Investing Tips for High-Net-Worth Individuals in 2026

Navigating Your Wealth in 2026: Top Investing Strategies for High-Net-Worth Individuals

Standard investment advice is great for building wealth, but it often falls short when you’re managing it. For high-net-worth individuals (HNWIs), the game changes. Your financial picture involves complex tax situations, concentrated assets, and long-term legacy goals that a simple stocks-and-bonds portfolio can’t address alone.

The primary goal is no longer just accumulation; it's about sophisticated preservation. You need to protect what you’ve built from tax erosion, market volatility, and inefficient wealth transfer. This requires a different playbook—one focused on advanced portfolio construction, proactive tax minimization, and integrated estate planning tailored for the 2026 economic landscape.

TLDR: Key Investment Strategies for HNWIs in 2026

Go Beyond Stocks and Bonds: Diversify with alternative investments like private equity and real estate to reduce public market correlation.

Prioritize Tax Efficiency: Use strategies like asset location and tax-loss harvesting to protect returns from tax drag.

Integrate Legacy Planning Now: Make estate and philanthropic planning an active part of your wealth strategy, not an afterthought.

Focus on Holistic Risk Management: Actively manage unique HNWI risks, such as concentrated stock or business ownership.

Work with a Coordinated Team: Assemble a team of wealth, tax, and legal experts to manage financial complexity.

What Makes High-Net-Worth Investing Different in 2026?

For high-net-worth individuals, the focus shifts from wealth accumulation to sophisticated wealth preservation and transfer. The biggest threats to your financial legacy are often taxes, inflation, and inefficient planning—not just market downturns. This challenge is amplified by the unique circumstances many successful individuals face.

For Executives

The primary risk is often over-concentration in company stock. Key challenges include:

Navigating the high stakes of having too much net worth tied to a single company.

Managing complex tax rules and timing decisions for stock options (ISOs and NSOs).

For Business Owners

Personal and business finances are deeply intertwined for company founders. This leads to challenges like:

Balancing reinvestment in the business with growing a personal portfolio.

Creating a smart succession plan for the company's future.

Preparing for an eventual liquidity event, such as a sale or IPO.

Navigating these high-stakes decisions requires a clear view of the economic environment. In 2026, the Federal Reserve's median projection for the federal funds rate is 3.4%, with PCE inflation expected to be around 2.7% according to the CBO. While the interest rate environment has stabilized, strategic planning remains critical to protect and grow your wealth effectively.

Core Strategy 1: Beyond Public Markets: Advanced Portfolio Construction for 2026

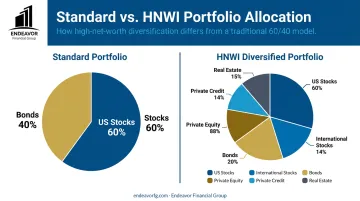

The traditional 60/40 portfolio of stocks and bonds has long been a staple, but its reliability has been tested. During the market downturn of the 2020s, a 60/40 portfolio experienced more "pain" (a combination of decline depth and duration) than an all-equity portfolio for the first time in 150 years, according to Morningstar.

For HNWIs, this signals a clear need to look beyond public markets for true diversification and portfolio resilience.

Incorporating Alternative Investments

Alternative investments offer a way to diversify away from public markets and access unique return streams that aren't tied to the daily swings of the S&P 500.

Invest in private equity to access pre-IPO company growth, but be prepared for longer lock-up periods and higher complexity.

Explore private credit by lending directly to companies, a strategy that can offer higher yields than traditional bonds.

Consider direct real estate to generate steady income and access significant tax advantages, such as depreciation deductions.

Beyond adding private assets, diversifying your public market holdings is equally crucial for building a resilient portfolio.

The Role of Global Diversification

Even within public markets, a U.S.-centric portfolio may carry unseen risks. The U.S. market is highly concentrated, with the top 10 companies in the S&P 500 making up 37% of the total market capitalization as of early 2026.

Expanding globally can hedge against domestic economic risks and capture growth in different cycles. Research from Vanguard shows that portfolio volatility has historically been reduced most with an international equity allocation between 35% and 55%. International and emerging markets offer different opportunities and can provide a crucial layer of diversification for a robust HNWI portfolio.

Core Strategy 2: Mastering Tax Efficiency: The Cornerstone of Wealth Preservation

For most high-income individuals, taxes are the single largest recurring expense. Making your portfolio as tax-efficient as possible isn't just a minor optimization—it's a primary driver of your net returns.

Foundational Tax-Reduction Techniques

Before exploring advanced strategies, ensure these fundamental techniques are part of your financial plan.

Locate assets strategically by placing income-generating investments like bonds in tax-deferred accounts (401(k)s, IRAs) and keeping tax-efficient index funds in standard brokerage accounts.

Harvest tax losses year-round by selling underperforming investments to offset capital gains elsewhere in your portfolio. This isn't just a year-end task; it's a continuous, disciplined strategy.

Advanced Strategies for Significant Tax Savings

For those with substantial wealth, more advanced tools can help preserve assets for your family and charitable causes.

Give charitably with appreciated assets, such as stocks, by donating them directly to a charity or a Donor-Advised Fund (DAF). You can receive a full market-value deduction while avoiding capital gains taxes.

Transfer wealth using advanced trusts like GRATs or IDGTs. These powerful tools help move asset appreciation to the next generation while minimizing gift and estate tax liabilities.

Implementing these trust strategies is not a DIY project; it requires careful coordination between your financial advisor, tax professional, and an estate attorney. At Endeavor Financial Group, our advisors act as the "quarterback" for your financial team, ensuring all investment, tax, and legal strategies work in unison.

Integrating Estate, Legacy, and Philanthropic Goals

For HNWIs, estate planning isn't something you do once and forget about. It's an active, ongoing part of your overall financial strategy. A key component of this strategy in 2026 is utilizing the federal estate tax exemption.

For 2026, the federal estate tax exemption is $15,000,000 per individual. This means you can pass up to this amount to your heirs without triggering the federal estate tax, which stands at a steep 40%. This generous exemption allows for significant lifetime gifting strategies to reduce the size of your future taxable estate.

Philanthropy is also a powerful tool for building a family legacy while meeting tax objectives. Integrating charitable giving strategies, such as Donor-Advised Funds (DAFs), into your estate plan allows you to:

Support the causes you care deeply about

Engage your family in a shared mission

Optimize your overall tax situation

Coordinating these elements with a financial advisor helps ensure your philanthropic goals align with your broader financial and legacy strategy.

How a Comprehensive Financial Plan Ties It All Together

These advanced strategies—alternative investments, tax optimization, and estate planning—are not standalone tactics. They are interconnected pieces of a larger puzzle. The only way to ensure they work in harmony is through a comprehensive, integrated financial plan.

This requires working with a financial advisor who takes a holistic, consultative approach and is committed to understanding your entire financial picture. At Endeavor Financial Group, we use a structured five-step process to provide our clients with a clear roadmap.

Discovery Meeting: We start by identifying your goals and priorities to ensure our consultative approach is the right fit for your needs.

Analysis & Strategy Development: Our team takes a deep dive into your complete financial picture, analyzing every component to develop a strategic roadmap.

Plan Presentation & Refinement: We present your comprehensive financial plan and work with you to refine the details, ensuring you are confident in every step.

Implementation: Once you approve the plan, we put the strategies into action, coordinating with other professionals like attorneys and accountants as needed.

Ongoing Monitoring & Support: We continuously monitor your plan and adapt it as your life and goals evolve, providing proactive advice to keep you on track.

This structured process provides the clarity and confidence needed to navigate the complexities of significant wealth. If you're ready to build a plan that preserves your wealth and secures your legacy, schedule a consultation with the Endeavor Financial Group team today.

Frequently Asked Questions

What net worth is considered wealthy in 2026?

While definitions vary, "high-net-worth" (HNW) is typically defined as having $1 million or more in liquid, investable assets. The next tier, "ultra-high-net-worth" (UHNW), generally starts at $30 million in investable assets.

What percentage of Americans have a net worth of over $1,000,000?

According to the Federal Reserve's 2022 Survey of Consumer Finances, about 16 million American families, or just over 12% of all households, had a net worth of $1 million or more.

How do billionaires plan to invest in 2026?

Billionaires and family offices often prioritize alternative investments like private equity, real estate, and private credit. For instance, a 2025 UBS report noted that U.S. family offices allocate over half of their portfolios to these areas, moving beyond just public stocks and bonds.

What is the best investment for your money in 2026?

There is no single "best" investment, as the optimal strategy depends on your personal goals, risk tolerance, and tax situation. The most effective approach is always a customized, comprehensive financial plan tailored to your needs, not a specific product or stock.