Many entrepreneurs find themselves so focused on day-to-day survival that long-term financial planning gets pushed aside. A recent study found that 50% of small businesses have fewer than 15 cash buffer days, a razor-thin margin that leaves little room for strategic thinking.

This article provides a clear, actionable roadmap to change that. We'll walk you through a structured, step-by-step approach to financial planning that aligns your business's success with your personal wealth goals, giving you the clarity and confidence to build a lasting legacy.

Key Takeaways

- A financial plan acts as a strategic roadmap for business growth and long-term stability.

- Essential components include budgets, cash flow forecasts, and key financial statements.

- Integrate business finances with personal goals like retirement and a clear exit strategy.

- Avoid critical mistakes like mixing funds or forgoing professional advice for sustainable success.

Why Financial Planning is a Non-Negotiable for Business Owners

A financial plan isn't just about bookkeeping or filing taxes; it's the strategic blueprint for your company's future. It helps you allocate resources effectively, manage risk, and steer your business toward its long-term objectives. Without a plan, you’re navigating blind.

The stakes are high. Poor financial management is a primary reason businesses fail. An analysis of failed startups by CB Insights found that 70% cited running out of capital as a key factor. A formal financial plan moves you from a reactive state of crisis management to a proactive position of control.

Key benefits of a robust financial plan include:

- Gain clarity and direction. A plan translates your vision into measurable financial goals, giving your team a clear target to work toward.

- Increase credibility with lenders. A well-documented plan is essential for securing funding, and the SBA confirms that a solid business plan is crucial for convincing investors.

- Solve problems proactively. By forecasting financials, you can anticipate potential cash flow shortages or identify investment opportunities before they arise.

The Core Components of a Business Financial Plan

Before you can build your roadmap, you need to understand the foundational documents that tell your company’s financial story. These reports provide a snapshot of where you are now and a baseline for where you're headed.

The Big Three Financial Statements

- Profit & Loss (P&L) Statement: Also called an income statement, this report summarizes revenues, costs, and expenses over a set period to answer the fundamental question: "Is my business profitable?"

- Balance Sheet: This provides a snapshot of your company's financial health on a specific day. It lists assets (what you own) and liabilities (what you owe) to calculate your net worth—a key figure for securing loans or valuing the business.

- Cash Flow Statement: Often the most critical report for daily operations, this statement tracks cash moving in and out of your business. It reveals your ability to cover immediate expenses like payroll and rent, preventing unexpected shortfalls.

Forward-Looking Projections

While the "big three" look backward, projections help you plan forward. Sales forecasts and financial projections use historical data and market analysis to set realistic goals and make informed decisions about hiring, expansion, and managing inventory.

These documents aren't just for accountants. Together, they form the narrative of your business, providing the clarity needed to steer it toward long-term success.

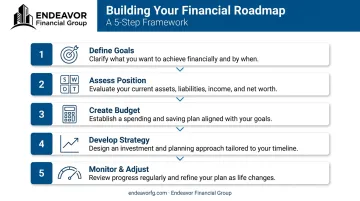

Building Your Financial Roadmap: A 5-Step Guide

Creating a financial plan feels less daunting when broken into a structured process. At Endeavor Financial Group, we guide business owners through a similar five-step journey to build a clear and comprehensive roadmap.

Define Your Business and Personal Financial Goals Your business should be a vehicle for achieving personal financial freedom. Start by setting SMART (Specific, Measurable, Achievable, Relevant, Time-bound) goals for both your company and your life.

Business goals might include 20% revenue growth, while personal goals could be retiring by 60 or funding a child's education. Aligning these two sets of goals is the critical first step.

Assess Your Current Financial Position Gather your foundational documents—the P&L, balance sheet, and cash flow statement. With this data in hand, conduct a simple SWOT analysis of your financial situation:

- Strengths: Healthy profit margins, low debt.

- Weaknesses: Inconsistent cash flow, high customer concentration.

- Opportunities: Untapped markets, potential for cost savings.

- Threats: Rising material costs, new competitors.

Create a Comprehensive Budget and Cash Flow Forecast Build an operational budget by separating fixed costs (rent, salaries) from variable costs (materials, marketing). This clarifies your break-even point and shows where you can optimize spending.

Next, create a 12-month cash flow forecast. This allows you to anticipate potential shortfalls and plan for seasonal surpluses.

Develop Your Strategic Plan for Growth and Risk This is where you plan your big moves. Your strategic plan should cover key areas like:

- Tax Planning: Work with a CPA to implement strategies that minimize your tax liability.

- Capital for Expansion: Determine how you'll fund growth—through profits, debt, or equity.

- Debt Management: Create a plan to pay down existing debt and evaluate any new financing.

- Risk Management: Identify financial risks (market downturns, loss of a key client) and build a contingency fund to weather them.

Monitor, Review, and Adjust Continuously Your financial plan isn't static. Set a schedule for regular reviews to keep it relevant and effective.

Check cash flow monthly, review your budget quarterly, and revisit your strategic plan annually. This discipline allows you to adapt to changing market conditions and stay on track with your goals.

Beyond the Business: Integrating Personal Wealth and Succession Planning

For many entrepreneurs, the business is the retirement plan. But failing to separate and integrate your business and personal wealth can put your entire future at risk. This final piece of the puzzle connects your business engine to your personal destination.

Planning for Your Retirement

Reinvesting every dollar back into the business is tempting, but it can leave you financially vulnerable. A 2024 Gallup poll found that one-third of business owners have no long-term plan for when they step away. It's crucial to pay yourself a consistent salary and fund dedicated retirement accounts. Options for business owners include:

- SEP IRA: Allows you to contribute up to 25% of your compensation, with a 2024 maximum of $69,000.

- Solo 401(k): For self-employed individuals (and a spouse), this plan allows you to contribute as both "employee" and "employer," with a total 2024 limit of $69,000.

- SIMPLE IRA: A straightforward option for businesses with fewer than 100 employees, allowing employee contributions and required employer matches.

Beyond funding retirement accounts, proper planning ensures the wealth you build is protected and passed on efficiently. Working with a financial advisor, like the team at Endeavor Financial Group, alongside legal professionals helps you create a tax-efficient estate plan that protects both your company and your personal assets. This forward-thinking approach is crucial for your eventual exit, whether you plan to sell, pass it to family, or transition to employees. A clear exit strategy, established years in advance, maximizes your business's value and ensures a smooth transition into your next chapter.

Common Mistakes and When to Seek Professional Guidance

Navigating financial planning alone can be treacherous. Here are three common pitfalls to avoid:

- Mixing business and personal finances: This common habit is a recipe for disaster. It creates an accounting nightmare, complicates tax filing, and can expose your personal assets to business liabilities. The IRS requires clear records, and a lack of substantiation can lead to disallowed deductions.

- Forgetting about "Future You": It's easy to prioritize the business's immediate needs over long-term savings for retirement. This mindset is why 6 in 10 small business owners find it difficult to fully retire, according to a study from Equitable and SCORE. Your personal financial security should be a non-negotiable business objective.

- Assuming a "DIY" approach is always best: While self-reliance is key for entrepreneurs, areas like tax law, investment management, and succession planning are highly specialized. A DIY approach here can lead to costly errors, missed opportunities, and an unbalanced portfolio.

Recognizing these challenges is the first step. The next is seeking professional guidance. A fee-only fiduciary firm like Endeavor Financial Group specializes in creating comprehensive financial plans tailored to the unique needs of business owners. We help you navigate these complexities, building a clear, integrated roadmap that connects your business success to your personal financial freedom.

Frequently Asked Questions

What are the 7 steps of financial planning for business owners?

The core process involves five steps: defining goals, assessing your position, creating a budget, developing a strategic plan, and continuous monitoring. To make it more comprehensive, you can add two more: securing adequate business insurance and establishing a formal succession plan.

What is the 50/30/20 rule for businesses?

While the 50/30/20 rule is designed for personal budgeting (50% needs, 30% wants, 20% savings), you can apply a similar principle to allocating after-tax business profits. For example: 50% for reinvestment/growth, 30% for owner distributions or debt reduction, and 20% for cash reserves.

Is $200,000 in assets enough to work with a financial advisor?

Absolutely. While some firms have high minimums, many advisors (including Endeavor Financial Group) focus on your goals, not just your assets. For business owners, flexible hourly or flat-fee options make expert advice accessible even when cash flow varies.

Can a financial advisor help with cryptocurrency?

While not all financial advisors are crypto specialists, a good advisor can help you understand the risks associated with volatile assets. They can help you determine if and how it fits into your overall diversified portfolio and ensure it doesn't compromise your long-term financial health.