Many owners find themselves trapped by volatile cash flow, struggling to connect their business's profitability to their personal financial security. The dream of one day selling the company or passing it on to the next generation feels distant when you're just trying to make payroll next month.

This guide is your blueprint for changing that. We’ll walk through everything from mastering daily financial operations to building a long-term legacy, giving you a clear path to financial stability and success.

TL;DR: Your Financial Blueprint

- Master Cash Flow: Construction's long payment cycles are a major risk. Implement strict billing, require deposits, and build a 3-6 month cash reserve.

- Know Your True Costs: Accurate job costing is non-negotiable. Use historical data to create smarter, more profitable bids.

- Plan for Big Purchases: Create a Capital Expenditure (CapEx) plan for heavy equipment and use tax strategies like Section 179 to your advantage.

- Integrate Business & Personal: Your business should fund your personal goals. Connect the two with a unified financial plan that includes retirement and a succession strategy.

- Don't Go It Alone: Partner with a financial professional who understands the unique challenges business owners face.

Why Financial Planning is Different (and Critical) for Construction Owners

Financial planning in construction isn't like in other industries. While a retail store has predictable daily sales, you operate in a world of project-based revenue, long payment cycles, and high capital costs. This creates a unique and challenging financial landscape.

The core challenges include:

- Irregular, project-based revenue that makes consistent cash flow a constant battle.

- Long payment cycles that average 83 days, often compounded by retainage where 5-10% of payment is withheld.

- High capital costs for heavy equipment, skilled labor, and materials with volatile prices that can destroy a job's profitability.

- Sensitivity to economic cycles, which ties your pipeline of new projects directly to the health of the economy.

Without a financial plan designed for these unique challenges, construction businesses often remain in a reactive state instead of achieving proactive growth. This is a key reason why, according to the Bureau of Labor Statistics, only 42.6% of construction firms make it to their tenth year. A solid financial plan is your best tool for beating those odds.

The Foundation: Mastering Your Business's Day-to-Day Financials

Before you can build a legacy, you need a rock-solid foundation. That starts with disciplined, day-to-day financial management. These three habits are the bedrock of a healthy construction business.

Separate Business and Personal Finances—The First Rule

This may sound basic, but it's the most common mistake owners make. Commingling funds creates a bookkeeping nightmare and makes tax preparation difficult. Most importantly, it puts your personal assets—like your home, savings, and vehicles—at risk if the business faces legal trouble or debt.

Action Step: Immediately open separate checking accounts, savings accounts, and credit cards for your business. All business income goes into the business account, and all business expenses are paid from it. Pay yourself a regular, predictable salary from the business account to your personal account.

Develop a Rock-Solid Budget and Job Costing System

A business budget is your high-level financial map for the year, accounting for both fixed and variable costs.

- Fixed costs are predictable expenses like rent, insurance, key employee salaries, and software subscriptions.

- Variable costs fluctuate with your workload and include materials, fuel, subcontractor payments, and hourly labor.

While a budget provides the big picture, accurate job costing is what determines your profitability. It’s the only way to know which projects actually make you money. For every single job, you must meticulously track:

- Labor hours and costs

- Material quantities and expenses

- Equipment usage and rental fees

- Subcontractor invoices

- Permit fees and other direct costs

This data is your single source of truth. It tells you where you're making money and where you're losing it, allowing you to build more accurate bids for future work.

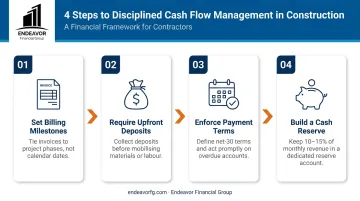

Implement a Disciplined Cash Flow Management Process

Profit on paper doesn't pay the bills. Cash flow is the lifeblood of your business, and you need to manage it with discipline. Negative cash flow is one of the top reasons construction companies fail.

Here are actionable steps to take control:

- Set Clear Billing Milestones: Structure contracts so you can invoice as you complete key phases of a project, not just at the very end.

- Require Upfront Deposits: Always get a deposit before you order materials or schedule labor. This protects you if a client backs out and improves your initial cash position.

- Enforce Payment Terms: Clearly state your payment deadlines (e.g., Net 30) on every invoice and follow up immediately when an invoice becomes overdue.

- Build a Cash Reserve: Aim to have 3-6 months of core operating expenses saved in a separate business savings account. This is your emergency fund for slow periods, unexpected project delays, or major equipment repairs.

Advanced Strategies for Profitability and Growth

Once your foundational finances are in order, you can shift your focus to strategic growth. This involves using your financial data to make smarter decisions about bidding, equipment, and expansion.

Using Financial Data to Make Smarter Bids

Your job costing data is a goldmine. Stop guessing and start using historical numbers to build future bids. When you know exactly what a similar project cost you in the past—including your true labor burden and overhead allocation—you can create bids that are both competitive and profitable. This data-driven approach removes emotion and ensures every new job contributes positively to your bottom line.

Creating a Capital Expenditure (CapEx) Plan

Buying a new excavator or dump truck is a major financial decision that shouldn't be made on a whim. A CapEx plan is a forward-looking strategy for acquiring, upgrading, and replacing major assets.

When considering a large purchase, you need to analyze the "lease vs. buy" decision.

- Buying: You build equity in the asset and can take advantage of tax deductions for depreciation. However, it requires a large upfront cash outlay or loan.

- Leasing: This requires less cash upfront and may include maintenance, but you don't own the asset at the end of the term.

A crucial part of this plan is understanding tax implications. For instance, Section 179 of the IRS tax code allows businesses to deduct the full purchase price of qualifying equipment in the year it's placed in service. This can provide a significant tax benefit compared to depreciating the asset over many years.

Deduction limits change annually, so you should always consult with your tax professional to ensure it's the right move for your situation. A financial advisor can help coordinate these big-picture decisions, ensuring they align with your long-term growth plans.

Securing the Right Financing for Expansion

Growth often requires capital. Whether you're hiring more crew, expanding your service area, or bidding on larger projects, you'll need access to financing. Maintaining clean, accurate, and up-to-date financial records is critical for demonstrating your creditworthiness to lenders.

Key financing options include:

- Revolving Line of Credit: Perfect for managing short-term working capital needs and bridging cash flow gaps between project payments.

- Equipment Loans: Term loans used specifically to purchase new or used heavy equipment.

- SBA Loans: Government-backed loans, like the SBA's CAPLines program for builders, can offer favorable terms for working capital or expansion.

- Surety Bonds: While not direct financing, a strong financial history is essential for increasing your bonding capacity, which is required to bid on larger, more lucrative contracts.

Protecting Your Business: Risk and Tax Management

A profitable business can be quickly derailed by a single unforeseen event. Proactive risk and tax management are essential for protecting what you've built.

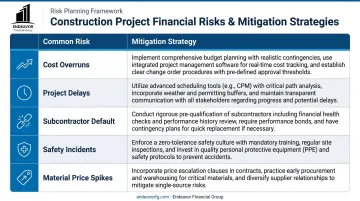

Identifying and Mitigating Financial Risks

Construction is an inherently risky business. Your financial plan must account for potential threats and include strategies to mitigate them.

| Common Risk | Mitigation Strategy |

|---|---|

| Cost Overruns | Build a 10-15% contingency fund into every project budget. |

| Project Delays | Use strong contracts with clear timelines and penalties. |

| Subcontractor Default | Thoroughly vet subcontractors and consider subcontractor default insurance (SDI) for large jobs. |

| Safety Incidents | Maintain robust safety protocols and carry adequate workers' compensation insurance. |

| Material Price Spikes | Include price escalation clauses in your contracts for long-term projects. |

Beyond project risks, ensure your business is properly insured with general liability, builder's risk, and commercial auto policies.

Proactive Tax Planning Strategies

Tax planning is a year-round activity, not just something you think about in April. Partnering with a financial advisor who coordinates with your CPA is key. A team that understands the construction industry can align these tax strategies with your broader financial goals, potentially saving you thousands.

Key strategies to discuss with your financial team include:

- Optimizing your business structure (e.g., LLC, S-Corp) for tax efficiency based on your profitability.

- Selecting the correct revenue recognition method, like Percentage of Completion vs. Completed Contract, to manage income reporting.

- Maximizing equipment depreciation to significantly reduce your annual taxable income.

Building Your Legacy: Personal Wealth & Succession Planning

Your construction business is a vehicle for achieving personal financial goals. To make that happen, you need a clear plan to translate your business success into personal wealth and a lasting legacy.

Connecting Business Profit to Your Personal Financial Goals

Start by defining what you want to achieve personally. Do you want to retire at 60? Pay for your kids' college education? Buy a vacation home? Once you have clear, specific goals, you can work backward to determine how much income and profit the business needs to generate to fund them. This transforms the business from just a job into a powerful wealth-creation engine.

Retirement Planning for the Business Owner

As a business owner, you don't have a corporate 401(k). You have to create your own retirement plan. Fortunately, there are several powerful options available:

- SEP IRA: Simple to set up and allows you to contribute up to 25% of your compensation, with a 2024 maximum of $69,000 (note: limits are adjusted annually by the IRS). It's funded solely by employer (your business) contributions.

- SIMPLE IRA: A good option if you have employees. It allows both employee and employer contributions, with a 2024 employee contribution limit of $16,000 (plus catch-ups for those over 50).

- Solo 401(k): An excellent choice for an owner-only business (or one that only employs a spouse). It allows you to contribute as both the "employee" and "employer," potentially reaching the same $69,000 total contribution limit as a SEP IRA but with more flexibility.

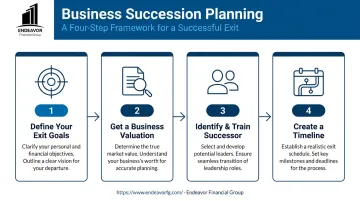

Creating Your Succession and Exit Plan

Every owner will exit their business one day. Whether you plan to sell to a third party, pass it down to family, or transition ownership to a key employee, you need a plan. A good succession plan is a multi-year process that includes:

- Defining Your Exit Goals: When do you want to leave and how much money will you need from the sale to fund your retirement?

- Getting a Business Valuation: You can't plan an exit until you know what your business is worth. A professional valuation provides an objective assessment.

- Identifying and Training a Successor: If you're passing the business on, start training your replacement years in advance.

- Creating a Timeline: Map out the key steps and milestones for a smooth and orderly transition.

Partnering with a Financial Professional for a Comprehensive Blueprint

Integrating complex business financials with personal wealth goals is where a dedicated financial professional becomes invaluable. A Certified Financial Planner™ (CFP®) who specializes in working with business owners can help you build a single, cohesive plan that aligns every decision with your ultimate objectives.

At Endeavor Financial Group, our team specializes in creating comprehensive financial plans for business owners here in Indiana. We understand that your business and personal finances are deeply intertwined, and our consultative, five-step process provides a clear roadmap for your future.

We act as the "quarterback" for your financial team, coordinating with your CPA and attorney to ensure your investment, tax, and estate strategies work together seamlessly. This helps build a secure financial future for both your company and your family.

Frequently Asked Questions

What is financial planning for construction business owners?

It's the process of managing your company's finances to achieve business goals while integrating them with your personal financial objectives. It covers everything from day-to-day cash flow and job costing to long-term retirement and succession planning.

How can I improve cash flow in my construction business?

The best tactics are to invoice promptly on project milestones, require upfront deposits on all jobs, follow up diligently on overdue receivables, and maintain a business line of credit for short-term gaps.

What are the most important financial metrics for a construction business to track?

Key metrics include Gross Profit Margin per project, Work-in-Progress (WIP) to monitor billing accuracy, cash flow, and a Budget vs. Actual cost report for every job.

What's the difference between a CPA and a financial planner for my business?

A CPA focuses on historical data like tax compliance and financial reporting. In contrast, a financial planner (such as a CFP®) creates a forward-looking strategy to help integrate your business and personal goals for retirement and succession.

What is the first step in creating a succession plan?

The first step is to define your personal exit goals, including when you want to leave and the financial resources you'll need. This is followed by getting a professional valuation of your business to establish a clear understanding of its current worth.

How much money do I need to work with a financial advisor?

It's more accessible than many business owners assume. Many advisory firms offer a complimentary initial consultation to discuss your needs and fee structure, focusing on creating a financial roadmap rather than meeting a specific account minimum.