple terms?

It's a partnership where a financial expert gives you investment advice and recommendations, but you always make the final call on whether to buy or sell. The advisor researches and suggests, but you approve every transaction.

What is the main difference between advisory and discretionary portfolio management?

The key difference is trading authority. In an advisory relationship, you (the client) retain all decision-making power. In a discretionary relationship, you delegate that authority to the portfolio manager to trade on your behalf.

Is $200,000 enough to work with a financial advisor?

While many firms have high minimums (often $500,000 or more), many advisors work with clients at this level, especially if they see a long-term fit. The key is finding a firm whose service model matches your needs.

What are the typical fees for advisory portfolio management services?

Fees are usually an annual percentage of assets under management (AUM), often ranging from 0.5% to 2%. According to research from industry expert Michael Kitces, this percentage typically decreases for larger portfolios.

What is the best investment for a 70 year old?

There's no single "best" investment, as advice must be tailored to an individual's risk tolerance, income needs, and financial health. Generally, the focus for a 70-year-old shifts to capital preservation and income using bonds, dividend stocks, and cash equivalents.

How do I know if an advisory PMS provider is trustworthy?

Check their registration with regulatory bodies like the SEC through its IAPD database. Verify their fiduciary status in writing, read client reviews, and look for established credentials like the CFP® or CFA® designations.