What if there was a simple, low-tech way to stress-test your strategy? In the world of software development, programmers use a quirky but effective method called "rubber duck debugging." The idea is that by explaining a problem out loud to an inanimate object, like a rubber duck, you're forced to articulate your thought process step-by-step, often revealing the solution yourself.

This same principle can be a powerful tool for your retirement finances. This article will show you how to use the "Rubber Duck Rule" to challenge common assumptions, find dangerous gaps in your tax plan, and prepare yourself for a smarter conversation with a financial professional.

TL;DR: The Rubber Duck Rule for Retirement Taxes

- Challenge Assumptions: Your tax bracket may not be lower in retirement due to RMDs and expiring tax laws.

- Uncover Hidden Gaps: Watch out for stealth taxes like the "widow's penalty" and Medicare IRMAA surcharges.

- Structure Your Withdrawals: Use a "bucket strategy" to pull from taxable, tax-deferred, and tax-free accounts in the right order.

- Know When to Get Help: The duck helps you find the questions; a professional helps you find the answers.

What Is the Rubber Duck Rule of Retirement Tax Planning?

The concept originated in software engineering. When a programmer is stuck on a piece of code that isn't working, they grab a rubber duck, place it on their desk, and explain the code to it, line by line.

The duck doesn't need to understand programming—the value comes from the act of explaining. By vocalizing their logic, the programmer often spots the flaw in their own reasoning.

Translating this to retirement planning is simple. Your goal is to explain your entire strategy for generating income and minimizing taxes to a non-judgmental listener—your "duck." This forces you to move from vague ideas like "I'll live off my 401(k)" to a concrete, step-by-step process.

The psychological benefits are significant. This process helps you:

- Challenge your own long-held beliefs

- Uncover gaps in your knowledge

- Organize your thoughts without the fear of asking a "stupid question"

You're just talking to a duck.

Challenging Your Assumptions: The First Conversation with Your Duck

Let's start by testing the most common assumptions people make about retirement taxes. Explain your reasoning for each of these points to your duck, out loud.

Assumption 1: "My tax bracket will be lower in retirement."

This is the bedrock of traditional retirement advice, but it's not a guarantee. Explain to your duck why you believe this. List every source of income you expect: pensions, Social Security, part-time work, and withdrawals from your retirement accounts.

Now, consider the forces that can push your income—and your tax bracket—higher than you expect.

- Required Minimum Distributions (RMDs): At age 73, the IRS generally requires you to start taking distributions from traditional 401(k)s and IRAs. These withdrawals are taxed as ordinary income and can be substantial, easily pushing you into a higher tax bracket.

- The 2026 "Tax Cliff": Many lower tax rates from the Tax Cuts and Jobs Act are set to expire at the end of 2025. If Congress doesn't act, rates will revert to higher pre-2018 levels, a change the Congressional Research Service notes would affect nearly everyone.

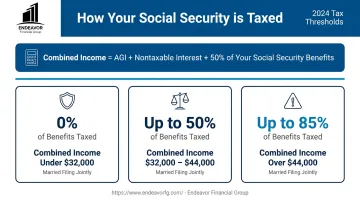

Assumption 2: "My Social Security benefits won't be heavily taxed."

Next, tell your duck how Social Security fits into your income plan. Many retirees are shocked to learn that their benefits can be taxable. The IRS determines this based on your "combined income," which is a specific formula:

Combined Income = Adjusted Gross Income (AGI) + Nontaxable Interest + 50% of Your Social Security Benefits

The Social Security Administration uses this number to determine how much of your benefit is taxed. For 2024, if your combined income as a couple is over $44,000, up to 85% of your Social Security benefits could be subject to federal income tax.

Assumption 3: "I don't need to worry about RMDs until I turn 75."

This is a common point of confusion due to recent law changes. The current RMD age is 73 for individuals born between 1951 and 1959. The age will eventually shift to 75, but only for those born in 1960 or later.

Explain your RMD start date to the duck. Planning for these mandatory withdrawals is critical because they can trigger higher taxes on your Social Security benefits and even increase your Medicare premiums. And the penalty for failing to take an RMD is steep: a 25% excise tax on the amount you failed to withdraw.

Uncovering Hidden Gaps: Deeper Questions for Your Tax Plan

Once you've tested your core assumptions, it's time to dig deeper. These are the tax traps that often catch even diligent planners by surprise.

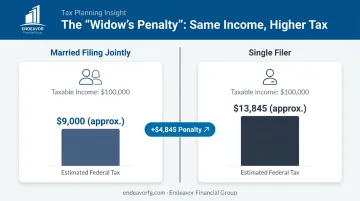

Gap 1: The "Widow's Penalty"

This is a tough but essential scenario to plan for. Walk your duck through what happens to your household's tax situation if one spouse passes away. The surviving spouse must switch from filing "Married Filing Jointly" to "Single."

As Kiplinger explains, this "widow's penalty" can be financially devastating. The standard deduction is cut in half, and the tax brackets become much narrower for a single filer.

However, the surviving spouse's income from pensions and Required Minimum Distributions (RMDs) from retirement accounts often remains nearly the same. The result is that same income gets taxed at a much higher rate.

For example, a household with $100,000 in taxable retirement income might pay around $9,000 in federal taxes. A single filer with that same income could face a tax bill of nearly $14,000.

Gap 2: Medicare Premium Surcharges (IRMAA)

Explain to your duck how you plan to manage healthcare costs. Most people don't realize that Medicare Parts B and D premiums can increase based on your income. This is called the Income-Related Monthly Adjustment Amount, or IRMAA.

These surcharges are based on your Modified Adjusted Gross Income (MAGI) from two years prior. A single large income event—like a significant Roth conversion, selling a business, or a large IRA withdrawal—can trigger these higher premiums for an entire year, costing you thousands of dollars.

Gap 3: Inefficient Charitable Giving

If you plan to be charitable in retirement, explain your giving strategy. Many people simply write a check, but there's a much more tax-efficient way.

For those aged 70½ and older, a Qualified Charitable Distribution (QCD) is a powerful tool. A QCD allows you to donate up to $105,000 (for 2024) directly from your IRA to an eligible charity. This has two huge benefits:

- The distribution is not included in your taxable income.

- It can count toward your RMD for the year.

This strategy lowers your adjusted gross income, which can help you avoid IRMAA surcharges and reduce the tax on your Social Security benefits.

Gap 4: The Roth Conversion Blind Spot

Finally, explain your strategy for your tax-deferred (Traditional IRA/401k) versus your tax-free (Roth IRA) accounts. A common blind spot is failing to consider Roth conversions during the "gap years"—the period after you retire but before RMDs and Social Security begin.

During these potentially low-income years, you can strategically convert a portion of your traditional IRA to a Roth IRA. You'll pay ordinary income tax on the converted amount now, at what might be your lowest tax rate.

In exchange, that money grows tax-free forever and is not subject to RMDs. This gives you a flexible bucket of tax-free cash for later in retirement.

Building Your Tax-Efficient Withdrawal Strategy

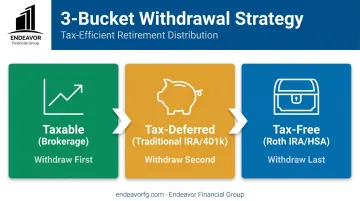

After talking to your duck, you've likely identified some weak spots. The next step is to structure a smarter withdrawal plan. A common and effective framework is the "bucket strategy," which organizes your assets by their tax treatment.

Bucket 1: Taxable Accounts (Brokerage)

Assets in standard brokerage accounts are typically the first you should tap into. You draw from this bucket first because you've already paid taxes on dividends and interest, and long-term capital gains are taxed at preferential rates (0%, 15%, or 20%)—often lower than ordinary income rates.

Bucket 2: Tax-Deferred Accounts (Traditional IRA/401k)

Your tax-deferred accounts are generally the second source of funds. Since withdrawals are taxed as ordinary income, the goal is to manage them carefully. Pull just enough to meet your needs while staying within a target tax bracket, giving you significant control over your annual taxable income.

Bucket 3: Tax-Free Accounts (Roth IRA/HSA)

This bucket should be your last resort, as withdrawals are completely tax-free. This money is perfect for covering large, unexpected expenses or for years when other income sources push you into a higher tax bracket. It's also an excellent, tax-free asset to leave to heirs.

This sequence is a guideline, not a rigid rule. The most tax-efficient strategy often involves a flexible approach, drawing a little from multiple buckets in a given year to fine-tune your income.

When the Duck Isn't Enough: Partnering with a Financial Professional

The Rubber Duck Rule is a fantastic tool for self-discovery. It helps you organize your thoughts, challenge your assumptions, and identify the right questions to ask. But the duck can't give you answers, run complex tax projections, or build a personalized financial plan.

This is where your conversation with the duck ends and a conversation with a professional begins. The exercise prepares you to have a much more productive meeting with a financial advisor because you're no longer starting from scratch. You have a list of specific concerns about RMDs, the widow's penalty, and your withdrawal strategy.

A professional partner like Endeavor Financial Group is essential for turning those questions into an actionable plan. We work with pre-retirees and business owners in Indiana and across the country, using a consultative approach that includes:

- A five-step structured process from discovery to implementation and ongoing monitoring.

- Coordination with your existing tax and legal professionals to ensure all strategies are aligned.

- A holistic plan that addresses tax efficiency, income needs, and legacy goals.

Frequently Asked Questions

What is the 30-30-30-10 rule for retirement?

This is a general budgeting guideline, suggesting you allocate 30% of your income to housing, 30% to other living expenses, 30% to debt or lifestyle wants, and 10% to savings. It's more of a budgeting concept than a formal retirement planning rule.

How long will $500,000 last using the 4% rule?

The 4% rule suggests withdrawing $20,000 in your first year of retirement. However, the actual lifespan of your money depends on real-world factors like market returns, inflation, and your unique spending needs.

What are the three main "buckets" of retirement savings for tax purposes?

The three buckets are taxable (brokerage accounts), tax-deferred (Traditional IRA/401k), and tax-free (Roth IRA/HSA). Each is taxed differently upon withdrawal, allowing for strategic, tax-efficient retirement income planning.

How can a Roth conversion reduce my future tax bill?

A Roth conversion moves pre-tax funds from a traditional IRA to a post-tax Roth IRA. You pay income tax on the converted amount now, allowing all future growth and withdrawals to be completely tax-free while also reducing future RMDs.

Are my Social Security benefits taxable in retirement?

Yes, up to 85% of your benefits can be taxable depending on your "combined income." This figure includes your adjusted gross income (AGI), non-taxable interest, and half of your annual Social Security benefits.

What is the "widow's penalty" and how can I plan for it?

This refers to the tax increase a surviving spouse may face when their filing status changes to "Single," which has tighter tax brackets. Proactive planning, such as building tax-free assets through Roth conversions, can help reduce this impact.