According to the Capgemini World Wealth Report 2026, the U.S. now has 8.7 million HNWI millionaires, after adding 736,000 in 2025 alone. Yet only 17% of those individuals describe their advisory experience as seamless and personalized — and 42% have to restate their goals to the same firm repeatedly.

That gap between wealth and quality guidance is exactly the problem this article addresses.

This guide covers:

- How HNWI and UHNWI tiers are defined — and why the distinction matters

- Why this level of wealth requires integrated planning, not siloed advice

- Core and advanced strategies that matter most at each tier

- What to look for when choosing a wealth manager

Key Takeaways

- HNWIs have $1M+ in investable assets; UHNWIs have $30M+, with meaningfully different planning needs at each tier

- Taxes, investments, estate plans, and business interests must be managed as one connected system — not separately

- U.S. family offices allocate 54% to alternatives, signaling how differently the ultra-wealthy invest

- 52% of wealthy Americans lack a basic estate plan — making delayed planning one of the costliest mistakes at this wealth level

- Work with a fiduciary who covers the full financial picture — not just the investment portfolio

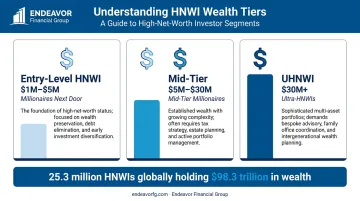

What Is an HNWI? Understanding the Wealth Tiers

The term "high-net-worth individual" has a specific, widely-used definition: someone with $1 million or more in liquid, investable assets, excluding the primary residence, collectibles, and consumer durables. This is the standard used by Capgemini and most institutional wealth managers — not total net worth.

The Three Tiers

| Tier | Investable Assets | Capgemini Label |

|---|---|---|

| Entry-level HNWI | $1M – $5M | Millionaires Next Door |

| Mid-Tier | $5M – $30M | Mid-Tier Millionaires |

| Ultra-High-Net-Worth (UHNWI) | $30M+ | Ultra-HNWIs |

These aren't just labels. The strategies, tools, and professionals suited to each tier are fundamentally different. A $2M portfolio and a $50M portfolio share little in common beyond the HNWI classification.

The scale of this population is substantial. Globally, 25.3 million HNWIs held $98.3 trillion in wealth at year-end 2025. That concentration of assets in relatively few hands is precisely why the strategies, professionals, and planning structures covered in this guide exist — and why applying the right approach to the right tier matters.

Why HNWI Wealth Management Is Different from Standard Financial Planning

Standard financial planning addresses most people's core needs: build savings, manage a portfolio, prepare for retirement. At higher wealth levels, the complexity multiplies — not because the goals change, but because the variables do.

Everything Is Connected

Tax decisions affect estate plans. Business income shapes investment strategy. Equity compensation interacts with AMT exposure. And something as routine as a retirement distribution sequence can shift your tax bracket, which in turn affects your Medicare premiums and cash flow projections simultaneously.

Financial decisions at this wealth level are rarely isolated. They require integrated, holistic planning where each element is designed to work with the others — not just optimized independently.

The Stakes Are Higher

- Market swings hit harder. A 10% portfolio drop on $5M is a $500,000 loss. Volatility that's manageable at lower wealth levels becomes consequential in ways that demand active risk management.

- Tax and legal errors are expensive. The top estate tax rate reaches 40% on taxable amounts, and the 2026 federal estate and gift tax exclusion is $15 million per individual. Mismanaging this window has permanent consequences.

- Income complexity grows. Business distributions, equity awards, rental income, and investment gains all interact in ways that demand more sophisticated cash flow management.

The Opportunity Set Expands

HNWIs gain access to investment vehicles unavailable to most: private equity, venture capital, hedge funds, and real estate syndications. These can improve diversification and long-term returns — but they require expertise to evaluate and manage responsibly. Without proper due diligence on liquidity constraints, fee structures, and risk profiles, expanded access can create exposure rather than protection.

Core Wealth Management Strategies for HNWIs

Tax Optimization

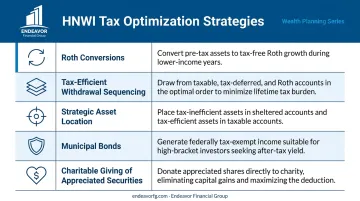

Proactive tax planning at the HNWI level happens year-round, not just at filing time. Key strategies include:

- Roth conversions — Moving funds from traditional IRAs to Roth accounts during lower-income years locks in current tax rates and eliminates future RMDs

- Tax-efficient withdrawal sequencing — Drawing from taxable, tax-deferred, and tax-free accounts in the right order to manage annual bracket exposure

- Strategic asset location — Placing less tax-efficient investments (corporate bonds, actively managed funds) in tax-advantaged accounts; holding index funds and municipal bonds in taxable accounts

- Municipal bonds — Generating income exempt from federal tax (and often state tax), especially valuable for clients in higher brackets

- Charitable giving of appreciated securities — Avoids capital gains while still generating a deduction

For business owners and executives, entity structuring through LLCs and S-corps adds another layer of planning opportunity — managing income flow, liability exposure, and self-employment taxes simultaneously. Federal and state tax law changes make this an area where ongoing professional guidance pays for itself.

Investment Diversification and Asset Allocation

A well-constructed HNWI portfolio goes well beyond a standard mix of stocks and bonds. Spreading allocations across multiple asset classes reduces volatility and creates more consistent long-term outcomes.

Asset classes typically considered at this wealth level:

- Public equities and fixed income (core)

- Real estate (direct ownership or REITs)

- Private equity and venture capital

- Hedge funds and liquid alternatives

- Private debt and infrastructure

94% of wealth managers already allocate to alternatives, and 44% allocate more than one-fifth of portfolios to them, according to Capgemini research. Critically, asset allocation should reflect your specific risk tolerance, time horizon, liquidity needs, and goals — not a generic model. Periodic rebalancing matters as much as initial construction.

Estate Planning and Wealth Transfer

A basic will isn't a plan. Estate planning at the HNWI level involves structures designed to minimize tax exposure across generations.

Core tools include:

- Revocable and irrevocable trusts — Control over asset distribution, potential estate tax reduction

- GRATs (Grantor Retained Annuity Trusts) — Transfer appreciation out of the taxable estate

- Family limited partnerships — Consolidate family assets with valuation discounts

- Annual gifting — The 2026 annual gift tax exclusion is $19,000 per donee

Despite the stakes, Bank of America research found 52% of wealthy Americans lack a basic estate plan — no will, no healthcare directive, no durable power of attorney. That gap has real consequences.

For business owners, estate planning must also address succession: who inherits equity, how a business transfer is structured, and how that intersects with family dynamics. Delayed planning is among the most costly mistakes HNWIs make.

Charitable Giving and Philanthropic Planning

Structured giving strategies can reduce taxable income while creating a lasting legacy:

- Donor-advised funds — Immediate tax deduction with the flexibility to distribute grants over time

- Charitable remainder trusts — Generate income during your lifetime; remainder passes to charity

- Gifts of appreciated securities — Transfer assets directly to a fund or charity, preserving full market value for the cause rather than losing a portion to capital gains.

Advanced Strategies for Ultra-High-Net-Worth Individuals

Private Investments and Alternative Assets

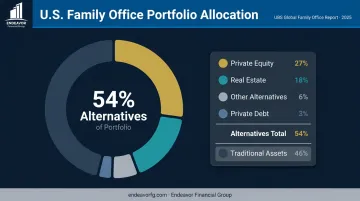

UHNW individuals routinely allocate over half their portfolios to alternatives. According to the UBS Global Family Office Report 2025, U.S. family offices allocated 54% to alternatives — including 27% to private equity, 18% to real estate, and 3% to private debt.

The trade-offs are real:

- Higher potential returns and diversification benefits

- Lower liquidity — capital can be locked up for years

- Longer holding periods requiring careful cash flow planning

- Greater due diligence burden — these aren't passive investments

Access to private markets is one of the clearest distinctions between UHNW and standard investor portfolios. Getting in without the operational knowledge to evaluate deals, monitor managers, or time distributions is how concentrated bets go wrong.

Family Office Services

A family office is a dedicated structure that coordinates investment management, tax, estate, philanthropy, and sometimes lifestyle management under one umbrella.

Two models exist:

| Type | Best For | Typical Threshold |

|---|---|---|

| Single-family office | One family, maximum customization | $250M–$500M+ in assets |

| Multi-family office | Multiple families sharing infrastructure | More cost-efficient entry point |

Deloitte estimates 8,030 single-family offices globally in 2024, up 31% since 2019 — with 3,180 in North America. That growth reflects a real problem: fragmented advisor relationships create gaps that a unified governance structure is designed to close.

The primary benefit isn't just investment returns. It's consistent decision-making across generations, with one unified strategy rather than a dozen separate professional relationships pulling in different directions.

Concentrated Position and Equity Compensation Planning

Executives, founders, and business owners often hold the bulk of their wealth in a single stock, business, or asset class. That concentration creates meaningful downside risk. Moving out of it without triggering a large immediate tax bill requires deliberate, sequenced strategy.

Options worth evaluating with an advisor:

- Exchange funds — Contribute concentrated shares into a fund, receive diversified exposure

- Collars — Options strategies that cap downside while limiting upside

- Charitable strategies — Donate appreciated shares to a donor-advised fund or trust

- Installment sales — Spread gain recognition over multiple years

For executives with RSUs and stock options, the planning layer deepens further. Vesting schedules, exercise timing, blackout periods, and AMT exposure all interact — and each decision has downstream tax consequences.

Median CEO stock awards reached $21.9 million in 2025, according to Equilar. At that scale, equity compensation planning isn't a side conversation — it's one of the highest-leverage financial decisions an executive makes.

Asset Protection and Risk Management for High-Net-Worth Individuals

Greater wealth creates greater exposure — to lawsuits, creditors, and liability. Core protection tools include:

- Domestic asset protection trusts — Shield assets from future creditors while retaining some benefit

- LLCs and S-corps — Create legal barriers between business and personal assets

- Umbrella insurance — Chubb notes personal umbrella limits range from $1M to $100M, layering above standard home and auto coverage

Beyond litigation risk, other protection needs deserve attention:

- Life and disability insurance — An unexpected event can derail decades of planning; coordinating with licensed specialists ensures appropriate coverage is in place

- Long-term care coverage — Extended care costs can erode assets quickly; a fiduciary advisor can help evaluate options alongside a qualified insurance professional

Physical and financial protections only go so far. Cybersecurity has become a serious concern for HNWIs. The FBI's IC3 2025 report documented cyber-enabled losses exceeding $20.877 billion, with investment fraud alone accounting for $8.649 billion. Advisors increasingly address digital security — account protection, privacy practices, and fraud prevention — as part of the HNWI risk management conversation.

How to Choose the Right Wealth Manager for Your Needs

The most important question to ask when evaluating a wealth manager isn't "what returns do you target?" It's "what do you actually cover?"

Comprehensive Planner vs. Asset Manager

An asset manager focuses on portfolio construction and performance. A comprehensive financial planner addresses the full picture: taxes, estate planning, insurance, cash flow, equity compensation, and investments — as one connected system.

Endeavor Financial Group is built on this model. Every financial discipline — taxes, investments, estate, risk — is addressed as part of a single connected strategy, not as separate conversations. Their team coordinates directly with clients' CPAs and estate attorneys, serving as the quarterback of the overall financial plan.

Credentials and Fiduciary Status

Look for:

- CFP® (Certified Financial Planner) — Comprehensive planning expertise

- CFA® (Chartered Financial Analyst) — Deep investment analysis capability

- Fiduciary status — The SEC defines fiduciary duty as both a duty of care and a duty of loyalty; legally, the advisor must act in your interest, not recommend products for commission

More than 72% of financial advisors now operate under fee-based models, per Cerulli — but fee-based and fee-only are not the same thing. Confirm the advisor's compensation structure directly.

What a Strong Planning Process Looks Like

A disciplined advisor guides clients through a structured process:

- Discovery — Understand goals, priorities, income sources, and planning gaps

- Analysis — Assess current financial picture across all dimensions

- Strategy development — Build an integrated plan addressing taxes, investments, estate, and risk

- Implementation — Execute with coordination across advisors and legal professionals

- Ongoing monitoring — Adapt as markets, tax law, and life circumstances evolve

Knowing what this process should look like makes it easier to evaluate whether a specific advisor can actually deliver it — which is where the right questions matter.

Questions Worth Asking

- Do you have experience working with clients at my wealth level?

- Are you familiar with my specific planning needs — business ownership, equity compensation, estate complexity?

- How do you coordinate with my CPA and estate attorney?

- What does your ongoing review process look like?

Frequently Asked Questions

What is HNWI in wealth management?

HNWI stands for high-net-worth individual — defined as someone with $1 million or more in liquid, investable assets, excluding the primary residence. In wealth management, this classification determines eligibility for certain services, investment vehicles, and specialized planning strategies.

What percentage of Americans have a net worth over $1,000,000?

Based on Federal Reserve Survey of Consumer Finances data analyzed by Forbes, approximately 16 million American families — or slightly more than 12% — had a net worth of $1M or more in 2022. This figure uses total net worth, not the investable-assets definition Capgemini uses for its 8.7M HNWI count.

Where do millionaires keep their money if banks only insure $250,000?

HNWIs typically spread deposits across multiple institutions to stay within FDIC limits, and keep the majority of their wealth in diversified investment accounts, brokerage accounts, real estate, and other asset classes that fall outside FDIC caps entirely.

What is the difference between HNWI and UHNWI?

HNWIs have $1M+ in investable assets; UHNWIs have $30M or more. The distinction matters because UHNWI wealth involves greater planning complexity, access to exclusive investment vehicles, and often warrants more sophisticated structures such as family offices.

What services do wealth managers provide to high-net-worth individuals?

Core services include:

- Investment management and portfolio oversight

- Tax planning and tax-efficient withdrawal strategies

- Estate and legacy planning coordination

- Risk management and insurance review

- Charitable giving strategy

For UHNWI clients, family office coordination is typically added to manage the complexity across all of these areas.

At what net worth should I get a financial advisor?

There's no fixed threshold, but most people benefit from professional guidance once they have $500,000 or more in investable assets. Financial decisions become considerably more complex at the $1M+ level, and uncoordinated planning often costs more than working with a qualified advisor.