This new phase requires a different mindset and a deliberate strategy. The choices you make now will determine how you turn your nest egg into a reliable paycheck for the rest of your life. This article explores several proven retirement income strategies, explains how they work, and provides a framework for choosing the best approach for your unique situation.

Key Takeaways

- Generating lasting income from a $1M portfolio requires a clear strategy to manage key risks.

- Explore popular methods like the 4% Rule, the Bucket Strategy, or a Total Return approach.

- Select a strategy based on your personal risk tolerance, income needs, and legacy goals.

- Create a plan that accounts for taxes, healthcare costs, and appropriate investment risk.

Putting Your $1 Million into Perspective: Is It Enough?

While $1 million is a substantial sum, its longevity depends heavily on your lifestyle, location, and withdrawal rate. Using the well-known "4% rule" as a simple baseline, a $1 million portfolio could generate an initial income of around $40,000 per year. For many, that’s a solid foundation, but it’s not invincible.

Several key factors can erode the value of your savings over a 20 or 30-year retirement, and your plan must account for them.

Inflation

The rising cost of living is a silent portfolio killer. A fixed income today will buy significantly less in 10 or 20 years. For example, the average U.S. inflation rate over the last 30 years has been around 2.5%. That rate is enough to cut your money's purchasing power in half in under 30 years. Your income strategy must be designed to grow, not just hold steady.

Longevity

People are living longer than ever, which means retirement funds must also last longer. A retirement of 30 years or more is now common. For a 65-year-old couple today, there is a 46.7% chance that at least one of them will live to age 90. Your plan must be built for this longer timeline, not on outdated life expectancy assumptions.

Lifestyle and Healthcare Costs

Retirement spending isn’t a flat line. It often follows a pattern financial planners call the “go-go, slow-go, and no-go” years. You may spend more on travel and hobbies early on (go-go), slow down in the middle years (slow-go), and then see costs rise again due to healthcare needs later in life (no-go).

Healthcare is one of the biggest wild cards. According to Milliman, a healthy 65-year-old couple retiring this year may need an estimated $388,000 in savings to cover healthcare expenses in retirement. This significant potential expense must be factored into any durable income plan.

Key Retirement Income Strategies for a $1 Million Portfolio

Key Retirement Income Strategies for a $1 Million Portfolio

There is no single "best" strategy for generating retirement income. The best approach often blends these methods to create a plan tailored to your specific goals and risk tolerance. Here are four of the most effective strategies to consider.

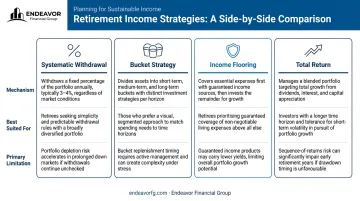

The Systematic Withdrawal Strategy

In this traditional approach, you withdraw a specific percentage or dollar amount from your portfolio each year to live on, leaving the rest invested.

- How it Works: The most famous version is the "4% Rule," which suggests withdrawing 4% of your portfolio in your first year of retirement and then adjusting that dollar amount for inflation each year. Modern variations include dynamic withdrawals, where you might take less in down market years and more in up years.

- Best Suited For: Retirees who want simplicity, flexibility, and the potential for portfolio growth to leave a legacy.

- Key Strengths: It’s easy to understand and implement, provides full access to your capital, and can lead to a growing nest egg in favorable markets.

- Limitations: This strategy is vulnerable to sequence of returns risk. Retiring into a bear market and selling assets at low prices can deplete your portfolio much faster than anticipated.

The Bucket Strategy

This strategy involves segmenting your assets into different "buckets" based on when you'll need the money. It’s designed to provide psychological comfort by separating your short-term needs from long-term growth assets.

- How it Works: A common setup uses three buckets:

- Bucket 1 (1-3 years of expenses): This holds cash, high-yield savings, and other ultra-safe assets to cover your immediate living expenses. It’s insulated from market volatility.

- Bucket 2 (4-10 years of expenses): This contains a conservative mix of bonds and low-volatility stocks. Its job is to generate modest returns and periodically refill Bucket 1.

- Bucket 3 (11+ years of expenses): This is your growth engine, invested in a diversified portfolio of stocks and ETFs designed for long-term appreciation.

- Best Suited For: Retirees who feel anxious about market swings and want peace of mind knowing their near-term income is secure.

- Key Strengths: It helps prevent emotional, panic-driven decisions during market downturns and provides a clear structure for managing your assets.

- Limitations: It can be more complex to manage than a single portfolio and may lead to a "cash drag"—holding too much in low-return assets, which can hurt your portfolio's overall growth.

The Income Flooring (or "Hybrid") Strategy

This approach focuses on creating a reliable income "floor" to cover your essential, non-negotiable expenses like housing, food, and healthcare.

How it Works: You use a portion of your portfolio to secure guaranteed income sources, such as a single premium immediate annuity (SPIA), which provides a pension-like payment for life.

This guaranteed income, combined with Social Security and pensions, creates your "floor." The rest of your assets are invested for growth to cover discretionary spending and combat inflation.

Best Suited For: Risk-averse retirees who prioritize certainty and want to ensure their basic needs are always met, no matter what the market does.

Key Strengths: It provides absolute peace of mind for essential costs and protects you from outliving your money (longevity risk).

Limitations: Annuities require you to give up control and liquidity (easy access to your cash) over a portion of your assets. Fixed annuity payments can also lose purchasing power over time unless you buy a more expensive inflation-adjusted rider.

The Total Return Investing Strategy

This flexible approach focuses on the overall growth of your portfolio from both capital gains and dividends. You generate income by selling assets as needed.

- How it Works: Instead of building a portfolio designed only to produce interest and dividends, you invest in a diversified growth-oriented portfolio. When you need income, you strategically sell appreciated assets. This gives you more control over the timing and tax implications of your withdrawals.

- Best Suited For: Sophisticated retirees who are comfortable managing their investments and want maximum flexibility and growth potential.

- Key Strengths: It's highly flexible, allows for tax-loss harvesting and strategic selling, and isn't limited by the dividend yield of your investments.

- Limitations: It requires active management and a solid understanding of tax planning. It can also be emotionally challenging to sell assets, especially during a market downturn.

How to Choose the Right Retirement Income Strategy

The best plan is rarely one-size-fits-all. It’s usually a personalized blend of the strategies above, tailored to your unique circumstances. As you build your plan, consider these key factors:

- Your tolerance for risk. If a 20% portfolio drop is unsettling, an income floor is a good fit. If not, a total return approach could work well.

- The difference between needs and wants. Cover essential needs with guaranteed income and use invested assets to fund discretionary wants.

- Your desire to leave a legacy. To leave money for others, choose strategies that preserve your principal rather than spending down assets with annuities.

- Your health and expected longevity. A long life expectancy may call for a more conservative withdrawal rate or an annuity for protection.

- The tax implications of your accounts. A tax-efficient withdrawal plan is a necessity, as your after-tax income is shaped by your account types (401k, Roth, etc.).

Navigating these complexities is challenging. Working with a Certified Financial Planner (CFP®) can provide the clarity and confidence you need. At Endeavor Financial Group, our five-step process is designed to create a clear roadmap that aligns your income strategy with your life goals, from discovery to ongoing monitoring.

Common Mistakes to Avoid When Finalizing Your Strategy

As you put the finishing touches on your plan, be careful to sidestep these common pitfalls.

Overlooking Tax Implications

Withdrawing from your accounts in the wrong order can cost you thousands in unnecessary taxes over your lifetime. A good rule of thumb is to withdraw from your accounts in this sequence:

- Taxable brokerage accounts

- Tax-deferred accounts (Traditional IRAs, 401(k)s)

- Tax-free accounts (Roth IRAs)

This allows your tax-advantaged accounts to continue growing for as long as possible. A professional can help you create a dynamic withdrawal plan that minimizes your lifetime tax bill.

Being Too Conservative or Too Aggressive

Retirees often swing to one of two extremes. Some, fearing market loss, move everything to cash—a losing battle, as inflation will steadily erode their purchasing power.

Others remain too aggressive, keeping their portfolio 100% in stocks. This approach exposes them to severe sequence of returns risk early in retirement. A balanced, diversified portfolio is the most reliable path.

Forgetting About Healthcare and Long-Term Care

Healthcare costs are a massive and unpredictable expense. Medicare doesn't cover everything, and the need for long-term care—whether at home or in a facility—can quickly deplete even a seven-figure portfolio.

Your retirement plan must include a specific strategy for funding these potential costs.

Your Next Chapter Awaits

Reaching the $1 million mark is the end of one journey and the beginning of another. Building a durable income plan is the critical next step to ensure the wealth you've built can support the life you want to live.

The best strategies—Systematic Withdrawals, Buckets, and Flooring—are tools, not rigid rules. The right approach for you will be a customized blend that reflects your goals, your risk tolerance, and your vision for the future. This level of thoughtful planning provides the financial confidence you need to enjoy it.

At Endeavor Financial Group, we specialize in the strategic wealth planning required to navigate this transition successfully. If you’re ready to build a clear roadmap for your retirement income, contact our team to get started.

Frequently Asked Questions

How to generate income when my portfolio reaches $1 million?

Income can be generated through systematic withdrawals from your invested assets, collecting dividends and interest, strategically selling investments, or purchasing an annuity for a guaranteed stream of payments. The best method depends on your individual goals and risk tolerance.

How much monthly income does a $1 million retirement portfolio produce?

Using the 4% rule as a guideline, a $1 million portfolio can produce about $40,000 per year, or roughly $3,333 per month. This amount can vary significantly based on your chosen strategy, market performance, and tax implications.

What is the 4% rule for retirement?

The 4% rule is a guideline stating you can withdraw 4% of your portfolio in the first year of retirement and then adjust that dollar amount for inflation in subsequent years. It's a starting point for planning, not a set-it-and-forget-it rule.

How do taxes impact retirement income withdrawals?

Withdrawals from traditional IRAs/401(k)s are taxed as ordinary income, while qualified Roth withdrawals are tax-free. Selling assets in a taxable account triggers capital gains tax. A strategic withdrawal plan is essential to minimize your lifetime tax burden.

Should I use my retirement funds to pay off my mortgage?

While paying off a mortgage provides security, it also reduces your portfolio's liquidity and growth potential. The decision depends on whether your expected investment returns are likely to be higher than your mortgage interest rate.

How does Social Security fit into my retirement income plan?

Social Security provides a reliable, inflation-adjusted income stream that serves as a financial foundation in retirement. When you claim benefits significantly impacts your lifetime income, so it must be coordinated with your portfolio withdrawal plan.