You're not alone in this. While 27% of Americans work with a financial advisor, many more hesitate, put off by confusing fee structures and a lack of price transparency.

This guide is here to change that. We're pulling back the curtain on financial advisor costs for 2026 to give you a clear, straightforward understanding of the different fee models, what drives the price, and how you can find the right expertise without overpaying.

TL;DR: Financial Advisor Costs

- Typical Cost Range: Most advisors charge a percentage of assets under management (AUM), typically 0.50% to 1.50% annually. Others use a flat fee, which can range from $2,500 to $10,000+ per year.

- What Drives the Price: Costs are primarily influenced by the amount of your assets, the complexity of your financial life (like business ownership or estate needs), and the scope of services you require.

- Key Fee Models: Common structures are AUM, flat annual fees, hourly rates, and commissions. Fee-only advisors, who operate as fiduciaries, eliminate the conflicts of interest found in commission-based models.

- Choosing Your Model: The AUM model often suits those wanting integrated investment management and planning. Flat fees are ideal for people who need project-based advice or predictable, holistic planning costs.

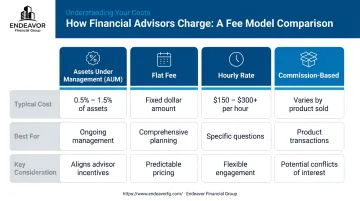

Understanding the Common Financial Advisor Fee Structures

Financial advisors use several fee structures, but most models fall into a few common categories. Knowing how an advisor gets paid is crucial for understanding their incentives and ensuring their interests are aligned with yours.

Assets Under Management (AUM) Fee

This is the most prevalent model in the industry. An advisor charges an annual percentage of the total assets they manage on your behalf. The typical industry range is between 0.50% and 1.50%.

For example, if you have a $1,000,000 portfolio and the AUM fee is 1%, you will pay $10,000 per year. This fee is usually tiered, meaning the percentage rate decreases as your assets cross certain thresholds (e.g., 1% on the first $1M, 0.80% on the next $1M, and so on).

- Best For: Investors with a sizable portfolio who want ongoing, integrated investment management and financial planning. The advisor's compensation grows as your portfolio does, creating a shared incentive for success.

Flat Fee / Fixed Fee

With a flat fee model, you pay a set price for a specific service or an annual retainer for ongoing advice. This could be a one-time fee for creating a comprehensive financial plan or an annual fee for continuous access to your advisor.

Annual flat fees typically range from $2,500 to $10,000+, depending on complexity. This fee often covers services like retirement analysis, tax strategy, and estate planning coordination, but it may or may not include the day-to-day management of your investments.

- Best For: Individuals who want a comprehensive financial plan but might prefer to manage their own investments. It's also great for those who value predictable, transparent costs that aren't tied to market performance.

Hourly Rate

Just like hiring an attorney or an accountant, some financial advisors charge by the hour for their time. This is a straightforward, pay-as-you-go model. Hourly rates for a qualified financial planner typically fall between $200 and $500 per hour.

This model makes sense for specific, targeted needs, such as:

A one-time portfolio review or "second opinion."

Getting advice on a specific issue, like exercising stock options.

Help with a particular financial decision, like a pension buyout analysis.

Best For: DIY investors who are comfortable managing their finances but need occasional, expert advice on specific issues without the commitment of an ongoing relationship.

Commission-Based

Commission-based advisors earn money by selling financial products like mutual funds, annuities, or insurance policies. This model creates a potential conflict of interest, as advice may be influenced by which product pays the highest commission, not which one is best for you.

Because of this potential conflict, it's important to understand two key terms:

- Fee-Based advisors use a hybrid model, earning both client fees and product commissions.

- Fee-Only advisors are compensated solely by client fees and accept no commissions, which is the fiduciary standard for minimizing conflicts of interest.

Key Factors That Influence Financial Advisor Costs

Regardless of the fee model, your final cost depends on a few key variables. Think of these as the dials that turn the price up or down.

Your Financial Complexity and Net Worth

A recent graduate with a single 401(k) has a much simpler financial situation than a business owner with multiple revenue streams, real estate, and a complex trust. Greater complexity requires more work and specialized expertise, which translates to a higher fee based on factors like business ownership, trusts, and intricate tax situations.

The Scope of Services Required

The services you need directly impact the cost. Are you looking for someone to simply manage your investment portfolio, or do you need a comprehensive financial plan?

Services that can increase the scope and cost include:

- Detailed retirement income planning

- Tax optimization and withdrawal strategies

- Business succession planning

- Estate planning coordination

- Insurance and risk management analysis

Advisor's Experience and Credentials

An advisor's qualifications and years of experience play a significant role in their fee structure. Certifications like CFP® (Certified Financial Planner) or CFA® (Chartered Financial Analyst) indicate a high level of expertise and a commitment to rigorous ethical standards. An advisor with decades of experience guiding clients through multiple market cycles can command higher fees than someone new to the industry.

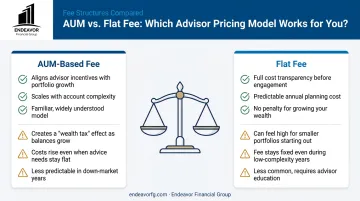

AUM vs. Flat Fee: Which Model is Right for You?

For most people seeking a long-term advisory relationship, the choice boils down to two primary models: Assets Under Management (AUM) or a flat annual fee. The best fit depends entirely on your personal needs, asset level, and what you value most in a professional relationship.

The Case for AUM

- Pros: Aligns your advisor’s success directly with your portfolio’s growth. The fee is simple to calculate and debited from your account, making payments seamless. It also offers a lower barrier to entry for those with smaller portfolios.

- Cons: Fees can become a "wealth tax" as your assets grow—a 1% fee is $10,000/year on a $1M portfolio but grows to $20,000/year on a $2M portfolio for similar work. This also creates a conflict in retirement, as an advisor may hesitate to recommend withdrawals that reduce their compensation.

The Case for a Flat Fee

- Pros: Offers total cost transparency and predictability, unaffected by market swings. Your fee is based on the complexity of the advice, eliminating the conflicts of interest tied to asset growth or withdrawals.

- Cons: The fixed cost can feel high for smaller portfolios compared to a low AUM percentage. You also have to pay the fee actively (e.g., by check or transfer), which feels more tangible than an automatic deduction.

AUM vs. Flat Fee: Key Differences

| Feature | Assets Under Management (AUM) | Flat Fee |

|---|---|---|

| Cost Structure | Percentage of your managed assets | Fixed annual or project-based price |

| Best For | Bundled investment management and ongoing advice | Complex, holistic advice with a predictable cost |

| Potential Conflicts | Discourages spending down assets in retirement | None directly tied to portfolio size |

| Predictability | Varies with market performance | High; fixed for the term of the agreement |

The right model isn't about which is universally "better," but which one aligns with your financial complexity, asset level, and the type of partnership you want with an advisor.

Beyond the Management Fee: Hidden Costs to Watch For

An advisor’s management fee is just one piece of the puzzle. To understand your "all-in" cost, you need to account for other expenses that can impact your returns. A great advisor will be transparent about these from the start.

Investment Expense Ratios

Every mutual fund and exchange-traded fund (ETF) charges an annual fee to cover its own operating expenses. This is called an expense ratio. These fees are separate from your advisor's compensation and are deducted directly from the fund's returns. While fees have come down, the average investor still paid around 0.42% in fund fees in 2024, according to Morningstar.

Trading and Custodial Fees

Some accounts may incur transaction fees for buying or selling securities. Additionally, the custodian—the firm that holds your assets, like Charles Schwab or Fidelity—may charge its own administrative fees, though these are becoming less common for retail investors.

Lack of Fiduciary Duty

Perhaps the biggest "hidden cost" isn't a fee at all—it's biased advice. A fiduciary is legally and ethically required to act in your best interest at all times.

In contrast, advisors who only follow a "suitability" standard (like many commission-based brokers) can recommend products that benefit them more than you. This conflict of interest can lead to you being sold high-commission, low-performance investments that cost you dearly in the long run.

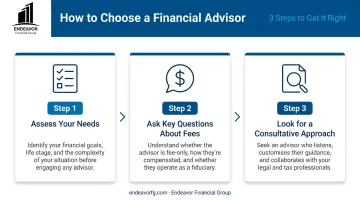

How to Choose an Advisor and Fee Structure That Fits Your Goals

Making a confident decision comes down to a clear process. Here are the steps you can take to find the right fit.

Assess Your Own Needs First

Before you start interviewing advisors, get clear on what you're looking for. Ask yourself:

- Do I primarily need someone to manage my investments, or do I need a strategic plan for retirement, taxes, and my estate?

- How hands-on do I want to be in the process?

- What are my most pressing financial concerns right now?

Ask These Questions About Fees

When you meet with a potential advisor, don't be shy about discussing compensation. This is a business relationship, and clarity is key.

- Are you a fiduciary at all times?

- How are you compensated? Are you fee-only, fee-based, or commission-based?

- Can you provide a full, written estimate of all fees I would pay, including your advisory fee and the underlying investment fees?

- How is your fee calculated, and when will I be billed?

Look for a Comprehensive, Consultative Approach

The best advisors don't lead with a fee structure; they lead with a process. They take the time to understand your unique situation before ever recommending a service or a product.

For example, firms like Endeavor Financial Group use a structured process to build a holistic financial plan first. Their initial steps focus on discovery—understanding your goals, priorities, and obstacles before discussing products or services.

This approach ensures the conversation about fees happens only after a clear roadmap is in place. As a result, the services and fee structure are tailored to your specific situation, whether you're planning for retirement income or creating a business exit strategy.

Frequently Asked Questions

What is a reasonable flat fee for a financial advisor?

A reasonable flat fee typically ranges from $2,500 to $10,000+ annually. The exact amount depends on the complexity of your financial situation and the depth of services provided.

What are red flags when choosing a financial advisor?

Key red flags include being evasive about fees, not committing to being a fiduciary, pressuring you to buy specific products, or promising guaranteed high returns (which is impossible).

What is the difference between a fee-only and a fee-based advisor?

A fee-only advisor is compensated solely by fees paid directly by their clients and does not accept commissions. A fee-based advisor can earn both client fees and sales commissions on products, creating potential conflicts of interest.

Is it worth paying a financial advisor 1% of my assets?

Yes, if the advisor provides value through comprehensive planning, tax optimization, and behavioral coaching that outweighs the cost. While research shows good advisors add value, a tiered or flat fee is often more cost-effective for large portfolios.

Do financial advisor fees come out of my investment returns?

AUM fees are typically deducted directly from your investment account, which reduces your net return. Flat fees are usually paid separately by the client via check or bank transfer.

Can I negotiate fees with a financial advisor?

While many advisors have a set fee schedule, some may have flexibility, especially for clients with very large portfolios or relatively simple needs. It never hurts to ask politely if there is any room for discussion.