This shift from accumulation to "decumulation" can feel daunting. How do you make your money last? How do you protect it from market swings and inflation? This guide is here to answer those questions. We'll walk through the essential components of a durable retirement income strategy, explore the most common approaches, and help you understand the factors to consider when building a plan that provides true financial confidence.

TL;DR: Key Retirement Income Takeaways

- A formal income strategy is crucial due to modern challenges like longer lifespans, inflation, and market volatility.

- Most retirement income is built on three pillars: Social Security, employer plans like 401(k)s, and personal savings.

- Popular strategies include systematic withdrawals (like the 4% rule), guaranteed income from annuities, and bond ladders.

- The "bucket strategy" is a popular hybrid approach that segments your assets by time horizon to manage risk.

- The best strategy is a personalized blend tailored to your risk tolerance, expenses, health, and legacy goals.

Why You Need a Solid Retirement Income Strategy

Gone are the days of retiring at 65 with a company pension that covers all your needs. Today’s retirement landscape presents a unique set of challenges that make a formal income plan more critical than ever.

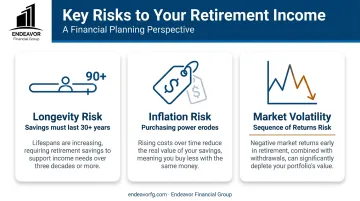

Longevity Risk

People are living longer. According to the CDC, the average life expectancy for a 65-year-old in the U.S. is now nearly 20 additional years. For a healthy 65-year-old couple, there's a 45% chance at least one spouse will live to age 90.

This incredible gift of a longer life also means your retirement savings may need to last for 30 years or more. Without a plan, there's a real risk of outliving your money.

Inflation

The rising cost of living is a silent portfolio killer. Even modest inflation can significantly erode your purchasing power over a long retirement.

For example, an income of $50,000 per year today would need to become about $90,300 per year in 20 years just to buy the same amount of goods and services, assuming an average inflation rate of 3%. Your income strategy must include a plan for growth to ensure your lifestyle doesn't shrink over time.

Market Volatility

Retiring into a bear market can have a devastating impact on your portfolio's longevity. This is known as sequence of returns risk. Withdrawing money from a portfolio during a downturn locks in losses and permanently reduces the asset base you need for future growth. A well-designed strategy creates buffers so you aren’t forced to sell investments at the worst possible time.

Understanding the Core Components of Your Retirement Income

Understanding the primary sources that will fund your retirement is the first step in building a sustainable strategy. Most plans are built on three foundational pillars.

Social Security

Think of Social Security as your baseline income floor. For the average worker, Social Security is designed to replace about 40% of pre-retirement earnings, though this percentage is higher for lower-income earners and lower for high earners. When you claim your benefits is a critical decision, as delaying can significantly increase your monthly payments for life.

Pensions and Employer-Sponsored Plans

While traditional pensions—which provide a guaranteed monthly check for life— are less common now, they still provide a valuable guaranteed income stream for many. For most people, however, the bulk of their savings is in defined contribution plans. These include:

- 401(k)s and 403(b)s

- Traditional and Roth IRAs

- SEP IRAs for the self-employed

These accounts have grown tax-deferred or tax-free for years, and now is the time to create a tax-efficient plan for withdrawing from them.

Personal Savings and Investments

This category includes any other assets you've accumulated that can be used to generate income. This might be a taxable brokerage account, rental income from real estate, CDs, or cash savings. These assets often provide the most flexibility in a retirement income plan.

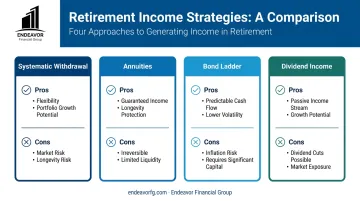

Four Popular Retirement Income Strategies

There is no one-size-fits-all solution for generating retirement income. Here are four of the most common strategies, each with its own set of advantages and disadvantages.

1. The Systematic Withdrawal Approach (Total Return)

This is perhaps the most well-known strategy, centered on the idea of the "4% Rule." You withdraw a set percentage of your portfolio each year, adjusting the dollar amount annually for inflation. The portfolio is managed for total return, which means it focuses on the overall growth of your assets, not just the income they generate.

- Pros: It’s simple to understand, offers complete flexibility to adjust spending, and you maintain full control over your assets. If markets perform well, your portfolio can continue to grow.

- Cons: It offers no income guarantee and fully exposes you to market risk, especially the sequence of returns risk. Modern research from firms like Morningstar suggests a lower starting rate of 3.9% may be more sustainable today.

2. Guaranteed Income with Annuities

An income annuity is a contract with an insurance company. You give them a lump sum of money, and in return, they provide you with a guaranteed stream of payments for a set period or for the rest of your life. This essentially allows you to create your own personal pension.

- Pros: An annuity provides a predictable, reliable income you can't outlive, which is perfect for covering essential expenses like housing and healthcare. This can provide immense peace of mind.

- Cons: Contracts are often irreversible, meaning you lose access to your principal once it's signed. Payments can have limited inflation protection without costly riders, and annuities may include high fees or hidden commissions.

3. The Bond Ladder Strategy

A bond ladder is built by purchasing several individual bonds that mature on different dates. For example, you might buy bonds that mature in one, two, three, four, and five years. When the one-year bond matures, you use the money for income and buy a new five-year bond to keep the ladder going.

- Pros: This strategy provides a highly predictable stream of income. It helps manage interest rate risk because you are regularly reinvesting at current rates. And, assuming the issuer doesn't default, your principal is returned at maturity.

- Cons: Building and managing a bond ladder can be complex. The income may not keep pace with high inflation, and you are exposed to the credit risk of the bond issuers.

4. The Dividend and Interest Income Strategy

With this approach, you aim to live only on the natural yield—dividends from stocks and interest from bonds—generated by your portfolio. The goal is to never touch the original principal, preserving it for legacy goals or future needs.

- Pros: This strategy is excellent for preserving your principal. If you invest in companies that consistently increase their dividends, your income can grow over time, providing a natural hedge against inflation.

- Cons: It requires a very large portfolio to generate sufficient income. For example, to generate $50,000 in annual income from a portfolio with a 4% average yield, you would need $1.25 million saved. Dividends are not guaranteed and can be cut. Additionally, focusing only on high-yield stocks can lead to a poorly diversified and riskier portfolio.

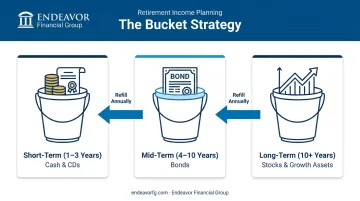

The Bucket Strategy: A Deeper Look

The bucket strategy is a popular way to structure retirement income because it's both practical and psychologically comforting. It helps manage the stress of a fluctuating portfolio by dividing your assets into distinct "buckets" based on when you'll need the money.

Bucket 1: Short-Term Needs (1-3 years)

This bucket is for your immediate living expenses. It holds your most conservative assets, protecting your near-term income from market volatility.

- What's inside: Cash, money market funds, short-term CDs.

- Purpose: To cover 1 to 3 years of expenses, ensuring you never have to sell stocks in a down market to pay your bills.

Bucket 2: Mid-Term Needs (4-10 years)

This bucket’s primary job is to refill Bucket 1. It’s invested more for a balance of income and modest growth, taking on moderate risk.

- What's inside: High-quality bonds, conservative balanced funds, and some blue-chip, dividend-paying stocks.

- Purpose: To generate returns that are stable enough to systematically replenish your cash bucket without the full volatility of the stock market.

Bucket 3: Long-Term Growth (10+ years)

This is your portfolio's growth engine. Because this money won't be needed for at least a decade, it can be invested more aggressively to generate the long-term returns needed to outpace inflation.

- What's inside: A diversified mix of domestic and international stocks, equity mutual funds, and ETFs.

- Purpose: To ensure your overall portfolio grows over your 20- or 30-year retirement, allowing you to sustain your income for the long haul.

The system works by spending from Bucket 1. Periodically, such as once a year, you sell appreciated assets from Buckets 2 and 3 to refill it. This disciplined process keeps your short-term cash reserves full, allowing your long-term growth investments to remain untouched during market downturns.

How to Choose the Right Strategy for Your Goals

The "best" strategy is rarely one of the above in isolation. It's usually a personalized blend that aligns with your unique financial situation and life goals. To find the right mix, start by assessing these key factors.

- Evaluate your risk tolerance. Your comfort with market fluctuations will influence how much you allocate to stocks versus more stable, guaranteed income sources.

- Separate essential and discretionary expenses. Match non-negotiable costs (mortgage, food, utilities) with guaranteed income like Social Security. Your portfolio can then cover discretionary spending like travel and hobbies.

- Consider your health and longevity. If you expect a long life, securing guaranteed lifetime income may be a priority. If you have health concerns, you might focus on preserving assets for potential medical costs.

- Define your legacy goals. If leaving an inheritance is important, you will likely favor strategies that preserve your principal rather than those designed to spend down assets over your lifetime.

Building Your Comprehensive Retirement Income Plan

A retirement income plan isn't a "set it and forget it" document. It must adapt to your life and evolving market conditions. Coordinating Social Security, managing tax-efficient withdrawals, and navigating market shifts requires a clear strategy—and often, professional guidance.

At Endeavor Financial Group, we use a comprehensive five-step process designed to build a durable retirement income plan tailored to your specific situation.

- Introductory Meeting: We start by getting to know you—your goals, priorities, and concerns. This discovery phase is about understanding your vision for the future before we even look at the numbers.

- Exploration & Preliminary Planning: We take a deeper dive into your financial life, having detailed conversations to sketch out a preliminary plan that aligns with your objectives.

- Detailed Planning: We deliver a clear, easy-to-follow roadmap. This detailed plan addresses your most important goals and outlines the steps needed to build a solid, tax-efficient portfolio.

- Implementation: We guide you through each step, providing foresight and support to ensure your plan is put into action correctly.

- Ongoing Support & Advice: Your life evolves, and your plan should too. We conduct regular reviews to make proactive adjustments, ensuring your strategy remains aligned with your evolving goals.

Ready to move from uncertainty to clarity? Schedule a complimentary discovery consultation with the Endeavor Financial Group team today and start building the retirement you've worked so hard for.

Frequently Asked Questions

What is the best retirement income strategy?

There is no single "best" strategy. The optimal approach is a personalized plan that blends different methods based on your unique risk tolerance, financial goals, health outlook, and legacy wishes.

What is the 30 30 30 10 rule for retirement?

This is a general budgeting rule for the savings phase (e.g., 30% for housing, 30% for needs, etc.), not a retirement income withdrawal strategy. It helps with accumulation but doesn't provide guidance on how to spend down assets in retirement.

How much can I safely withdraw from my retirement savings each year?

The "4% Rule" is a traditional guideline, but today's safe withdrawal rates are dynamic. Many experts now suggest a more conservative 3.5%-4% starting point, adjusted for your age, asset allocation, and market conditions.

How do I protect my retirement income from inflation?

A multi-faceted approach is best. Protect your purchasing power by holding growth assets like stocks, considering Treasury Inflation-Protected Securities (TIPS), and adding cost-of-living-adjustment (COLA) riders to annuities.

When is the best time to claim Social Security?

While you can claim as early as 62, delaying until your full retirement age or age 70 significantly increases your monthly benefit. The best time depends on your health, other income sources, and marital status.

Should I still own stocks when I'm retired?

Yes, most retirees should maintain an allocation to stocks. Over a multi-decade retirement, their long-term growth potential is essential to help your portfolio outpace inflation and maintain purchasing power.