This guide is designed to demystify the upcoming changes. We’ll break down what’s happening, why it matters to you, and outline proactive, advanced strategies you can implement now. The goal is simple: to help you preserve your hard-earned wealth for the people and causes you care about most.

TL;DR: Key Takeaways for Your 2026 Estate Plan

TL;DR: Key Takeaways for Your 2026 Estate Plan

- The federal estate tax exemption will be cut in half on Jan. 1, 2026, exposing more assets to a 40% tax.

- Act before the deadline to lock in today's historically high exemption levels and minimize future taxes.

- Utilize key strategies like gifting, Spousal Lifetime Access Trusts (SLATs), and ILITs to protect assets.

- Leverage valuation discounts to transfer business interests more tax-efficiently.

- Coordinate with your financial advisor, attorney, and CPA to ensure your plan is successful.

The 2026 Estate Tax Cliff: Why High-Net-Worth Families Must Act Now

The Tax Cuts and Jobs Act (TCJA) of 2017 nearly doubled the federal estate tax exemption. However, this increase was temporary. A "sunset" provision in the law means that on January 1, 2026, the exemption amount will revert to its pre-2018 level, adjusted for inflation.

The current rules are generous. In 2024, an individual can transfer $13.61 million to heirs free from federal estate taxes, and a married couple can shield over $27 million. After 2025, however, this exemption is projected to be cut nearly in half to approximately $7 million per person.

The Financial Impact of Inaction

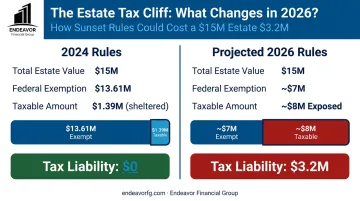

What does this mean in real dollars? Consider a hypothetical estate valued at $15 million.

- Under 2024 Rules: With an individual exemption of $13.61 million, the entire $15 million estate is sheltered from federal tax. The tax liability is $0.

- Under Projected 2026 Rules: The exemption drops to ~$7 million, leaving $8 million of the estate exposed. At the top 40% federal rate, this creates a potential tax bill of $3.2 million.

This is a "use it or lose it" scenario. Fortunately, the IRS has issued "anti-clawback" regulations. This means that large gifts made now using the current high exemption will not be penalized or "clawed back" into your estate if you pass away after the exemption amount drops.

This change doesn't just affect the ultra-wealthy. Decades of asset growth, real estate appreciation, and rising business values will push many families over the lower 2026 threshold, creating unexpected tax burdens.

Key Estate Tax Planning Strategies to Consider Before 2026

While many tools are available, a few strategies are particularly effective for leveraging the current tax environment. These techniques can help you transfer significant wealth now, removing it—and its future appreciation—from your taxable estate.

Foundational Strategy: Strategic Annual and Lifetime Gifting

This is the bedrock of most estate plans. It’s important to understand the two primary tools for gifting:

- Annual Gift Tax Exclusion: In 2024, you can give up to $18,000 to as many individuals as you like each year without filing a gift tax return or using your lifetime exemption. A married couple can combine their exclusions to gift $36,000 per recipient. Over several years, this can move a substantial amount of wealth to children and grandchildren tax-free.

- Lifetime Gift Tax Exemption: This is the $13.61 million amount set to decrease in 2026. Making large gifts now uses this exemption to remove those assets and all their future growth from your estate. For example, if you gift $1 million in stock that later grows to $3 million, that entire amount is outside your taxable estate.

Advanced Strategy 1: The Spousal Lifetime Access Trust (SLAT)

A Spousal Lifetime Access Trust (SLAT) is a powerful but complex tool for married couples. It's an irrevocable trust that one spouse (the donor) creates and funds for the benefit of the other spouse (the beneficiary), effectively removing the assets from both of their estates.

Key benefits of a SLAT include:

- Uses the Exemption Now: The donor spouse uses their lifetime gift tax exemption to fund the trust, locking in today's high amount.

- Maintains Indirect Access: The beneficiary spouse can receive distributions from the trust, providing a financial safety net. This makes it a popular choice for couples who want to plan ahead but are hesitant to give up access to assets completely.

- Creditor Protection: Assets held in a properly structured irrevocable trust are typically shielded from future creditors.

A critical note: To avoid IRS challenges under the "reciprocal trust doctrine," each spouse's SLAT (if both create one) must have meaningful differences in its terms.

Advanced Strategy 2: The Irrevocable Life Insurance Trust (ILIT)

An Irrevocable Life Insurance Trust (ILIT) is a trust created specifically to own a life insurance policy. When structured correctly, it ensures the policy's death benefit is paid to your heirs completely free of estate taxes.

Its primary function is to create liquidity. When an estate owes taxes, heirs often have to sell assets—like a family home or a business—to pay the bill. An ILIT provides an immediate, tax-free source of cash to cover these expenses, preserving the assets you intended to pass on.

The trust is typically funded through annual gifts, which the trustee uses to pay the policy premiums.

Special Considerations for Business Owners

If you own a closely-held business or have a family limited partnership (FLP), you have a unique and powerful planning opportunity: valuation discounts. When you gift minority, non-controlling interests in a private company, the value of that gift for tax purposes can often be discounted.

The two most common discounts are for lack of control, reflecting a minority shareholder's inability to direct business decisions, and lack of marketability, which accounts for the difficulty of selling a private company interest.

These discounts allow you to transfer more underlying business value while using less of your lifetime exemption. For example, a stake in your company with a paper value of $100,000 might be appraised at just $75,000 for gift tax purposes after a combined 25% discount. This strategy effectively moves more wealth out of your taxable estate.

However, these discounts can attract IRS scrutiny. You must obtain a formal business valuation from a qualified appraiser to substantiate your claims, a process your financial advisory team can help coordinate to ensure it aligns with your overall estate plan.

Building Your Roadmap: How to Implement Your Estate Tax Strategy

These advanced strategies are not DIY projects. Executing them successfully requires a coordinated team of professionals, including an estate planning attorney, a CPA, and a financial advisor.

Think of your financial advisor as the "quarterback" of this team. While an attorney drafts the legal documents and a CPA handles tax filings, your advisor understands your complete financial picture. They ensure the strategies chosen align with your investment portfolio, retirement goals, and overall life plan.

A structured implementation process ensures legal documents are not just created, but are also properly funded and integrated. At Endeavor Financial Group, our role is to connect those legal structures to your real-world finances.

This involves several key steps:

- Funding the trusts and integrating them with your investment portfolio.

- Aligning beneficiary designations across all retirement and insurance accounts.

- Monitoring the plan to ensure every component works together seamlessly.

Frequently Asked Questions

What is the federal estate tax exemption for 2026?

The exemption is scheduled to decrease significantly, reverting to its pre-2018 level (adjusted for inflation). Projections place it at approximately $7 million per individual.

What is the difference between an estate tax and an inheritance tax?

An estate tax is paid by the deceased's estate before assets are distributed to heirs. An inheritance tax is paid by the beneficiaries who receive the assets. The federal government has an estate tax; only a few states have an inheritance tax.

Can I simply gift my assets to my children to avoid estate tax?

Yes, but it has drawbacks. Gifts over the $18,000 annual exclusion count against your lifetime exemption. You also lose control over the asset, and your children forfeit the valuable “step-up” in basis they would receive upon your death.

How can a trust help reduce estate taxes?

An irrevocable trust can own assets outside of your personal estate. This means the assets in the trust, and all their future growth, are generally not subject to estate tax when you pass away.

Is it too late to start estate tax planning for 2026?

No, but the window of opportunity is closing. Acting now provides the necessary time to develop a sound strategy, draft legal documents, and properly transfer or re-title assets before the law changes.