This is where international estate tax planning comes in. It's the strategic process of arranging the transfer of your assets to minimize taxes and ensure your wishes are honored across borders. Without a plan, you risk double taxation, legal conflicts, and the serious erosion of your family's generational wealth. This guide will break down the core concepts, challenges, and key strategies you need to protect your legacy, no matter where in the world your assets or your loved ones are.

Key Takeaways

- Cross-border families need international estate plans to avoid double taxation.

- Your domicile (intent to remain) and asset situs (location) decide which tax laws apply.

- U.S. citizens are taxed on worldwide assets, while non-domiciliaries are only taxed on U.S. assets.

- Tax treaties, foreign credits, and specialized trusts are key tools for reducing tax liability.

- Success requires a coordinated team of international legal, tax, and financial experts.

Why International Estate Planning is Non-Negotiable

International estate tax planning is the legal and financial strategy for managing and transferring your worldwide assets upon death when you have connections to more than one country. Unlike domestic planning, which deals with federal and state laws, this adds layers of complexity, including different legal systems, conflicting tax regulations, and currency fluctuations.

The primary goals are to minimize global estate and gift taxes, ensure legal compliance in all relevant jurisdictions, and ensure your assets are transferred to the correct beneficiaries smoothly.

For cross-border families, inaction creates three major risks:

- Crippling Double Taxation: The most significant danger is having two or more countries claim the right to tax the same assets. For example, the U.S. may tax you based on citizenship, while your country of residence taxes you based on where you live. This can significantly reduce the inheritance your heirs receive.

- Unexpected Legal Conflicts: Legal systems vary widely. A U.S. will might not be fully recognized in a country with "forced heirship" rules, which legally require a portion of your estate to go to specific heirs (like children), regardless of what your will says. This can derail your intentions and lead to family disputes.

- Administrative Nightmares for Heirs: Without a clear plan, your heirs could face frozen assets, expensive multi-country probate, and overwhelming paperwork. Complex rules like the Foreign Account Tax Compliance Act (FATCA) add reporting burdens that can overwhelm a grieving family.

Core Concepts You Must Understand

Navigating international tax law requires a firm grasp of a few key terms. These concepts determine whose rules apply to your estate and which assets are subject to tax.

Domicile vs. Residency: The Deciding Factor

For U.S. estate tax purposes, domicile is far more important than residency. Residency is simply where you live. Domicile is your legal home—the place you intend to remain indefinitely. You can have multiple residences, but only one domicile.

This distinction is the cornerstone of U.S. estate taxation:

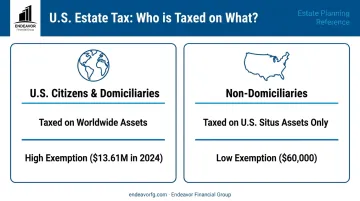

- U.S. Citizens and Domiciliaries: You are subject to U.S. estate tax on your worldwide assets, including property in the U.S. and abroad. However, you benefit from a very high federal exemption amount ($13.61 million in 2024), which is scheduled to decrease significantly after 2025.

- Non-Domiciliaries: If you are not a U.S. citizen and are not domiciled in the U.S., you are only taxed on your U.S.-situs assets. The trade-off is a drastically lower exemption—just $60,000.

Situs: Where Your Assets Legally Reside

"Situs" is the legal location of an asset for tax purposes. For a non-domiciliary, determining the situs of each asset is critical because it decides whether the U.S. can tax it.

Examples of U.S. Situs Assets:

- U.S. real estate (a condo in Miami, a house in California).

- Stock in U.S. corporations, even if you hold the certificates abroad.

- Tangible personal property located in the U.S. (art, vehicles, jewelry).

- Debt obligations of a U.S. person or government entity.

Examples of Non-U.S. Situs Assets:

- Stock in foreign corporations.

- Proceeds from life insurance policies.

- Deposits in U.S. banks that are not connected to a U.S. trade or business.

- Most U.S. government and corporate bonds (thanks to the "portfolio debt exemption").

Tax Treaties and Foreign Tax Credits

To prevent double taxation, the U.S. has estate and gift tax treaties with several countries, including the U.K., Germany, France, Canada, and Australia. These treaties can be a lifeline for international families.

They often provide "tie-breaker" rules to determine a single country of domicile for tax purposes. More importantly, they can offer significant benefits, like allowing a non-domiciliary from a treaty country to use a portion of the larger U.S. exemption instead of the standard $60,000.

If no treaty exists, U.S. law may still allow a foreign tax credit for estate taxes paid to another country on foreign-situs assets, though the rules for claiming this are complex.

Common Scenarios & Their Key Challenges

How these rules apply depends entirely on your family's situation. Here are three common scenarios and the unique challenges they present.

The U.S. Citizen Living Abroad (Expat)

As a U.S. citizen, you never escape the reach of the IRS. You remain subject to U.S. estate tax on your worldwide assets, no matter how long you've lived abroad. Your country of residence will also likely tax your assets, creating a clear risk of double taxation.

A standard U.S. will or revocable trust may not be recognized in your new home country, especially in civil law jurisdictions. This can lead to your assets being distributed according to local law, not your wishes.

The U.S. Citizen Married to a Non-U.S. Citizen

In the U.S., citizens benefit from an unlimited marital deduction, allowing them to transfer any amount of assets to their citizen spouse tax-free. This deduction does not automatically apply to transfers to a non-citizen spouse.

The primary solution is a Qualified Domestic Trust (QDOT). By transferring assets into a QDOT for the benefit of the surviving non-citizen spouse, you can defer the estate tax until that spouse's death. This allows the estate to function much like one with two citizen spouses, preserving wealth for the surviving partner.

The Non-U.S. Citizen with U.S. Investments

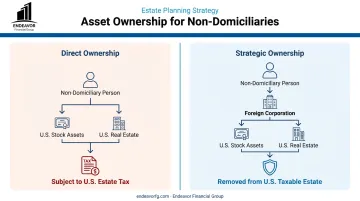

This is where the low $60,000 exemption becomes a major threat. If you are a non-domiciliary who owns U.S. stocks or real estate directly, your heirs could face a substantial and unexpected U.S. estate tax bill on the value of those assets exceeding $60,000.

A common strategy is to hold U.S. assets through a specific legal structure, such as a foreign corporation. This can potentially convert a U.S. situs asset (like U.S. stock) into a non-U.S. situs asset (stock in a foreign company), removing it from your U.S. taxable estate.

Disclaimer: This strategy is highly complex and has significant legal and tax implications. It absolutely requires guidance from qualified international tax and legal professionals.

Key Strategies for Managing International Estate Taxes

While the challenges are significant, several powerful strategies can help you protect your assets and provide for your family.

Utilizing Wills and Trusts Strategically

A single will is often insufficient for a global estate. Many families use multiple wills, known as "situs wills," with one for each country where they hold significant assets. This simplifies probate and ensures compliance with local laws. However, these wills must be carefully drafted by experts to avoid accidentally revoking one another.

Trusts are also powerful tools, but a standard U.S. trust can cause tax problems abroad. Specialized trusts, like the QDOT mentioned earlier, are designed for specific cross-border situations and are essential for tax efficiency.

Strategic Gifting and Ownership Structuring

Making lifetime gifts can reduce the size of your taxable estate. While gifts to non-citizen spouses don't qualify for the unlimited marital deduction, there is a generous annual exclusion. For 2024, you can give up to $185,000 to your non-citizen spouse gift-tax-free.

Beyond gifting, how you legally own an asset can also change its situs and tax treatment. Structuring ownership of U.S. assets through foreign entities is a sophisticated strategy that requires expert planning to be effective and compliant.

Leveraging Life Insurance

Life insurance can be a critical tool for providing the liquidity needed to pay estate taxes. The proceeds help your heirs in two key ways:

- Pay taxes without selling assets: Heirs receive immediate cash to cover tax liabilities, avoiding a forced sale of a family business or real estate.

- Avoid U.S. estate tax: For non-domiciliaries, life insurance proceeds are generally not considered U.S. situs assets and are therefore not subject to the tax.

Building Your Cross-Border Advisory Team

International estate planning is not a do-it-yourself project. The stakes are too high, and the rules are too complex. Assembling a qualified team of professionals is the most important step you can take.

This team should include:

- Estate planning attorney with demonstrated cross-border experience.

- Tax advisor or accountant who understands international compliance and treaties.

- Financial advisor who can manage global investments and see the big picture.

A comprehensive financial planning firm like Endeavor Financial Group often serves as the "quarterback" for this team. While we don't draft legal documents or prepare taxes, our primary role is to coordinate these moving parts.

We work with your legal and tax professionals to ensure every piece—from investment strategy to your will—fits into a cohesive plan. This integrated approach helps you achieve your long-term goals without costly oversights.

Frequently Asked Questions

What is the difference between residency and domicile for estate tax purposes?

Residency is based on your physical presence, while domicile is your legal home where you intend to remain indefinitely. For U.S. estate tax, domicile is the critical factor that determines how your worldwide assets are taxed.

How much is the U.S. estate tax exemption for a non-U.S. citizen?

A non-citizen domiciled in the U.S. shares the same exemption as a U.S. citizen (over $13 million). A non-domiciled non-citizen's exemption is only $60,000 for U.S. assets, though an estate tax treaty can increase this amount.

Can I use a U.S.-based trust for my international assets?

This is generally not advisable. A U.S. trust may not be recognized in other countries and could create negative tax consequences for foreign beneficiaries. It is crucial to use a structure that is valid in all relevant jurisdictions.

What is a QDOT and when is it needed?

A QDOT, or Qualified Domestic Trust, is a special trust used to defer U.S. estate tax when a U.S. citizen leaves assets to a non-U.S. citizen spouse. It allows the surviving spouse to benefit from the assets while delaying the tax until their death.

Do I need a will in each country where I own property?

It is often recommended to have separate "situs wills" for each country. This can simplify probate, reduce costs, and ensure compliance with local inheritance laws, but they must be carefully coordinated by an expert to avoid conflicts.

How do tax treaties affect international estate planning?

Tax treaties help prevent double taxation by setting rules for which country has the primary right to tax your estate. They can also provide significant benefits, such as offering a higher estate tax exemption for non-citizens from treaty countries.