Maximizing Your Nest Egg: A Guide to Equity Compensation and Retirement Planning

If you're an executive or long-term employee, your company stock isn't just a number on a statement—it's a significant part of your net worth. So, how do you turn this "paper wealth" into a secure retirement? It's a common challenge. You've worked hard to accumulate significant equity, but the path from owning shares to funding your lifestyle for the next 30 years isn't always clear.

This article provides a framework for integrating your equity compensation into a cohesive retirement plan. We'll break down the different types of equity, outline strategies based on your retirement timeline, and highlight the critical risks you need to manage. The goal is to give you the clarity needed to make confident decisions about your financial future.

TL;DR: Key Equity Compensation Strategies

- Know Your Equity: Understand the unique tax rules for RSUs, stock options, and ESPPs.

- Diversify Systematically: Create a plan to regularly sell company stock and reinvest in a balanced portfolio.

- Align Strategy to Timeline: Shift from growth to preservation and de-risk your portfolio as retirement nears.

- Plan for Taxes: Use a multi-year strategy to manage the tax impact of each equity transaction.

Understanding the Building Blocks: Common Types of Equity Compensation

Equity compensation is a powerful wealth-building tool, but it’s fundamentally different from your salary or 401(k). It requires a dedicated strategy to manage its unique opportunities and risks. Let's look at the most common forms.

Restricted Stock Units (RSUs)

RSUs are grants of company shares that you receive after a specific period or milestone, known as a vesting schedule. Once your RSUs vest, they are yours to keep. The total value of the shares at the time of vesting is taxed as ordinary income, just like your regular paycheck.

Stock Options (NQSOs and ISOs)

Stock options give you the right, but not the obligation, to buy company stock at a predetermined "strike price." The value comes from the difference between your strike price and the stock's current market price.

There are two main types of stock options, each with different tax implications.

Non-Qualified Stock Options (NQSOs): When you exercise these, the difference between the strike price and the market price is taxed as ordinary income.

Incentive Stock Options (ISOs): These can offer more favorable tax treatment. If you hold the shares for at least one year after exercising and two years after the grant date, the gain can be taxed at lower long-term capital gains rates.

However, be aware that exercising and holding ISOs can trigger the Alternative Minimum Tax (AMT), which requires careful planning.

Employee Stock Purchase Plans (ESPPs)

An ESPP is a company benefit that allows you to buy company stock, often at a discount, through convenient payroll deductions. These plans can be a great way to build ownership over time. If the plan is "qualified," you may receive favorable tax treatment if you hold the shares long enough after purchase.

The Foundation: Integrating Equity into Your Overall Retirement Plan

Your equity compensation shouldn't be managed in a silo. It needs to be a core component of your holistic financial plan, integrated with your other assets.

The first step is to quantify your retirement goals. Calculate the annual income you'll need to live comfortably, then determine the gap your equity compensation must fill. This exercise clarifies how your company stock fits alongside other assets, such as:

- 401(k)s and other employer-sponsored plans

- Traditional and Roth IRAs

- Social Security benefits

- Other personal savings and investments

Once you understand the numbers, the next step is to create a diversification plan. This involves systematically converting a concentrated position in company stock into a balanced portfolio that aligns with your risk tolerance.

A disciplined diversification strategy doesn't mean selling everything at once. Instead, it’s a multi-year plan designed to reduce your reliance on a single company's success over time.

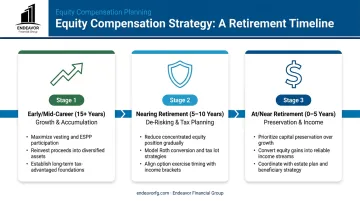

Strategic Planning by Retirement Stage

The right strategy for your equity depends heavily on your timeline. The closer you are to retirement, the more your focus should shift from aggressive growth to wealth preservation.

Early to Mid-Career (15+ Years from Retirement)

With time on your side, the focus is on growth and accumulation.

- Participate Fully: Take full advantage of programs like ESPPs, especially if there's a discount or company match.

- Learn the Mechanics: Use this time to understand the vesting schedules and tax implications of your grants.

- Adopt a "Sell-to-Diversify" Plan: Automatically sell a percentage (e.g., 25-50%) of your RSUs as they vest. Reinvest the proceeds into a diversified index fund or ETF to reduce concentration risk while still holding some shares for potential upside.

Nearing Retirement (5-10 Years Out)

Now, the priority shifts to de-risking and locking in your gains. Your retirement plan is becoming less theoretical and more concrete, so you need to reduce your dependency on a single stock's performance.

This is the time to create a multi-year tax plan. By strategically exercising options or selling shares over several years, you can avoid a massive income spike that pushes you into a much higher tax bracket in a single year.

It's also crucial to stress-test your plan. Model different scenarios to see if your retirement is still viable if your company stock drops by 20% or 30%. This analysis helps you determine a "core" amount of stock you're comfortable holding versus an amount that must be sold to secure your future.

At or Near Retirement (0-5 Years)

At this stage, it's all about wealth preservation and generating reliable income.

- Know the Rules: Understand your company's policies for equity after you leave. Many stock options have a limited post-termination exercise period, often just 90 days, after which they expire worthless.

- Create a Liquidity Calendar: Map out exactly when you can sell shares to generate cash for living expenses during your first few years of retirement.

- Coordinate Withdrawals: This calendar should be integrated with your other income sources. Plan how your stock sales will work alongside your 401(k) withdrawals and when you plan to start taking Social Security to create a smooth, tax-efficient income stream.

Navigating the Pitfalls: Key Risks and How to Mitigate Them

Building wealth with equity is only half the battle. Protecting it requires a strong defense. Here are the three biggest risks to manage.

Over-Concentration Risk

This is the danger of having too much of your net worth tied to a single company's stock. If the company hits a rough patch, your retirement savings could be decimated. Financial planners generally advise against letting any single stock make up more than 10% to 20% of your investment portfolio, a guideline supported by J.P. Morgan.

Mitigation Strategies:

- Systematic Selling: Implement a disciplined, automatic plan to sell shares on a set schedule (e.g., quarterly).

- Gifting: Donate appreciated shares to a charity or a Donor-Advised Fund to get a tax deduction while reducing your position.

- Fund Major Purchases: Use company stock to pay for a large expense like a home renovation or a child's wedding instead of depleting your cash reserves.

Market Volatility

A single stock is far more volatile than a diversified index. For example, in 2022, Meta's stock fell by over 64%, while the S&P 500 fell by a more modest 18%.

An undiversified portfolio heavily weighted toward one stock can experience swings that could derail a retirement plan right when you need the money most.

Tax Complexity

Mistakes in tax planning can erode a huge portion of your equity wealth. Each action you take—or don't take—has a tax consequence.

- RSU Vesting: Triggers ordinary income tax.

- NQSO Exercise: Triggers ordinary income tax.

- ISO Exercise: Can trigger the Alternative Minimum Tax (AMT).

It's critical to plan for the tax bill. This means setting aside enough cash from sales to cover the taxes or using a "sell-to-cover" transaction where a portion of your shares are automatically sold to handle the withholding.

Surprises are the last thing you want at tax time, and navigating these rules is where professional guidance becomes invaluable.

Why Professional Guidance is Crucial for Equity Compensation Planning

Managing significant equity compensation is one of the most complex areas of personal finance. The stakes are high, and the rules are complicated. The risks of over-concentration, volatility, and tax missteps are too significant to navigate with guesswork.

A professional financial advisor helps by:

- Building sophisticated models to project your retirement income

- Creating a multi-year tax strategy to minimize your liability

- Providing the unbiased discipline needed to stick to a diversification plan

At Endeavor Financial Group, we operate as fee-only fiduciaries, which means we are legally obligated to act in your best interest. Our advice isn't influenced by commissions, ensuring our recommendations are based solely on what's best for your financial plan.

Our structured, five-step process—from discovery to ongoing monitoring—provides the clear roadmap needed to turn your hard-earned company stock into lasting financial freedom and peace of mind.

Frequently Asked Questions

What is an equity compensation plan?

It's a non-cash payment method companies use to give employees an ownership stake. Common forms include stock options, restricted stock units (RSUs), and employee stock purchase plans (ESPPs).

Is equity compensation worth it?

It can be an extremely valuable tool for building wealth. However, it comes with risks like market volatility and over-concentration that require a thoughtful and disciplined management strategy.

What happens to my vested stock options when I retire?

When you leave a company, a post-termination exercise period begins. This window is often 90 days, and you must exercise your vested options before it closes, or you will forfeit them.

How much of my company stock is too much for my retirement portfolio?

A general guideline is to keep no more than 10-20% of your total investment portfolio in a single stock. This helps mitigate the risk of a single company's poor performance derailing your entire retirement plan.

Should I sell my company stock as soon as it vests?

While many planners suggest selling immediately to diversify, the best strategy is unique to you. A financial advisor can help create a plan based on your tax situation, risk tolerance, and long-term retirement goals.