You need sophisticated wealth management, but you also deserve to know your money is working for you—not just for your advisor. This article is for investors who have moved beyond basic portfolio management and are ready to redefine "affordable" as the best possible value, not just the lowest price.

We’ll break down the different ways advisors charge, uncover the hidden costs you might be paying, and give you a clear framework for choosing a service that truly enhances your financial life.

TL;DR

- For large portfolios, "affordable" is about value—tax planning, estate guidance, and strategic advice—not just the lowest fee percentage.

- Common fee models are Assets Under Management (AUM), flat annual fees, and hourly rates. AUM fees can become excessive for portfolios over $1 million.

- Always calculate the "all-in" cost, which includes advisor fees, underlying fund expense ratios, and any trading or platform costs.

- The right model depends on your need for comprehensive planning. High-net-worth individuals often get more value from flat-fee or holistic AUM models that include extensive planning services.

Why 'Affordable' Means More Than Just a Low Percentage

As your portfolio grows, you encounter the paradox of asset management: a standard percentage-based fee means you pay more in absolute dollars, often without a proportional increase in service. A 1% fee on a $500,000 portfolio is $5,000. On a $3 million portfolio, it's $30,000. Is the work six times harder? Rarely.

This is why savvy investors shift their focus to value-based affordability. A truly affordable service for a substantial portfolio is one that actively saves you money or generates value far beyond its own cost. The fee becomes an investment in financial efficiency, not just an expense.

This value comes from services that a simple investment manager might not provide:

- Strategic tax-loss harvesting to offset capital gains.

- Asset location optimization, placing investments in the right accounts (taxable, tax-deferred, tax-free) to minimize your tax bill.

- Coordinating with estate attorneys and CPAs to ensure your financial plan is fully integrated.

- Behavioral coaching during market downturns to prevent costly emotional decisions.

This isn't just theory. Research from Vanguard suggests that a comprehensive financial advisor can add approximately 3% in net returns over time through these value-added services, though this value is irregular and not guaranteed annually.

When an advisor's fee is 1%, but their tax and planning strategies are saving you 2%, the service isn't just affordable—it's profitable.

Decoding Asset Management Fee Structures

To find the best value, you first need to understand how advisors charge. Here’s a breakdown of the most common models and what they mean for a large portfolio.

The Traditional Assets Under Management (AUM) Model

In this common structure, the advisor charges a percentage of the total assets they manage. Fees are often tiered, meaning the percentage drops as your portfolio grows—for example, 1% on the first $1 million and 0.75% on the next $2 million.

- Pros: The advisor’s incentive is aligned with yours—when your portfolio grows, so does their compensation. It’s a simple and predictable structure.

- Cons: For large portfolios, fees can become excessive. A $2.5 million portfolio at a blended 0.85% rate costs $21,250 per year, regardless of service needs. Research from Michael Kitces shows average fees drop as assets increase, but you must ensure the value you receive scales with the cost.

The Flat-Fee Model

This model uses a fixed annual retainer for a defined scope of services, independent of your portfolio's size. Depending on your financial complexity, these fees typically range from $5,000 to over $20,000 annually.

- Pros: You get complete cost predictability, and your total fee is capped. This model shifts the focus from asset gathering to comprehensive planning, which is exactly what owners of large portfolios need.

- Cons: The fee is due regardless of market performance. For those just starting to build their wealth, it can seem more expensive upfront compared to a small AUM percentage.

Hourly and Project-Based Fees

These models are best for specific, one-off needs. You might hire an advisor for a few hours to review your portfolio, create a retirement projection, or analyze a specific investment.

- Pros: You only pay for the advice you need, when you need it. It’s a great option for DIY investors who want a professional check-up without committing to ongoing management.

- Cons: This model is not designed for continuous oversight. If you want a long-term partner to manage your assets and navigate life changes, this approach can become disjointed and less cost-effective.

The Hybrid or "Fee-Based" Model

It's crucial to distinguish between "fee-only" and "fee-based." A fee-only advisor is compensated solely by you, the client. A fee-based advisor can charge a fee (like AUM) but also earn commissions by selling financial products, such as insurance or annuities.

- Pros: Can offer one-stop shopping for both advice and products.

- Cons: This model creates a significant conflict of interest. Is your advisor recommending a product because it’s the best solution for you, or because they will earn a commission? This inherent conflict is why working with a fee-only fiduciary is critical for unbiased advice.

Calculating the All-In Cost of Managing Your Wealth

The fee you pay your advisor is just one piece of the puzzle. To make a true apples-to-apples comparison, you need to calculate the "all-in" cost of managing your wealth.

Here are the other costs to look for:

Underlying Investment Expenses

Your portfolio is likely built with mutual funds or Exchange-Traded Funds (ETFs), and each fund has its own internal management fee known as an expense ratio. This fee is separate from what you pay your advisor.

According to 2024 data from the Investment Company Institute, the average expense ratio for actively managed equity mutual funds was 0.64%, versus just 0.13% for index equity ETFs. This difference can have a massive impact on your net returns over time.

Platform and Custodial Fees

Some advisory platforms or custodians (the institutions that hold your assets, like Schwab or Fidelity) may charge their own administrative or "wrap" fees. These are often small but should be disclosed.

Trading or Transaction Costs

While less of an issue with modern, low-cost brokerages, frequent trading can still incur costs. Ask your advisor about their trading philosophy and any associated fees.

The bottom line: Your total annual cost is Advisor Fee + Fund Expense Ratios + Platform/Trading Fees. Don't settle for just the headline number.

How to Choose the Right Service Model for Your Portfolio

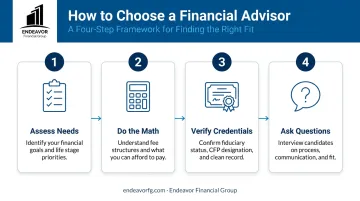

Choosing the right service model involves evaluating your financial complexity, comparing fee structures, and verifying an advisor's credentials. Follow these four steps to find the best fit.

Step 1: Assess Your Need for Comprehensive Planning

Start by assessing if you only need investment management or if you require integrated advice on taxes, retirement income, insurance, and your estate. The more complex your financial life, the more valuable a comprehensive planner becomes. If your needs go beyond the portfolio, a flat-fee or a holistic fee-only AUM advisor often provides the most value.

Step 2: Do the Math for Your Asset Level

Calculate what you are currently paying (or would pay) under a traditional AUM model. Compare that figure to the typical cost of a flat-fee advisor. A good rule of thumb comes from the White Coat Investor: if your AUM fee exceeds $10,000 per year, it's time to seriously explore flat-fee alternatives. For a $2 million portfolio, a 0.75% fee is $15,000—a price point where many excellent flat-fee advisors operate.

Step 3: Verify Fiduciary Status and Credentials

A fiduciary is legally and ethically bound to act in your best interest at all times. This is non-negotiable. Ensure any advisor you consider is a fee-only fiduciary.

Additionally, look for credentials that signal expertise in managing complex wealth:

- CFP® (Certified Financial Planner™): The gold standard for holistic financial planning.

- CFA® (Chartered Financial Analyst®): Indicates deep expertise in investment analysis and portfolio management.

- CPWA® (Certified Private Wealth Advisor®): Specializes in the challenges facing high-net-worth individuals.

Step 4: Ask Potential Advisors How They Justify Their Fee

A great advisor should clearly articulate their value. Ask these key questions:

- "What specific services do I receive for your fee beyond investment management?"

- "How do you measure the value you provide?"

- "Can you provide a transparent, all-in cost estimate, including underlying fund fees?"

- "How will you coordinate with my CPA and estate planning attorney?"

Your Partner in Strategic Wealth Planning

For investors with large portfolios, the most affordable asset management service isn't the cheapest—it's the one that delivers the most strategic value. True affordability comes from a partnership that optimizes your entire financial life, from minimizing taxes to securing your legacy.

At Endeavor Financial Group, we built our firm around this principle. Our approach is designed to provide strategic value through:

- A consultative method that starts with your goals, not just your assets.

- A holistic perspective that connects your business, family, and personal ambitions.

- A five-step structured process providing a clear roadmap from discovery to monitoring.

As fee-only fiduciaries, our only incentive is your success.

If you're looking for a partner to provide strategic wealth planning tailored to your unique goals, schedule a consultation with our team today.

Frequently Asked Questions

Is $500,000 enough to work with a financial advisor?

Yes, $500,000 is an excellent point to engage a professional advisor. This is often where financial complexity increases, and strategic planning around taxes, retirement, and investments becomes critical to long-term growth.

Where do millionaires keep their money if banks only insure $250,000?

Assets in brokerage accounts are typically protected by SIPC insurance up to $500,000 for securities and cash. Furthermore, these assets are held by a third-party custodian (like Schwab or Fidelity), not the advisory firm itself, providing an additional layer of protection.

How long will it take to turn $500,000 into $1 million?

The "Rule of 72" offers a simple estimate—divide 72 by your annual rate of return to see how long it takes to double. A comprehensive financial plan provides a more accurate timeline by factoring in contributions, returns, and fees.

What would be the best investment for $500,000?

There is no single "best" investment. The optimal strategy depends entirely on your personal goals, risk tolerance, and time horizon. This is precisely why personalized advice is essential to build a portfolio that is right for you.

What is the difference between a fee-only and fee-based advisor?

Fee-only advisors are paid only by their clients, eliminating commission-based conflicts of interest. Fee-based advisors can earn commissions from selling financial products, which may influence their recommendations.

Are asset management fees tax-deductible?

No. Following the Tax Cuts and Jobs Act of 2017, miscellaneous itemized deductions, which include investment advisory fees, are no longer deductible for individuals for tax years 2018-2025.