Most pre-retirees understand diversification conceptually. Fewer actually have portfolios built to handle the specific risks retirement introduces: longevity stretching 20–30 years, inflation steadily eroding purchasing power, and the sequence-of-returns problem that can permanently impair a portfolio in its earliest withdrawal years.

This article breaks down what portfolio diversification actually means in a retirement context, why it matters more than most people realize, and how to build a strategy that holds up through market cycles.

Key Takeaways

- Diversification in retirement means spreading investments across asset classes, sectors, and geographies so no single market event derails your income

- The goal shifts from maximizing returns to reducing volatility while maintaining enough growth to outlast your lifespan

- Sequence-of-returns risk (early portfolio losses during the withdrawal phase) is the primary threat a diversified strategy guards against

- Without regular rebalancing, even a well-designed diversification strategy drifts out of alignment over time

- Comprehensive planning covers taxes, Social Security timing, and estate coordination — not just which assets you hold

What Is Portfolio Diversification for Retirement?

Portfolio diversification means holding a mix of investment types that don't all move in the same direction at the same time. When one position falls, others may hold steady or rise, limiting the damage to your overall plan.

That definition applies at any age. What changes in retirement is how costly getting it wrong can be.

Accumulation vs. Drawdown — A Critical Difference

During your working years, you're continuously adding money to your portfolio. A bad year in the market gets offset by the following year's contributions and the recovery that typically follows. You have time and cash flow working in your favor.

In retirement, that buffer disappears. You're withdrawing funds, not adding them. A significant loss early in retirement — when your portfolio is at its largest and your withdrawals are just beginning — can permanently reduce how much income that portfolio can generate for the next 20 or 30 years.

This is why diversification in retirement isn't a return-maximizing strategy. It's a risk management strategy — one designed to protect your income and reduce the chance of panic-driven decisions during downturns.

The goal isn't simply growth. A well-diversified retirement portfolio is built to keep generating reliable income even when parts of the market are struggling — and that distinction shapes every allocation decision that follows.

Key Benefits of a Diversified Retirement Portfolio

The benefits below matter most in the retirement context because the consequences of undiversified losses are largely irreversible — you no longer have decades of future contributions to compensate for a bad year.

Reduced Volatility and Emotional Stability

Combining assets with low or negative correlation smooths out portfolio performance over time. When domestic equities fall, international bonds may hold. When growth stocks drop, dividend-paying value stocks often fare better.

Since 1960, the average correlation between stocks and bonds has been approximately 0.08, according to Morningstar — meaning they tend to move largely independently. This is the mechanical basis for diversification's risk-reduction effect.

The behavioral benefit is equally important. Emotional investing — selling during downturns and buying back during recoveries — consistently costs retirees returns. DALBAR's research found that in 2024, the average equity investor earned 16.54% while the S&P 500 returned 25.02% — an 8.48 percentage-point gap driven largely by mistimed buying and selling behavior.

A diversified portfolio that doesn't swing as dramatically gives retirees the confidence to stay the course. For most retirees, that staying power matters more than chasing theoretical return optimization.

Protection Against Sequence-of-Returns Risk

Sequence-of-returns risk is the danger that early losses in retirement — precisely when withdrawals begin — can permanently impair a portfolio's ability to sustain income for decades, even if long-run average returns look acceptable.

The math is stark. Morningstar modeled a retiree who entered 2000 with $1,000,000, an all-equity portfolio, and $40,000 in annual inflation-adjusted withdrawals. Hit by two major crashes in three years, the portfolio had declined to roughly $644,000 by age 85. If those same returns had occurred in reverse order, the portfolio would have reached nearly $2.7 million — same average returns, drastically different outcomes.

A retiree starting before 2000 with a 60% stock / 40% bond portfolio, rebalanced annually, fared better. After the 2008 collapse, that balanced portfolio held around $729,000 and recovered to approximately $1.2 million by age 84.

The diversified allocation didn't eliminate the pain of two major crashes. It made the difference between recovery and permanent impairment.

The years immediately before and after retirement are the highest-risk window. This is when diversification's protective value is at its peak.

Income Stability and Longevity Protection

Retirement isn't a five-year horizon — it's potentially a 30-year funding challenge. According to J.P. Morgan Asset Management's 2026 Guide to Retirement, a 65-year-old woman has a 54% probability of living to age 90, and a 65-year-old man has a 42% probability. The SSA's actuarial tables show remaining life expectancy at 65 is already 17.5 years for men and 20.1 years for women — those are averages, not ceilings.

A portfolio that only protects against short-term volatility but ignores inflation will fail that longevity test. A steady 2% annual inflation rate reduces the purchasing power of $100,000 to $67,000 over 20 years, per Vanguard. Healthcare costs compound the problem further — J.P. Morgan data shows they rose at an average of 4.4% annually from 1982 to 2025, compared to 2.9% overall inflation.

A diversified portfolio addresses this by combining multiple income streams:

- Dividend-paying stocks — regular income with growth potential that can pace inflation

- Bonds and fixed income — predictable interest payments that stabilize cash flow during equity downturns

- REITs — real estate exposure with legally mandated dividend payouts (at least 90% of taxable income)

No single asset class handles all three retirement income needs — stability, growth, and inflation protection — simultaneously. Building across asset types, not just across individual securities, is what gives a retirement portfolio its durability over a 20- to 30-year draw-down period.

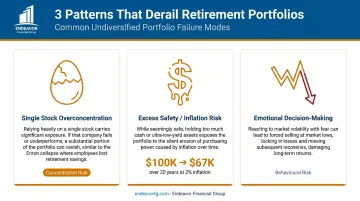

What Happens When Retirees Skip Diversification

The consequences of an undiversified retirement portfolio aren't hypothetical. They show up in three predictable patterns:

Overconcentration in a single stock or sector. Employees who spent careers accumulating employer stock often enter retirement with outsized concentration in one company. The Enron case remains the clearest example: 62% of assets in Enron's 401(k) plan were held in company stock as of December 31, 2000. When the company collapsed, the U.S. Department of Labor filed a $356.25 million bankruptcy claim against those retirement plans.

The people who lost most weren't reckless speculators. They were employees following a pattern millions still repeat today.

Excess "safety" that creates inflation risk. Holding too much cash or fixed income carries its own risk — just a quieter one. During inflationary periods, U.S. large-cap stocks have posted nominal returns of about 3% per year and core bonds approximately 2.2%, according to Morningstar. Neither keeps pace with real spending needs, especially in healthcare-heavy retirement years.

Emotional decision-making under pressure. When a concentrated portfolio drops 30%, retirees face a choice no one wants: hold through the pain or sell at a loss and lock in permanent damage. A diversified portfolio rarely requires that choice because the drawdowns are smaller and more manageable.

Each of these patterns is avoidable. The next section covers how a diversified portfolio is structured to prevent them.

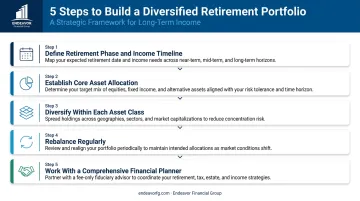

How to Build a Diversified Retirement Portfolio Strategy

Step 1: Define Your Retirement Phase and Income Timeline

A 62-year-old still five years from retirement needs a fundamentally different allocation than a 72-year-old actively drawing down assets. The starting point of any diversification strategy is a clear picture of when income begins, how much you'll need, and how long it must last.

This phase assessment shapes every subsequent decision — asset allocation, income sequencing, and rebalancing thresholds.

Step 2: Establish Core Asset Allocation

The general principle: the closer you are to or in retirement, the more the portfolio shifts from growth-focused to income-and-stability-focused. This is the classic "glide path" concept — gradually reducing equity exposure and increasing bond and income-generating asset exposure as retirement approaches and progresses.

Common allocation frameworks fall into three broad categories:

| Framework | Equity Range | Bond/Stable Range | Best Suited For |

|---|---|---|---|

| Aggressive | 70–80% | 20–30% | Pre-retirees 10+ years out |

| Moderate | 50–60% | 40–50% | Near-retirees and early retirees |

| Conservative | 30–40% | 60–70% | Active drawdown, shorter horizons |

No single allocation suits every retiree. Risk tolerance, health, income sources, and spending needs all affect where you should land.

Step 3: Diversify Within Each Asset Class

True diversification goes deeper than "stocks and bonds." Within equities, that means:

- Different sectors (technology, healthcare, consumer staples, utilities)

- Different market caps (large-cap, mid-cap, small-cap)

- Different geographies (domestic, international developed, emerging markets)

Within fixed income: varying maturities, credit quality, and issuer types. Beyond traditional assets, REITs, commodity exposure, and dividend-focused funds can provide inflation hedging that pure stock/bond portfolios often lack.

Step 4: Rebalance Regularly

Market performance causes portfolio drift. A strong equity run can leave a retiree significantly overexposed to stock risk without any active decision being made. A common industry guideline is threshold-based rebalancing — reviewing the portfolio when any asset class drifts 5 percentage points or more from its target allocation.

Most advisors also recommend a calendar-based review at minimum annually, or whenever financial circumstances change materially — a new income source, a health change, or a major market move.

Step 5: Work With a Comprehensive Financial Planner

Each of the steps above addresses one dimension of a retirement portfolio. Coordinating all of them — alongside taxes, Social Security, and estate goals — is where asset management ends and comprehensive financial planning begins.

A comprehensive financial planner — like the CFP®- and CFA®-certified team at Endeavor Financial Group — integrates portfolio strategy into your complete financial picture. The firm follows a five-step structured process: discovery, analysis, strategy development, implementation, and ongoing monitoring that adjusts as your life changes.

The practical difference: a comprehensive plan integrates your diversification strategy with:

- Tax-efficient withdrawal sequencing — which accounts to draw from first to minimize lifetime tax burden

- Social Security timing optimization — coordinating claiming strategies with portfolio income

- Estate planning alignment — ensuring your investment structure supports your legacy goals

- RMD planning — structuring the portfolio so Required Minimum Distributions don't create unexpected tax exposure

Because Endeavor Financial Group operates as a fee-only fiduciary — compensated directly by clients, not through commissions — every recommendation is based on what serves the client's situation, not what generates advisor income.

Conclusion

A well-diversified retirement portfolio is built for endurance — supporting your lifestyle through market cycles, health changes, and two or three decades of spending without forcing reactive decisions when conditions get difficult.

The best time to build or refine a diversified retirement strategy is before a market event makes the decision urgent. If you're approaching retirement and want to assess whether your current portfolio is built for the drawdown phase, a discovery meeting with Endeavor Financial Group's advisors can clarify where your portfolio stands and what adjustments — if any — make sense before the transition begins.

Frequently Asked Questions

What is the best investment strategy for a retiree?

There's no single right answer — it depends on your income needs, risk tolerance, health, and time horizon. Most advisors recommend a diversified mix of income-producing and growth-oriented assets, rebalanced regularly and adjusted over time to keep pace with inflation without taking on more volatility than you can sustain.

What did Warren Buffett say about diversification?

In his 1996 letter to Berkshire Hathaway shareholders, Buffett wrote: "Wide diversification is only required when investors do not understand what they are doing." That quote applies to investors who can deeply analyze individual businesses — which most retirees cannot and should not try to do. For individual investors managing retirement income, broad diversification remains the most practical risk management approach available.

What is the $1,000 a month rule for retirees?

It's a simplified rule of thumb suggesting you need roughly $240,000 in savings for every $1,000 per month in desired retirement income, based on a 5% annual withdrawal rate. It's a starting-point estimate, not a professional standard — actual needs vary by lifestyle, inflation assumptions, and portfolio performance. A diversified portfolio helps sustain withdrawals at this level across a multi-decade retirement.

How often should I rebalance my retirement portfolio?

Most financial advisors recommend reviewing your portfolio at least annually and rebalancing when any asset class drifts more than 5 percentage points from its target allocation. You should also review after significant life changes — a health event, new income source, or major shift in spending needs.

Can you have too much diversification in a retirement portfolio?

Yes. Holding too many funds with overlapping holdings adds fees and complexity without meaningfully reducing risk. Over-diversification dilutes your best positions without improving your correlation profile. True diversification is about holding assets that behave differently from each other — not simply owning more of everything.

How does diversification change as you approach retirement?

As retirement approaches, most investors gradually shift from growth-heavy allocations toward income-and-stability-focused ones — increasing exposure to bonds, dividend-paying stocks, and lower-volatility assets. The shift doesn't mean eliminating equities entirely; growth exposure remains necessary to fight inflation across a 20–30 year retirement.