The most significant tax you might face—capital gains tax—is only triggered when you sell the property. The good news? With the right knowledge and planning, you can often minimize this tax or even eliminate it entirely. This article breaks down the key concepts and actionable strategies you need to protect the full value of your inheritance.

TL;DR: Avoiding Capital Gains on Inherited Property

- Inheritance itself is tax-free; you only owe capital gains tax if you sell for a profit.

- A "stepped-up basis" resets the property's value to its market value on the date of death.

- You can minimize taxes by selling quickly, living in the home, or tracking improvements.

- Avoid gifting appreciated property before death, as it can create a large tax bill for heirs.

Understanding the Taxes on Inherited Property

When you inherit property, it's easy to get overwhelmed by tax jargon. The most important one to understand is capital gains tax, which is a tax on the profit you make from selling an asset. To understand it fully, you need to see how it differs from two other taxes you might encounter.

Capital Gains vs. Estate vs. Inheritance Tax

These three taxes are often confused, but they apply to different people at different times.

- Capital Gains Tax: Paid by you, the heir, only when you sell the inherited property for a profit. This is the tax you have the most control over.

- Estate Tax: Paid by the deceased's estate before you receive the assets. This only applies if the estate's total value exceeds a very high federal threshold. For 2026, that exemption amount is $15 million per individual, meaning the vast majority of estates owe nothing.

- Inheritance Tax: Paid by the heir upon receiving assets. This tax is rare and only exists in five states as of 2026: Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania.

For most people, capital gains tax is the only one they need to plan for.

The Stepped-Up Basis: Your Most Powerful Tax-Saving Tool

The most important concept for an heir is the "stepped-up basis." When you inherit property, the IRS allows its cost basis to be "stepped up" to its Fair Market Value (FMV) on the date of the original owner's death.

This rule effectively erases decades of appreciation for tax purposes.

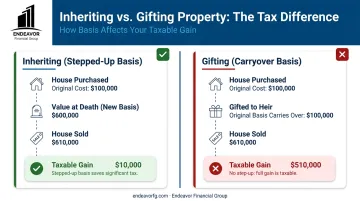

Here’s a clear example: Imagine your parents bought a home for $100,000. It’s worth $600,000 when they pass away. Your new cost basis isn't $100,000; it becomes $600,000.

If you turn around and sell it for $610,000, you only owe capital gains tax on the $10,000 profit—not on the $510,000 gain that occurred during your parents' lifetime.

How Capital Gains are Calculated

Your taxable gain is calculated with a simple formula:

Sale Price - Stepped-Up Basis - Cost of Improvements - Selling Costs = Taxable Gain

If the result is negative, you have a capital loss. If the property was used as an investment (e.g., a rental), you can often use that loss to offset other investment gains. However, according to the IRS, if you sell a personal-use property like a primary home for a loss, that loss is not deductible.

The Financial Impact of Mismanaging Your Inheritance

Mismanaging an inherited property can have a steep financial cost. Without a clear tax strategy, you could face a substantial tax bill that consumes a large portion of the inheritance, often forcing a quick sale or causing disputes among family members.

The stakes are high—an uninformed decision can easily cost tens or even hundreds of thousands of dollars in preventable taxes.

Common Mistakes That Trigger Unnecessary Taxes

Avoiding a big tax bill is often about sidestepping a few common but costly errors.

Gifting Property Instead of Inheriting It

Well-meaning parents sometimes decide to gift their home to their children while they are still alive to avoid probate. This is usually a massive tax mistake.

Gifted property comes with a "carryover basis," meaning the recipient takes on the original owner's cost basis. In our earlier example, if the parent gifted the $600,000 house, the child would inherit the original $100,000 basis.

A subsequent sale at $610,000 would result in a taxable gain of $510,000. By inheriting the property instead, the taxable gain would have been just $10,000.

Ignoring Capital Improvements

It's crucial to keep detailed records of any major improvements made after inheriting the property. A new roof, a kitchen remodel, or a new HVAC system all increase your cost basis, which in turn reduces your taxable gain when you sell. Forgetting to track these expenses is like leaving money on the table.

Selling Too Late Without a Strategy

While selling a property immediately after inheritance often results in little to no tax, holding it for several years allows it to appreciate further. This creates a potential tax liability that requires a plan.

For example, if you sell five years later for $700,000, you now have a $100,000 taxable gain ($700k sale price - $600k stepped-up basis). This outcome isn't necessarily bad, but it must be planned for.

Key Strategies to Legally Avoid or Minimize Capital Gains Tax

Several IRS-approved strategies can help you legally protect your inheritance from capital gains taxes.

Strategy 1: Sell the Property Quickly

The simplest approach is often the best. Selling the property within a few months of inheriting it usually means the sale price will be very close to the stepped-up basis established at the time of death. When you factor in selling costs like realtor commissions, the net result is often a small gain or even a slight loss, which means your tax bill will be minimal or zero.

Strategy 2: Make it Your Primary Residence

This is a powerful strategy if you plan to hold onto the property. The Section 121 Exclusion, also known as the Primary Residence Exclusion, allows you to exclude a significant amount of capital gains from your income.

To qualify, you must own and live in the property as your main home for at least two of the five years leading up to the sale.

- Single filers can exclude up to $250,000 of capital gains.

- Married couples filing jointly can exclude up to $500,000.

By moving into the inherited home and meeting this requirement, you could shelter years of future appreciation from taxes.

Strategy 3: Document All Capital Improvements

Any money you spend to substantially improve the property adds to your basis. It’s vital to distinguish between improvements and simple repairs.

- Capital Improvements: These add to your basis and include projects that add significant value or prolong the property's life, like a new roof, a kitchen remodel, or finishing a basement.

- Repairs and Maintenance: These do not add to your basis. They simply keep the property in good working order, such as painting a room, fixing a minor leak, or replacing a broken window pane.

Keep every receipt for improvements. Each dollar you document is a dollar less that the IRS can tax.

Strategy 4: Sell at a Loss (for Investment Properties)

If the real estate market dips after you inherit an investment property, its value might fall below the stepped-up basis. Selling it would result in a capital loss. This loss can be used to offset capital gains from other investments, such as stocks, and up to $3,000 per year can be used to offset your regular income.

Strategy 5: Consider a 1031 Exchange (For Investment Properties)

If you inherit a rental or commercial property and want to continue being a real estate investor, a 1031 exchange is a powerful tool. It allows you to sell the property and roll the entire proceeds into a new, "like-kind" investment property without paying immediate capital gains tax. This is a tax deferral, not elimination. The tax is eventually due when you sell the replacement property, but you can potentially defer it for years.

Strategy 6: Rent Out the Property

Converting the house into a rental property avoids an immediate capital gains event. It turns the asset into an income stream (which is taxable as ordinary income) and allows you to take deductions for expenses like maintenance, property taxes, and depreciation. If you convert the home to a rental, you can begin depreciating it based on its fair market value at the time you inherited it, creating another valuable tax deduction.

Proactive Planning: Long-Term Tips for Estate Holders

Property owners can significantly minimize an heir's future tax burden through proactive planning.

Tip 1: Keep Meticulous Records

Property owners should keep detailed records of the original purchase price and all capital improvements made over the years. While the basis is stepped up at death, these records are invaluable for simplifying estate administration and ensuring a smooth asset transfer.

Tip 2: Consider Using a Trust

Placing property in a revocable living trust is an excellent estate planning tool. While it doesn't eliminate capital gains tax, a trust offers two key advantages:

- It avoids probate, a lengthy and often expensive court process, allowing heirs to manage or sell the property much more quickly.

- Assets in a revocable trust still receive a stepped-up basis at death, preserving this critical tax benefit.

Tip 3: Get a Professional Appraisal

To establish a clear, defensible stepped-up basis, the estate's executor should get a formal appraisal of the property as of the date of death. This provides the IRS with clear documentation of the fair market value and prevents future disputes about the basis calculation.

Secure Your Legacy with Strategic Planning

Inheriting property doesn't have to mean losing a chunk of its value to taxes. By understanding the power of the stepped-up basis and using the right strategies, you can preserve your family's legacy and make the most of your inheritance. Proactive planning, both by the person leaving the property and the heir receiving it, is the key to a smooth and tax-efficient transfer of wealth.

Navigating the complexities of estate settlement, tax law, and investment decisions during an emotional time can be overwhelming.

The financial professionals at Endeavor Financial Group specialize in creating holistic wealth plans that help families manage inheritances strategically. As fiduciaries with CFP® designations, we coordinate with your legal and tax teams to ensure your financial plan protects your assets and secures your future.

Frequently Asked Questions

Optimize Estate Planning to Minimize Inheritance Tax Burdens

Request a quote and our experts will contact you within 24 hours with tailored solutions and pricing.

For immediate assistance, feel free to give us a direct call at 463-273-4062. You can also send us a quick email at team@endeavorfg.com.

For immediate assistance, feel free to give us a direct call at 463-273-4062. You can also send us a quick email at team@endeavorfg.com.