For most retirees, the primary concern is making their savings last a lifetime without taking on unnecessary risk. This is where capital preservation becomes the guiding principle. Your portfolio's job shifts from aggressive growth to providing a reliable, sustainable income stream that protects your principal.

This article will guide you through the key strategies for making that safe descent. We’ll explore the unique risks retirees face, how to build a defensive financial foundation, and proven methods like the bucket system and bond laddering to create a resilient retirement portfolio.

TL;DR: Key Strategies for Capital Preservation

- Understand Retirement Risks: The biggest threats to your portfolio are poor market returns early in retirement (sequence risk), the rising cost of living (inflation risk), and the possibility of outliving your money (longevity risk).

- Build a Cash Buffer: Set aside 12 to 24 months of essential living expenses in a safe, liquid account to avoid selling investments during a market downturn.

- Use the Bucket Strategy: Segment your money by time horizon: a short-term bucket for immediate needs, a mid-term bucket for stable income, and a long-term bucket for growth.

- Ladder Your Bonds: Create a predictable income stream and reduce interest rate risk by staggering the maturity dates of your bonds or CDs.

The Unique Financial Risks of Retirement: Why Capital Preservation is Key

When you stop receiving a regular paycheck, your portfolio becomes your primary source of income. This transition exposes you to a new set of financial risks that didn't matter as much when you were focused on accumulation.

Sequence of Returns Risk

This is the risk of experiencing negative market returns in the first few years of retirement. When you’re withdrawing money to live on, a market downturn early on can do permanent damage. You’re forced to sell more shares at lower prices, which depletes your principal much faster.

Consider this example from Charles Schwab: two retirees start with $1 million and withdraw $50,000 a year, adjusted for inflation.

- Retiree A experiences a significant market drop in their first two years of retirement. Their portfolio runs out of money in just 18 years.

- Retiree B enjoys positive returns early on and experiences the exact same market drop ten years later. Their portfolio still has nearly $400,000 left after 18 years.

The only difference was the timing of the returns. This is why protecting your portfolio from early losses is so critical.

Inflation Risk

Inflation poses a more subtle threat, slowly eroding your purchasing power over time. Even a modest rate of inflation can have a huge impact over a 20 or 30-year retirement. Your savings must grow enough to not only fund your withdrawals but also keep pace with the rising cost of living.

Over the last 30 years, the average annual inflation rate in the U.S. has been around 2.5%. While that might not sound like much, it means that $50,000 in today’s money will only buy what $24,000 could 30 years ago. Your capital preservation strategy must account for this by including assets that can generate growth.

Longevity Risk

Thanks to advances in healthcare, people are living longer than ever. While that’s great news, it presents a financial challenge: the possibility of outliving your assets. According to the Social Security Administration, a 65-year-old woman today has an average life expectancy of another 20 years. A 65-year-old man can expect to live another 17.5 years. Many will live well into their 90s.

Your portfolio must be structured to provide reliable income for a retirement that could last for decades, making a disciplined capital preservation strategy non-negotiable.

Building Your Defensive Foundation: Cash Reserves and Liquidity

The first step in protecting your retirement savings is to build a wall between your living expenses and market volatility. This wall is your cash reserve—a liquidity buffer designed to cover your essential needs without forcing you to sell other investments at the wrong time.

Financial planners generally recommend setting aside 12 to 24 months of essential living expenses in highly liquid, safe accounts. This isn't money you're trying to grow; it's an emergency fund for your retirement.

The purpose of this buffer is simple but powerful. If the stock market enters a bear market, you can draw from your cash reserve to pay your bills instead of selling your stocks at a loss. This gives your growth-oriented assets time to recover, effectively neutralizing the threat of sequence of returns risk.

When building your cash reserve, choose accounts that prioritize safety and accessibility:

- Choose high-yield savings accounts for FDIC-insured funds that earn slightly more interest than traditional savings.

- Hold assets in money market funds, which invest in high-quality, short-term debt for safety and easy access.

- Stagger short-term Certificates of Deposit (CDs) to get a fixed, FDIC-insured rate while ensuring cash is available regularly.

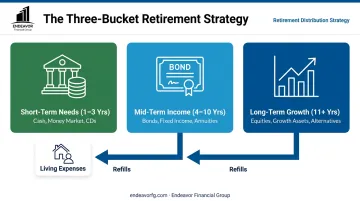

Core Strategy #1: The Bucket Strategy for Segmenting Your Nest Egg

The bucket strategy is a popular framework for organizing your retirement assets. It’s a form of mental accounting that helps you align your investments with your time horizon, ensuring you have the right money available at the right time. You simply divide your nest egg into three distinct "buckets."

Bucket 1: Short-Term Needs (1-3 Years)

This is your primary liquidity pool, designed to cover immediate living expenses for the next one to three years. It's essentially your cash reserve.

- Pays for daily living expenses and planned near-term purchases, providing peace of mind regardless of market volatility.

- Holds the safest, most liquid assets, such as cash, high-yield savings accounts, money market funds, and very short-term bonds or CDs.

- Provides your monthly income and is refilled periodically by returns generated from Bucket 2.

Bucket 2: Mid-Term Income (4-10 Years)

This bucket acts as a bridge, generating stable income and preserving capital with minimal risk. Its primary job is to systematically replenish Bucket 1 over the coming years.

- Generates a steady stream of income and returns without the volatility of the stock market.

- Contains high-quality, income-producing assets like bond ladders, conservative income funds, and low-volatility dividend stocks.

- Refills Bucket 1 as assets mature or generate interest, preventing you from selling long-term investments to cover short-term spending.

Bucket 3: Long-Term Growth (11+ Years)

This is your portfolio's growth engine. Because you won't need this money for at least a decade, it can be invested in assets with higher growth potential and can weather the inevitable ups and downs of the market.

- Grows your capital at a rate that outpaces inflation, ensuring your portfolio lasts throughout your retirement.

- Holds a diversified portfolio of domestic and international stocks, often through low-cost ETFs or mutual funds.

- Replenishes Bucket 2 over time by trimming profits after strong market performance and moving gains into more conservative assets.

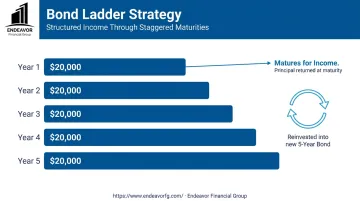

Core Strategy #2: Laddering Fixed-Income for Predictable Cash Flow

For retirees who want a predictable, reliable stream of cash flow, a bond or CD ladder is one of the most effective strategies available. Laddering is the practice of buying multiple fixed-income securities with staggered maturity dates.

Instead of investing a lump sum into a single 10-year bond, you would divide that money across bonds that mature in different years. For example, with $100,000, you could build a 5-year ladder by investing:

- $20,000 in a 1-year bond

- $20,000 in a 2-year bond

- $20,000 in a 3-year bond

- $20,000 in a 4-year bond

- $20,000 in a 5-year bond

When the 1-year bond matures, you can use the principal for income or reinvest it into a new 5-year bond at the "long end" of the ladder, maintaining the structure for years to come.

Benefits of a Laddering Strategy

This simple approach offers several powerful advantages for capital preservation.

First, it creates a predictable and steady stream of income. You know exactly when each bond or CD will mature, giving you a reliable source of cash to fund your living expenses or refill Bucket 1 of your portfolio.

Second, laddering helps mitigate interest rate risk. One of the main risks for bond investors is a rise in interest rates, which causes the value of existing, lower-rate bonds to fall.

Because a ladder has bonds maturing every year, you can adapt to the changing rate environment. If rates go up, you can reinvest the principal into new, higher-yielding bonds. If rates have fallen, you still benefit from your older, locked-in bonds.

You can build a ladder with some of the safest investments available, including:

- Certificates of Deposit (CDs): FDIC-insured and offered by most banks.

- U.S. Treasury Securities: Backed by the full faith and credit of the U.S. government, these are considered among the safest investments in the world.

- High-Quality Municipal or Corporate Bonds: For those willing to take on slightly more risk for a higher yield.

Putting It All Together: A Cohesive Plan for the Long Haul

Implementing strategies like the bucket system and bond laddering requires more than just buying the right investments. A successful capital preservation plan must also be tax-efficient and disciplined.

One key concept is tax-efficient asset location. This means placing investments that generate high taxable income, like corporate bonds, inside tax-advantaged accounts such as an IRA or 401(k).

Meanwhile, more tax-efficient investments like long-term stocks or municipal bonds can be held in a standard taxable brokerage account. This strategy can significantly reduce your tax bill over your retirement.

Equally important is disciplined rebalancing. Over time, your asset allocation will drift as some investments outperform others. It's crucial to review your portfolio at least annually and rebalance back to your target mix. This prevents you from becoming over-exposed to risk and forces you to "sell high and buy low."

While these strategies provide a powerful framework, implementing them effectively requires careful personalization. At Endeavor Financial Group, our five-step process is designed to tailor these strategies to your unique goals, income needs, and risk tolerance.

As fee-only fiduciaries, our CFP® designated advisors are legally bound to act in your best interest. This ensures the advice you receive is always unbiased and focused on helping you achieve a secure retirement.

Frequently Asked Questions

What is the difference between capital preservation and capital appreciation?

Capital preservation focuses on protecting your principal from loss, while capital appreciation focuses on growing its value. Retirees need a strategic balance of both—preservation for near-term income and appreciation to ensure their money outlasts inflation over the long term.

How much cash should I keep on hand in retirement?

A common guideline is to hold 12 to 24 months of your essential living expenses in a liquid, safe account. This cash buffer protects you from having to sell growth investments during a market downturn to cover your bills.

Are bonds completely safe for capital preservation?

While generally safer than stocks, bonds are not risk-free. They carry interest rate risk (their market value can fall when rates rise) and credit risk (the issuer could default on their payments). Building a high-quality bond ladder helps mitigate these risks.

Can I still own stocks if my goal is capital preservation?

Yes, and you absolutely should. Stocks are crucial for providing the long-term growth needed to combat inflation over a multi-decade retirement. They should be part of a balanced portfolio, typically held in your long-term bucket (Bucket 3).

What is sequence of returns risk and why is it so important for retirees?

It's the risk of experiencing poor market returns early in retirement. Since you are also withdrawing funds, these early losses can severely reduce your portfolio's longevity and make recovery much more difficult.

How often should I rebalance my retirement portfolio?

You should review your portfolio at least once a year. A common approach is to rebalance whenever your asset allocation drifts significantly from your target—for example, by more than 5% in either direction.