For many pre-retirees and those already in retirement, this uncertainty can be a major source of stress. The retirement bucket strategy offers a powerful framework for structuring your assets to solve this very problem. It’s a logical approach to generating income while managing risk, but the practical steps for putting it into action are often misunderstood.

This guide will provide a complete, step-by-step roadmap to implementing and maintaining a bucket strategy, helping you protect your savings from volatility and gain the financial confidence you deserve.

Key Takeaways

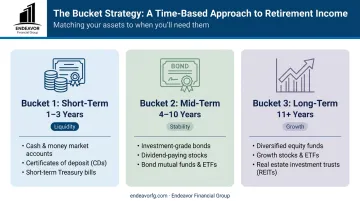

- Divides your assets into three buckets for short-term (1-3 years), mid-term (4-10 years), and long-term (11+ years) needs.

- Protects near-term income from market volatility, reducing "sequence of returns risk."

- Uses a cash bucket for immediate expenses, refilling it from bond and stock buckets over time.

- Balances short-term safety with the essential need for long-term portfolio growth.

What Is the Retirement Bucket Strategy?

The retirement bucket strategy is an asset allocation and withdrawal method designed to create a predictable income stream from your portfolio. Its primary goal is to insulate the funds you need for immediate living expenses from the day-to-day swings of the stock market.

By segmenting your money based on time horizons, you create a clear structure. The money you need for bills and groceries next year isn't invested in the same way as the money you won't touch for another 15 years.

This stands in contrast to a traditional "total-return" approach, where all assets are held in a single portfolio. In that model, withdrawals are taken from the total pool, which can force you to sell assets at the worst possible time—during a market downturn.

The bucket strategy is designed to prevent that exact scenario.

Why Use the Retirement Bucket Strategy for Retirement?

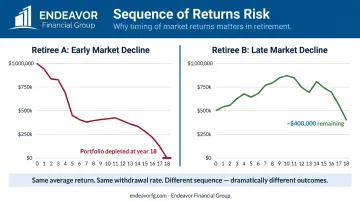

The bucket strategy’s primary strength is its ability to solve one of the biggest and least-understood threats to a secure retirement: sequence of returns risk.

The Core Problem It Solves: Sequence of Returns Risk

Sequence of returns risk is the danger of experiencing poor investment returns in the first few years of retirement. The timing of market performance has a massive impact when you start making withdrawals. Strong returns early on can set you up for success, while a bear market right after you retire can be devastating.

Consider this powerful example: Schwab compared two hypothetical retirees both starting with $1,000,000 and withdrawing $50,000 per year (adjusted for inflation).

- Retiree A experiences a 15% market decline in their first two years of retirement. Their portfolio runs out of money in just 18 years.

- Retiree B enjoys a calm market early on and experiences the same 15% decline a decade later. After 18 years, they still have nearly $400,000 left.

The average returns were the same, but the sequence of those returns made all the difference. Withdrawing money from a declining portfolio forces you to sell more shares at low prices, permanently impairing your capital base and its ability to recover and grow. The bucket strategy is a direct defense against this risk.

Key Benefits for Retirees

Beyond mitigating risk, the bucket strategy offers several other advantages:

- Provides psychological peace of mind by setting aside 1-3 years of cash, making it easier to ignore market volatility and avoid panicked selling.

- Creates a disciplined rebalancing plan that forces you to "sell high." You systematically trim gains from growth assets to refill your cash bucket.

- Delivers clarity and simplicity with an intuitive structure: a bucket for now, one for the medium-term, and one for long-term growth.

How the Retirement Bucket Strategy Works: A Step-by-Step Guide

Putting the bucket strategy into action is a straightforward process. It starts with calculating your annual income needs and then structuring your investments across three distinct buckets.

Step 1: Calculate Your Annual Income Needs

First, you need to know how much cash your portfolio must generate each year.

- List all your annual expenses. Include everything from essentials like your mortgage, property taxes, and healthcare premiums to discretionary spending like travel, dining out, and hobbies.

- Subtract your guaranteed income sources. Add up any income you receive from Social Security, pensions, or annuities.

- Calculate your withdrawal need. The final number is the amount your portfolio must generate each year to cover your lifestyle.

For example, if your annual expenses are $80,000 and you receive $30,000 from Social Security, your portfolio needs to provide $50,000 per year.

Step 2: Define and Fund Your Buckets

With your annual need calculated, you can now structure your three buckets. Using our $50,000 example:

Bucket 1 (Short-Term: 1-3 Years)

This is your liquidity bucket, designed for capital preservation above all else. It ensures your income for the immediate future is safe from market risk.

- Purpose: Cover 1 to 3 years of living expenses.

- Funding: $50,000 to $150,000.

- Typical Assets:

- Cash

- High-yield savings accounts

- Money market funds

- Short-term CDs

Bucket 2 (Mid-Term: 4-10 Years)

This is your stability bucket. Its job is to generate modest returns and be ready to refill Bucket 1 without the volatility of an all-stock portfolio.

- Purpose: Cover living expenses for years 4 through 10.

- Funding: Approximately $350,000 (7 years x $50,000).

- Typical Assets:

- High-quality corporate or municipal bonds

- Bond funds (e.g., a total bond market index)

- Conservative balanced funds (e.g., 40% stocks, 60% bonds)

Bucket 3 (Long-Term: 11+ Years)

This is your growth engine. Since you won't need this money for over a decade, it can be invested more aggressively to generate the long-term returns needed to replenish the other two buckets and outpace inflation. Historically, the S&P 500 has provided an average annual return of over 10% since 1928, though it's critical to remember that past performance doesn't guarantee future returns.

- Purpose: Long-term growth to sustain the portfolio for decades.

- Funding: The remainder of your portfolio.

- Typical Assets:

- Diversified domestic stock funds (e.g., S&P 500 index funds)

- International stock funds

- Other growth-oriented assets

Customizing Your Buckets: Common Approaches

The classic three-bucket model is a great starting point, but it can be tailored to your personal preferences and financial situation.

The Expense-Based Approach

Instead of segmenting by time, some retirees prefer to structure their buckets around the type of expense they cover.

- Bucket 1 (Essential Needs): Covers non-negotiables like housing and healthcare, funded by conservative investments and guaranteed income.

- Bucket 2 (Discretionary Wants): Funds lifestyle expenses like travel and hobbies, using a moderate-risk investment profile.

- Bucket 3 (Legacy Goals): Holds funds for inheritance or charity, invested for maximum long-term growth.

The Two-Bucket or Four-Bucket Simplification/Expansion

Some people find three buckets to be too many or too few. The framework is flexible enough to be simplified or expanded.

A Two-Bucket Model offers simplicity, with a "Now" bucket for 5-7 years of expenses in conservative assets and a "Later" bucket for everything else invested for growth.

Alternatively, a Four-Bucket Model provides more granular control by splitting the mid-term bucket into two distinct time horizons, such as one for years 3-5 and another for years 6-10.

Key Factors in Managing Your Bucket Strategy

The bucket strategy is a dynamic plan, not a "set it and forget it" solution. It requires ongoing management to work effectively.

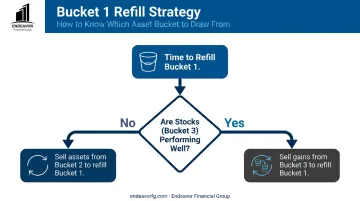

The Rebalancing and Replenishing Process

The key to the strategy's success is the disciplined process of refilling Bucket 1. This process should happen systematically, typically once a year.

- Use new income first. Any interest or dividends generated by Buckets 2 and 3 should be your first source for refilling your cash bucket.

- Sell appreciated assets. If more cash is needed, you can tap your growth bucket. If stocks have had a good year, sell some of the gains from Bucket 3 and transfer the cash to Bucket 1. This is the "sell high" discipline in action.

- Use Bucket 2 if needed. If stocks are down, you can avoid selling them at a loss. Instead, you can sell assets from your more stable Bucket 2 to replenish your cash, giving your stocks time to recover.

Adapting to Market Conditions and Life Changes

Your plan is a living document, not a static report. That's why it's essential to conduct periodic reviews—at least annually—with a fiduciary financial advisor to adjust for:

- Inflation: Your withdrawal needs may need to increase to maintain your purchasing power.

- Spending Changes: A major health event or a decision to travel more (or less) will impact your income needs.

- Market Performance: A prolonged bull or bear market may require adjustments to your asset allocation within the buckets.

Common Issues and When to Reconsider the Bucket Strategy

While the bucket strategy is effective, its success depends on proper implementation and avoiding a few common pitfalls. Potential issues to watch for include:

- Operational Complexity: Buckets don't require separate accounts, but managing allocations, tracking performance, and rebalancing within existing accounts requires discipline.

- Cash Drag: Holding too much cash in Bucket 1 can hinder portfolio growth during bull markets. Fidelity notes a hypothetical $5,000 annual investment from 1980 to 2023 would have grown to $349,999 in cash versus over $4 million in stocks.

- Inaccurate Projections: The strategy relies on precise expense estimates. Over- or under-estimating your spending needs can compromise the entire structure.

A framework like the bucket strategy is an excellent tool, but it requires tailoring to your specific goals, risk tolerance, and tax situation. Working with a fee-only, fiduciary financial planner can help you build and maintain a robust plan that accounts for these variables.

At Endeavor Financial Group, our comprehensive five-step planning process—from discovery and analysis to implementation and ongoing monitoring—ensures your strategy is both well-designed and diligently managed for the long term.

Frequently Asked Questions

What is the 3 bucket approach to retirement?

It's a strategy that divides your retirement savings into three pools: a short-term bucket (1-3 years of expenses in cash), a mid-term bucket (4-10 years in bonds/balanced funds), and a long-term bucket (11+ years in stocks) to balance income needs with growth.

How is the bucket strategy different from the 4% rule?

The 4% rule is a guideline for your starting withdrawal rate. The bucket strategy is a portfolio structure that helps source those withdrawals, protecting you from selling assets at the wrong time.

How often should I rebalance my retirement buckets?

Most financial planners recommend reviewing and rebalancing your buckets annually. You might also replenish your cash bucket whenever it falls below a set threshold, such as one year's worth of living expenses.

What is sequence of returns risk?

It is the risk that a major market downturn in the first few years of your retirement can severely damage your portfolio. Making withdrawals from a declining asset base can permanently reduce your long-term financial security.

Can I have more or fewer than three buckets?

Yes, the strategy is flexible. While three buckets is the most common model, you can simplify it to a two-bucket system ("Now" and "Later") or expand it to four or more for greater control over your assets.