This isn't just about who gets what. It's about preserving family relationships and ensuring your values endure. This article provides a clear roadmap for legacy planning, covering everything from essential documents to passing on your principles, so you can leave behind a legacy of confidence and peace of mind.

TL;DR: Key Steps to Secure Your Legacy

- Go Beyond Estate Planning: Legacy planning includes your values and life lessons, not just your financial assets.

- Establish Core Documents: A will, a revocable living trust, and powers of attorney are the non-negotiable foundations of your plan.

- Check Your Beneficiaries: Beneficiary designations on retirement accounts and insurance policies override your will—keep them updated.

- Communicate Clearly: Hold a family meeting and consider writing a legacy letter to explain your intentions and prevent future conflicts.

What is Legacy Planning and Why is it Critical for Retirees?

Many people use the terms "estate planning" and "legacy planning" interchangeably, but they represent two different levels of thinking. Understanding the distinction is the first step toward creating a truly meaningful plan for your future.

Estate Planning vs. Legacy Planning

Think of estate planning as the foundational blueprint. It's the legal and financial process of creating documents to manage and distribute your property after your death. This is the "what" of your plan:

- Who gets the house?

- How are the investment accounts divided?

- Who will be the executor of your will?

Legacy planning, on the other hand, is a more holistic approach. It builds on your estate plan by going further to consider your non-financial assets: your values, beliefs, life lessons, and philanthropic wishes.

It’s the "why" and "how" behind your decisions—for example, why you want to fund a grandchild's education or how you want your family business to continue operating with its core values intact.

The Unique Urgency for Retirees

Retirement marks a fundamental shift in your financial focus, moving from accumulation to preservation. This change makes legacy planning not just important, but urgent.

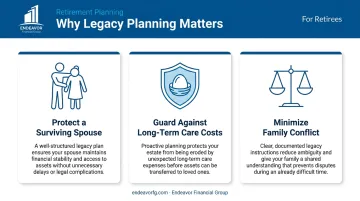

Protect a Surviving Spouse: After a lifetime together, ensuring your partner is financially secure is a top priority. A solid plan provides a clear framework for them to manage assets without unnecessary stress or financial shocks during an already difficult time.

Guard Against Long-Term Care Costs: The reality is that long-term care can quickly drain an estate. A private room in a nursing home can cost nearly $128,000 per year, according to AARP. With 56% of adults expected to need long-term care services, a legacy plan can use strategies like trusts or insurance to protect assets from these expenses.

Minimize Family Burden and Conflict: A lack of clear planning is a primary source of family conflict. A LegalShield survey found that 58% of people have experienced or know someone who has experienced family disputes over an estate. A well-communicated plan removes ambiguity, preventing your children from making difficult decisions under pressure and reducing the risk of relationship-damaging disputes.

The Core Components of a Comprehensive Legacy Plan

A strong legacy plan rests on a combination of essential legal documents and clear directives for your assets. Getting these elements right is crucial for ensuring your wishes are carried out smoothly.

The Foundational Documents

These legal documents form the bedrock of your plan, dictating how your affairs are handled both during incapacity and after your death.

- Last Will and Testament: This is the primary document for naming an executor, designating guardians for any minor dependents, and outlining the basic distribution of your assets. A will must go through probate—the court-supervised process of validating the will and distributing assets, which can take anywhere from 9 to 18 months.

- Revocable Living Trust: A trust is a powerful tool for avoiding probate. You transfer assets like your home or brokerage accounts into the trust, which you control as the trustee. Upon your death, a successor trustee distributes the assets per your instructions, bypassing the lengthy and public court process.

- Powers of Attorney: These documents are critical for managing your affairs if you become unable to do so yourself. A Financial Power of Attorney allows a person you designate to handle your financial matters, while a Medical Power of Attorney (or healthcare directive) empowers someone to make healthcare decisions on your behalf.

Directing Your Assets

Beyond a will or trust, several other tools directly control how specific assets are transferred, often allowing them to pass to your heirs much more quickly.

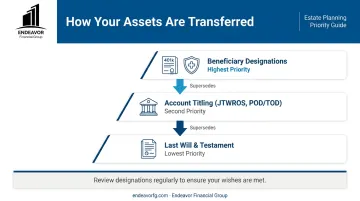

Review Your Beneficiary Designations

This is one of the most critical and often overlooked aspects of planning. The beneficiary designations on your retirement accounts (like 401(k)s and IRAs) and life insurance policies supersede your will.

If your will leaves everything to your children but your ex-spouse is still listed as the beneficiary on your IRA, your ex-spouse will get the funds. It is essential to review and update these forms after any major life event.

Strategic Account Titling

How you own property and bank accounts also matters. Certain types of titling can automatically transfer assets outside of probate:

- Joint Tenancy with Rights of Survivorship (JTWROS): When one owner dies, the asset automatically passes to the surviving joint owner.

- Payable on Death (POD) / Transfer on Death (TOD): These designations can be added to bank and brokerage accounts, respectively, to name a beneficiary who will inherit the account directly upon your death.

Advanced Strategies to Maximize Your Legacy

For those with larger estates or specific philanthropic goals, advanced strategies can help you protect your assets from taxes and make a lasting impact on the causes you care about.

Tax-Efficient Wealth Transfer

Federal and state estate taxes can significantly reduce the inheritance you leave behind. The federal estate tax exemption is historically high ($13.61 million per person in 2024), but it is scheduled to be cut roughly in half after 2025. Additionally, many states have much lower thresholds.

Here are a few common strategies to transfer wealth efficiently:

- Use the annual gift tax exclusion to give up to $18,000 (in 2024, indexed for inflation) to any number of individuals each year, reducing your taxable estate over time.

- Establish an Irrevocable Life Insurance Trust (ILIT) to hold a life insurance policy. This removes the death benefit from your taxable estate, providing a tax-free sum to heirs.

Charitable Giving and Philanthropy

Integrating charitable giving into your legacy plan can be a powerful way to support causes you believe in while also potentially reducing estate taxes. A 2024 Bank of America study found that 91% of wealthy Americans are supporters of charitable causes.

- Name a charity as a beneficiary in your will or trust for a simple direct bequest.

- Create a Charitable Remainder Trust (CRT) to receive an income stream for life, with the remainder passing to charity.

- Use a Donor-Advised Fund (DAF) to get an immediate tax deduction and recommend grants to charities over time.

Beyond the Documents: The Importance of Family Communication

Even the most perfectly drafted legal plan can create conflict if if it comes as a shock to your family, it can still create conflict. The "soft side" of legacy planning—communication—is just as important as the documents themselves.

A 2018 study by Merrill Lynch and Age Wave revealed that 59% of people believe passing on values and life lessons is the most important part of their legacy, more so than financial assets.

To ensure your plan is received as a gift of clarity, not a source of confusion, consider these steps:

- Hold a Family Meeting: This isn't about revealing numbers but explaining your intentions. Use this time to introduce your executor, share the location of key documents, and discuss the "why" behind your decisions. This manages expectations and prevents surprises.

- Write a Legacy Letter or "Ethical Will": This personal, non-legal document is your chance to share your values, life lessons, and hopes for the future. It provides context and meaning, helping heirs understand the principles behind the assets they inherit.

Building Your Legacy with a Trusted Partner

A successful legacy plan integrates legal, financial, and family dynamics—it's not a DIY project based on a downloaded form. It requires a holistic perspective that aligns every piece of your financial life with your ultimate goals.

At Endeavor Financial Group, we serve as your guide through this process. Our consultative approach focuses on understanding you, your values, and your vision first. We then use our comprehensive five-step structured process to build a clear roadmap that moves you from uncertainty to confidence.

- Understand your goals through an in-depth discovery conversation.

- Explore strategies and sketch a preliminary plan tailored to your situation.

- Create a detailed roadmap for your short- and long-term financial life.

- Implement your plan with our team standing by your side for support.

- Review and adapt your plan regularly as your life and goals evolve.

By coordinating with your legal and tax professionals, we ensure your financial plan is fully integrated with your legacy goals. Ready to create a lasting legacy that protects your assets and your family? Schedule a consultation with the Endeavor team today.

Frequently Asked Questions

What is the most common inheritance mistake?

Failing to update beneficiary designations after major life events like a divorce or death is a frequent error. This can cause assets to go to an unintended person, such as an ex-spouse, regardless of what your will says.

Which bank accounts avoid probate?

Accounts with "Payable on Death" (POD) or "Transfer on Death" (TOD) designations, or those held in "Joint Tenancy with Rights of Survivorship" (JTWROS), typically pass directly to the named beneficiary or co-owner, avoiding probate.

What is the difference between a will and a living trust?

A will is a document that directs asset distribution after death but must go through the court process of probate. A living trust holds and manages assets during your life and after death, allowing those assets to avoid probate.

How often should I review my legacy plan?

You should review your plan every 3-5 years or after a major life event. Key events include marriage, divorce, the birth of a grandchild, a beneficiary's death, or a significant change in your finances.

What is an "ethical will" and should I have one?

An ethical will is a non-legal letter that passes down your values, life lessons, and personal wishes. It’s highly recommended for anyone who wants to share their non-financial legacy and explain the meaning behind their planning decisions.

Do I need a legacy plan if I don't have a lot of wealth?

Yes. A plan ensures your wishes are known, names an executor, and helps prevent family disputes over personal items. It simplifies the process for your loved ones, no matter the size of your estate.