This guide provides a clear, step-by-step framework for the fundamentals of stock portfolio management. We'll break down what it is, the core principles that drive success, and how to decide between a DIY approach and professional guidance. You'll walk away with a practical roadmap to take control of your investments.

TL;DR: The Essentials of Portfolio Management

- What it is: The ongoing process of creating and maintaining a collection of investments to meet your specific financial goals.

- Core principles: It revolves around aligning with your goals, strategic asset allocation, and disciplined monitoring.

- The process: Involves defining your goals, creating an asset allocation plan, selecting investments, and regularly reviewing your portfolio.

- Why it matters: Effective management helps minimize risk and maximize returns, ensuring your investments stay on track to fund retirement, business growth, or other major life events.

What Is Stock Portfolio Management? (And Why It Matters)

Stock portfolio management is the art and science of selecting, overseeing, and adjusting a mix of investments to achieve your long-term financial objectives. It goes beyond picking individual stocks to create a strategic framework that guides all of your investment decisions.

Buying stocks without a plan is like having a pile of bricks without a blueprint. Portfolio management provides the architectural plan to assemble those bricks into a sturdy financial structure designed to weather market storms.

The primary goals of portfolio management are:

- Mitigate risk by diversifying across different asset classes to smooth out volatility and protect against significant losses.

- Optimize returns by balancing growth and stability to achieve the best possible performance for your risk tolerance.

- Align with your goals by ensuring every investment decision supports a specific outcome, like funding retirement or preserving wealth.

This discipline is critical for pre-retirees shifting from aggressive growth to capital preservation. It’s also essential for business owners looking to strategically diversify wealth outside of the company they’ve worked so hard to build.

Having a documented plan is a powerful first step. According to Charles Schwab's 2024 Modern Wealth Survey, 96% of people with a written financial plan feel confident they will reach their goals.

The 3 Core Principles of Effective Portfolio Management

Any successful investment strategy rests on a few foundational pillars. These principles provide the discipline needed to navigate markets over the long term.

1. Goal-Driven Investing

Every decision you make must be tied back to a specific, measurable financial goal. "I want to make money" is a wish, not a goal. "I need my portfolio to generate $5,000 per month in retirement starting at age 65" is a goal. This clarity dictates your entire strategy, from how much risk you can take to the types of investments you choose.

2. Strategic Asset Allocation

Asset allocation is the practice of dividing your portfolio among different asset categories, such as stocks, bonds, and cash. It is the most significant driver of your portfolio's performance—even more so than picking individual stocks.

Vanguard's research confirms this, showing that a portfolio's broad mix of stocks and bonds explains the vast majority of its return variability. Your allocation is your primary tool for controlling risk and targeting returns.

3. Discipline and a Long-Term Perspective

Markets are noisy. Emotional decisions based on short-term headlines are one of the biggest destroyers of wealth. A solid portfolio management plan provides the discipline to stick with your strategy during inevitable market highs and lows, preventing you from buying high out of greed or selling low out of fear.

A Step-by-Step Guide to Managing Your Stock Portfolio

Here is a practical, four-step roadmap to building and maintaining your investment portfolio.

Step 1: Define Your Financial Goals and Risk Tolerance

This is the discovery phase. Before you invest a single dollar, you need to understand what the money is for and how much volatility you can stomach.

Ask yourself crucial questions:

- What are my specific financial goals? (for example, retire at 65 with an $80,000 annual income, fund a child's education in 10 years, invest the proceeds from selling my business for long-term security).

- What is my time horizon? A 35-year-old investing for retirement can take on more risk than a 62-year-old who needs to start drawing income soon.

- What is my risk tolerance? This is both your financial ability and emotional willingness to withstand market downturns. Many financial advisors use risk tolerance questionnaires to help quantify this.

The outcome of this step should be a clear "Investor Policy Statement"—even an informal one—that documents your goals, time horizon, and risk level.

Step 2: Create a Strategic Asset Allocation Plan

With your goals defined, you can now create the blueprint for your portfolio. This involves deciding what percentage of your assets will go into the primary asset classes:

- Equities (Stocks): Offer the highest potential for long-term growth but come with the most volatility.

- Fixed Income (Bonds): Generally provide lower returns than stocks but offer more stability and income.

- Cash/Cash Equivalents: Offer safety and liquidity but little to no growth, often losing purchasing power to inflation over time.

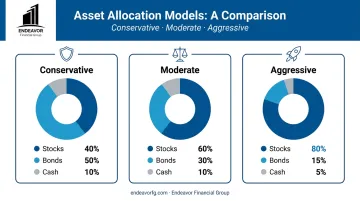

Your allocation should directly reflect your risk tolerance. Here are a few common examples:

- Conservative: 40% stocks, 50% bonds, 10% cash (Suits those nearing retirement with a focus on capital preservation).

- Moderate: 60% stocks, 30% bonds, 10% cash (A balanced approach for investors with a medium time horizon).

- Aggressive: 80% stocks, 15% bonds, 5% cash (Appropriate for investors with a long time horizon who can withstand market swings).

Remember to also diversify within each asset class. For stocks, this means holding a mix of large-company, small-company, domestic, and international stocks.

Step 3: Select Your Investments

Only after your allocation plan is set should you choose specific investments. This prevents you from chasing "hot tips" or making impulsive decisions.

There are two primary approaches to implementing your plan:

- Passive Investing: This involves using low-cost index funds or Exchange-Traded Funds (ETFs) to match the performance of a market index, like the S&P 500. It's a simple, low-cost, and effective strategy for most investors.

- Active Investing: This involves picking individual stocks or actively managed mutual funds with the goal of outperforming the market. This approach requires significant research and skill, and it often comes with higher costs.

The active vs. passive debate is ongoing, but data shows how difficult it is to consistently beat the market. According to the SPIVA U.S. Scorecard from S&P Dow Jones Indices, more than 90% of all domestic equity funds failed to outperform their benchmarks over the past 15 years.

Step 4: Monitor and Rebalance Your Portfolio

Portfolio management is an ongoing process, not a one-time setup. You need to review your portfolio periodically and make adjustments to keep it aligned with your goals.

- Monitoring: Check on your portfolio's performance at least semi-annually. Ensure it's on track to meet your goals and that the reasons you hold each investment are still valid.

- Rebalancing: This is the act of selling assets that have performed well and buying those that have underperformed to return your portfolio to its original target allocation. For example, if a strong year in stocks pushes your 60/40 portfolio to 70/30, you would sell some stocks and buy bonds to get back to your 60/40 target. This enforces a "buy low, sell high" discipline.

This structured, four-step process provides a solid foundation for managing your investments. While these principles are straightforward, applying them consistently requires discipline and expertise. A financial advisor can help you navigate these steps, ensuring your portfolio remains aligned with your long-term goals.

DIY vs. Professional Portfolio Management: When to Partner with an Advisor

It is certainly possible to manage your own portfolio, especially with the wide availability of online brokerages and low-cost funds. However, a successful DIY approach requires significant time, knowledge, and—most importantly—emotional discipline.

The biggest challenge for individual investors is often their own behavior. We tend to make emotional decisions when markets get volatile, which can lead to poor outcomes.

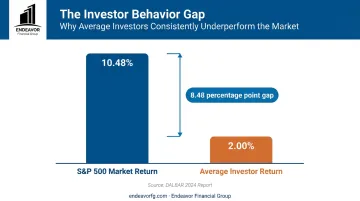

The research firm DALBAR quantifies this "behavior gap" every year. Its 2024 report found the average equity investor earned a return that was 8.48 percentage points lower than the S&P 500's return, largely due to poorly timed buying and selling.

Partnering with a financial advisor provides expertise and discipline, and it can be particularly valuable for:

- Busy professionals who lack the time for in-depth market research.

- Business owners who need to manage complex personal and company finances.

- Those nearing retirement who require a holistic strategy connecting their portfolio to taxes, estate plans, and income goals.

At Endeavor Financial Group, our comprehensive process begins with discovering your unique goals, moves to detailed strategic planning, and includes implementation and ongoing support.

As a fee-only fiduciary, we are legally bound to act in your best interest. This ensures you receive the unbiased guidance needed for a clear roadmap to your financial goals.

Frequently Asked Questions

What is Warren Buffett's 90/10 rule?

This refers to the instructions Warren Buffett gave for his wife's estate. In his 2013 Berkshire Hathaway shareholder letter, he recommended putting 90% in a very low-cost S&P 500 index fund and 10% in short-term government bonds.

What is the 70/20/10 rule in investing?

This is a budgeting guideline, not an investment strategy. It suggests allocating 70% of income to expenses, 20% to savings or investments, and 10% to debt repayment, so it doesn't apply to portfolio construction.

What is the first step in portfolio management?

The first and most critical step is defining your personal financial goals, time horizon, and risk tolerance. All other decisions, from asset allocation to investment selection, flow from this essential foundation.

How often should I rebalance my portfolio?

There's no single right answer, but common strategies include rebalancing annually on a set date or whenever an asset class drifts by a predetermined amount (e.g., 5% or 10%) from its target allocation.

What is the difference between asset allocation and diversification?

Asset allocation diversifies across asset classes (stocks, bonds, cash). Diversification is a broader concept that also includes spreading investments within an asset class, such as owning stocks from various industries.

Can I manage my own stock portfolio?

Yes, if you have the required knowledge, time, and discipline. However, many investors work with a fiduciary advisor to gain professional expertise, avoid behavioral mistakes, and create a comprehensive financial plan.