Navigating the world of retirement plans designed for the self-employed and small businesses can feel like a second job. The acronyms are confusing, the rules are complex, and choosing the wrong plan can mean leaving significant tax advantages and growth potential on the table.

This guide is designed to cut through the noise. We'll break down the top retirement plan options—the SEP IRA, SIMPLE IRA, and 401(k)—and provide a clear framework for choosing the best fit for you and your business.

TL;DR: Key Retirement Plan Takeaways

- Tax deductions are a primary benefit. Contributions you make for yourself and your employees are generally tax-deductible, lowering your business's taxable income.

- The "Big Three" plans are the SEP IRA (flexible, employer-only funding), the SIMPLE IRA (easy employee/employer plan), and the 401(k) (most powerful and flexible).

- Your business size and goals matter most. A Solo 401(k) is great for one, a SEP IRA for variable income, and a 401(k) for maximizing savings and attracting talent.

- Contribution limits vary significantly. For 2026, a Solo 401(k) owner can potentially save up to $72,000, while a SEP IRA has the same cap and a SIMPLE IRA is lower.

- Don't go it alone. Choosing and managing a plan requires aligning business strategy with personal financial goals, a process best navigated with professional guidance.

Why a Retirement Plan is a Non-Negotiable Business Asset

For a business owner, a retirement plan goes beyond being an employee benefit—it's a critical tool for wealth creation. It serves two essential functions: securing your own financial independence and giving your business a competitive edge.

The Power of Tax Advantages

One of the most immediate benefits of establishing a retirement plan is the tax savings. Contributions your business makes to employee accounts, including your own, are typically tax-deductible. This directly reduces your company's taxable income for the year.

This frees up capital that can be reinvested into the business or used to fund your retirement further. Plans like the SEP IRA, SIMPLE IRA, and 401(k) were designed by the IRS specifically to reward businesses for saving.

Attracting and Retaining Top Talent

In a tight labor market, benefits matter. A retirement plan can be the deciding factor for a high-value candidate choosing between your company and a competitor. In fact, a 2024 survey from the Employee Benefit Research Institute (EBRI) found that 90% of small business owners who offer a retirement plan do so to gain a competitive advantage in recruitment and retention.

When employees feel their long-term future is valued, they are more engaged and more likely to stay. This reduces turnover costs and helps you build a stable, experienced team to drive your business forward.

The "Big Three" Retirement Plans for Business Owners

While there are several types of plans, most business owners will find their perfect fit among three main options. Let's break them down.

A Simplified Employee Pension (SEP) IRA

A SEP IRA is one of the most straightforward retirement plans available. Only the employer contributes to the plan, making it simple to administer. You, as the owner, decide what percentage of compensation to contribute each year for yourself and any eligible employees.

Contribution rules are flexible. You can contribute up to 25% of compensation, with a maximum of $69,000 for 2024. A key advantage is that you can choose to skip contributions entirely in lean years, offering a safety valve for businesses with unpredictable cash flow.

SEP IRAs are ideal for self-employed individuals, freelancers, and small business owners with few or no employees. The plan's low administrative burden and contribution flexibility make it a popular starting point.

A Savings Incentive Match Plan for Employees (SIMPLE) IRA

A SIMPLE IRA is designed for small businesses (typically 100 or fewer employees) and allows both employees and the employer to contribute. This structure encourages employees to save for their own retirement, with the company providing a guaranteed contribution.

For 2024, employees can contribute up to $16,000 per year, with an additional $3,500 catch-up contribution for those age 50 and over. Employers are required to contribute via one of two methods:

- A dollar-for-dollar match up to 3% of an employee's compensation.

- A 2% non-elective contribution for all eligible employees, regardless of whether they contribute themselves.

This plan is a great fit for small businesses that want to foster a culture of saving through matching contributions. It has a lower administrative burden than a 401(k) but requires a mandatory employer contribution each year.

A 401(k) Plan (Including the Solo 401(k))

The 401(k) is the most powerful and flexible retirement plan. It offers the highest contribution limits and advanced features like the ability for participants to take out loans. It supports both pre-tax and Roth (post-tax) employee contributions, giving savers more control over their tax strategy.

For 2024, employees can defer up to $23,000 of their salary, with a $7,500 catch-up for those 50 and older. The total combined employer and employee contributions can reach up to $69,000.

The Solo 401(k): A special version of the 401(k), designed for business owners with no employees other than a spouse, allows you to contribute as both the "employee" and the "employer." This dual contribution structure lets you maximize your personal savings far beyond what's possible with other plans.

A traditional 401(k) is for established businesses ready to offer a top-tier benefit. The Solo 401(k) is the ultimate savings vehicle for self-employed individuals or husband-and-wife partnerships who want to save as much as possible for retirement.

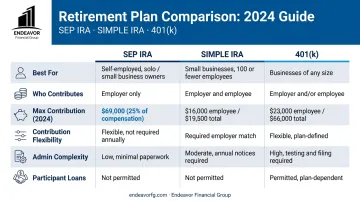

At a Glance: SEP IRA vs. SIMPLE IRA vs. 401(k)

Here’s a quick-reference table to help you compare the core features of the three main plan types.

| Feature | SEP IRA | SIMPLE IRA | 401(k) / Solo 401(k) |

|---|---|---|---|

| Best For | Sole proprietors, freelancers, businesses with variable cash flow | Small teams (<100 employees) wanting an easy-to-manage matching plan | Growing businesses & owners wanting to maximize personal savings |

| Who Contributes? | Employer only | Employee & Employer | Employee & Employer (Owner can be both in a Solo 401(k)) |

| Max. Owner Contribution (2024) | 25% of compensation, up to $69,000 | $16,000 (employee) + employer match | $23,000 (employee) + employer portion, up to $69,000 total |

| Contribution Flexibility | High (can skip years) | Low (mandatory employer contribution) | Moderate to High (employer contributions are often optional) |

| Admin. Complexity | Low | Low to Moderate | High (Form 5500 filing often required); Moderate for Solo 401(k) |

| Participant Loans Allowed? | No | No | Yes (if the plan document allows) |

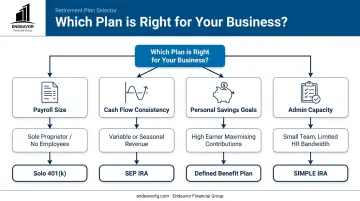

How to Choose the Right Retirement Plan for Your Business

Selecting a retirement plan is a strategic decision that should be based on your company's structure, goals, and your personal financial picture. Here are the key factors to consider.

1. Who Is On Your Payroll?

Your current and future headcount is a major driver.

- Are you a sole proprietor or just have a spouse on payroll? The Solo 401(k) is likely your best bet for maximizing personal savings.

- Do you have a small, stable team? A SIMPLE IRA is excellent for encouraging employee participation with a mandatory match.

- Do you have no employees or do you hire occasional contractors? The SEP IRA offers simplicity and the flexibility to skip contributions when cash is tight.

- Are you planning to grow your team significantly? A traditional 401(k) provides the most scalability and design flexibility as your company evolves.

2. How Consistent Is Your Cash Flow?

Consistent profitability makes it easier to commit to mandatory contributions. A business with fluctuating income needs more flexibility.

- Variable or seasonal income: The SEP IRA is a strong choice because you can adjust contributions based on annual profits or skip them entirely.

- Steady, predictable cash flow: The mandatory contributions of a SIMPLE IRA are manageable, and a 401(k) allows for consistent employer matching.

- Highly profitable years: A 401(k) with a profit-sharing component allows you to make large, discretionary contributions to yourself and your employees as a reward for a great year.

3. What Are Your Personal Savings Goals?

How much do you, the owner, want to save for your own future? If your top priority is to contribute as aggressively as possible, your choice of plan becomes clearer.

The Solo 401(k) and traditional 401(k) plans almost always allow for the highest personal contribution limits, thanks to the ability to contribute as both employee and employer and the high overall caps.

4. How Much Administration Can You Handle?

Be realistic about how much time and money you can dedicate to plan administration.

- Low-touch and simple: The SEP IRA is the easiest to set up and maintain, with minimal annual paperwork.

- Slightly more involved: A SIMPLE IRA has more moving parts due to employee deferrals and mandatory matching but is still far less complex than a 401(k).

- Most complex: A traditional 401(k) comes with annual compliance testing, reporting (Form 5500), and higher administrative costs. A Solo 401(k) is simpler but still requires filing a Form 5500-EZ once plan assets exceed $250,000.

Navigating these options is a cornerstone of your financial strategy. A financial professional can help you select a plan that aligns with both your business objectives and personal wealth goals, which is the specialized guidance our team at Endeavor Financial Group provides.

Your Next Step: Building a Retirement Strategy with a Professional

Choosing a plan is just the first step. Implementing it correctly and managing it effectively is what ensures long-term success. Your business should serve your life goals, not the other way around, and a well-designed retirement strategy is key to making that happen.

At Endeavor Financial Group, we specialize in creating personalized financial plans for small business owners right here in Indiana. We understand that your business and personal finances are deeply intertwined.

Our consultative approach is built on a structured five-step process: discovery and analysis, implementation, and ongoing monitoring. This ensures you get a clear roadmap to financial freedom that evolves as your business and life change.

If you're ready to build a retirement plan that truly works for you, let's have a conversation. Schedule a consultation with our team today.

Frequently Asked Questions

How do business owners retire?

They retire by building value in their business for a future sale while also funding dedicated retirement accounts like a SEP IRA or 401(k). This strategy creates a personal nest egg that grows in a tax-advantaged environment, independent of the business.

Can an LLC have a retirement plan?

Yes, absolutely. An LLC, whether it's a single-member or multi-member entity, is eligible to establish any of the major retirement plans, including SEP IRAs, SIMPLE IRAs, and 401(k)s, for its owners and employees.

What is the easiest retirement plan for a new business owner?

The SEP IRA is often the easiest plan for new owners. It involves minimal paperwork, has low administrative costs, and offers flexible contributions, which is ideal for a business in its early years.

Can I have a Solo 401(k) and a personal Roth IRA?

Yes, you can contribute to both a Solo 401(k) and a personal IRA (Traditional or Roth) in the same year. Just be aware that your eligibility to contribute to a Roth IRA is subject to IRS income limits.

What happens to my business retirement plan if I hire employees?

A Solo 401(k) must be converted to a traditional 401(k) to include new employees. For SEP and SIMPLE IRAs, you simply need to add eligible employees to the existing plan according to its rules.

What is a SEP IRA?

A SEP IRA is a simple retirement plan where only the employer (or self-employed individual) makes contributions for themselves and their employees. It's popular for its low administrative costs and flexible, non-mandatory funding.