This guide is for any employee, executive, or business owner who receives equity compensation and needs a clear roadmap. We'll break down how RSUs and different stock options are taxed, outline key planning strategies, and highlight common mistakes to avoid, helping you turn your equity into a cornerstone of your financial future.

Key Takeaways

- RSUs are taxed as ordinary income when they vest, based on the shares' fair market value on the vesting date.

- Non-qualified Stock Options (NSOs) are taxed as ordinary income on the "bargain element" (the spread between market price and strike price) when you exercise them.

- Incentive Stock Options (ISOs) can trigger the Alternative Minimum Tax (AMT) at exercise and may qualify for favorable long-term capital gains rates if you meet specific holding periods.

- Proactive planning, like timing your exercises and sales or making estimated tax payments, is essential to prevent a large, unexpected tax bill.

Understanding the Basics: Stock Options vs. RSUs

Equity compensation is a form of non-cash pay that gives you an ownership stake in the company you work for. While there are many types, most fall into two main categories: RSUs and stock options.

Restricted Stock Units (RSUs)

RSUs are a straightforward promise from your employer to give you a specific number of company shares on a future date, known as the vesting date. You don't pay anything for these shares. Once they vest, they are yours. Because you receive the shares outright, they have value even if the stock price doesn't increase.

Stock Options

Unlike RSUs, stock options give you the right—but not the obligation—to purchase a set number of company shares at a predetermined strike price (or exercise price). Options are only valuable if the stock's market price rises above your strike price. The profit potential is the "spread"—the difference between the higher market value and your lower purchase price.

Why Proactive Tax Planning for Equity is Non-Negotiable

Ignoring the tax implications of your equity is a recipe for financial stress. Because this compensation often arrives in large, lump-sum values, it can create significant and often unexpected tax liabilities.

Failing to plan exposes you to several significant financial risks:

- A Major Tax Shortfall: Companies often withhold at the default federal supplemental rate of 22%. However, a large equity event can easily push your marginal rate to 24%, 32%, or higher, leaving you with a surprise tax bill.

- Missed Savings Opportunities: Without a strategy, you could miss the chance to qualify for more favorable long-term capital gains tax rates.

- Costly Tax Triggers: A poorly timed decision can trigger complex and expensive taxes, like the Alternative Minimum Tax (AMT), that could have been avoided.

How Your Equity is Taxed: A Breakdown for Stock Options & RSUs

The lifecycle of equity compensation has four key events: Grant, Vest, Exercise, and Sale. The tax implications are different for each type of equity at each stage.

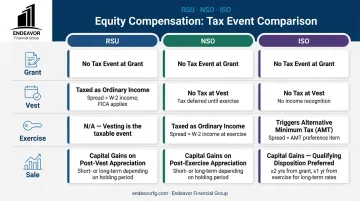

Tax Treatment of RSUs

- Grant Date: No tax event. This is simply when the company promises you the future shares.

- Vesting Date: This is the main taxable event. The total market value of your vested shares is taxed as ordinary income. This includes federal, state, Social Security, and Medicare taxes, just like your regular salary.

- Example: If 100 RSUs vest when the stock price is $50, you have $5,000 of ordinary income to report for that year.

- Sale Date: After vesting, the shares are yours. If you sell them immediately, there's typically no additional gain or loss. If you hold them, any appreciation in value from the vesting date to the sale date is taxed as a capital gain.

Tax Treatment of Non-qualified Stock Options (NSOs)

- Grant & Vesting Dates: No tax event. You don't owe tax just for receiving or becoming eligible to exercise your options.

- Exercise Date: This is the key taxable event. The "bargain element"—the difference between the market value and your strike price—is taxed as ordinary income.

- Example: You exercise 100 NSOs at a strike price of $10 when the market price is $50. The bargain element is ($50 - $10) x 100 = $4,000. This $4,000 is taxed as ordinary income.

- Sale Date: Your cost basis for the shares is the market value on the day you exercised. Any further gain is treated as a capital gain.

Tax Treatment of Incentive Stock Options (ISOs)

ISOs are more complex but offer significant tax advantages if handled correctly.

- Grant & Vesting Dates: No tax event.

- Exercise Date: For regular income tax, nothing is due. However, the bargain element is an adjustment item for the Alternative Minimum Tax (AMT), a separate tax system that runs parallel to the regular one.

A large ISO exercise can trigger a substantial AMT liability, even though you haven't sold any shares to cover the bill. This is a critical planning point.

- Sale Date: This is where the planning pays off.

- Qualifying Disposition: If you sell the shares at least 2 years after the grant date AND 1 year after the exercise date, the entire gain (from your strike price to the sale price) is taxed as a long-term capital gain. This is the ideal outcome.

- Disqualifying Disposition: If you don't meet both holding periods, the bargain element is taxed as ordinary income, and only the remaining gain is treated as a capital gain.

Key Tax Planning Strategies for Your Equity Compensation

The right strategy depends on your cash flow, risk tolerance, and financial goals. While there's no one-size-fits-all answer, several effective approaches can help manage your tax liability.

Managing Your Tax Bill at Vesting/Exercise

When your RSUs vest or you exercise NSOs, you have a tax bill to pay. You have two main options for covering it:

- Sell-to-Cover: Your broker automatically sells just enough shares to cover the estimated tax withholding. This is the most common method as it requires no cash upfront.

- Pay with Cash: You pay the taxes out-of-pocket, allowing you to keep all your vested shares. This makes sense if you are bullish on the company's future and have the available cash.

Regardless of which you choose, it's crucial to check your withholding rate. If it's only 22%, you may need to make quarterly estimated tax payments to the IRS to avoid underpayment penalties.

While managing taxes for RSUs and NSOs is straightforward, Incentive Stock Options (ISOs) introduce a major complication: the Alternative Minimum Tax (AMT).

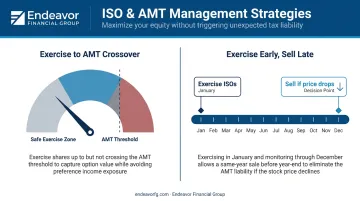

Strategies for ISOs and the AMT

The AMT is the biggest trap for ISO holders. To manage it, you can:

- Exercise up to the AMT Crossover: Work with a financial professional to model your taxes and determine how many ISOs you can exercise in a single year without triggering the AMT. This allows you to start the one-year holding period for long-term capital gains without an immediate tax hit.

- Exercise Early in the Year: If you exercise your ISOs in January, you have the rest of the year to see how the stock performs. If the AMT liability looks too large or the stock price drops, you can sell the shares before December 31. This creates a disqualifying disposition, which pushes the tax event into the regular income system and eliminates the AMT problem for that exercise.

Once you've acquired the shares and managed the initial tax event, the next decision is when to sell.

Planning for Long-Term Capital Gains

For both vested RSUs and exercised ISOs, holding the shares for more than a year qualifies you for lower long-term capital gains tax rates. This can result in significant savings compared to short-term rates, which are the same as ordinary income.

However, this tax benefit comes with a risk. Holding onto a large amount of company stock creates a concentrated position, exposing your net worth to the performance of a single company.

A common guideline suggests a single stock should not account for more than 10% of your total portfolio value. Balancing tax optimization with portfolio diversification is a critical part of any sound equity compensation strategy.

Common (and Costly) Tax Mistakes to Avoid

A small oversight can lead to a huge tax bill. Here are three of the most common mistakes to watch out for.

- Ignoring the Alternative Minimum Tax (AMT) impact on Incentive Stock Options (ISOs). Exercising many ISOs at once can trigger a massive, unexpected tax bill due in April, even if you haven't sold any shares.

- Failing to correct your RSU cost basis. The value of your RSUs at vesting becomes your cost basis, but your broker's 1099-B form may incorrectly list it as $0. Not fixing this on your tax return can lead to double taxation on the same income.

- Prioritizing tax benefits over concentration risk. Don't let the "tax tail wag the dog" by holding a massive stock position just for a better tax rate. A single bad earnings report could wipe out years of gains, far outweighing any tax savings.

Conclusion: Build Your Personalized Equity Compensation Strategy

RSUs, NSOs, and ISOs each have unique tax rules that create both challenges and opportunities. Understanding the timing of taxable events and the differences between ordinary income and capital gains is the first step toward building an effective plan. A proactive strategy can save you thousands of dollars in taxes and help you integrate your equity compensation into a broader wealth-building plan.

Navigating these complexities requires a personalized approach. This involves modeling tax scenarios, deciding when to exercise and sell, and balancing tax efficiency with sound investment diversification.

A financial advisor can help you create a clear roadmap for your equity. As fee-only fiduciaries, the team at Endeavor Financial Group specializes in building comprehensive strategies for executives and business owners to turn complex compensation into long-term wealth.

Frequently Asked Questions

Are RSUs taxable?

Yes, the full market value of RSUs is taxed as ordinary income when they vest. This includes federal, state, and payroll taxes (Social Security and Medicare).

How can I avoid being taxed twice on my RSUs?

To avoid double taxation, you must correctly report your cost basis when you sell your RSU shares. Your cost basis is the market value of the shares on the day they vested, since that amount was already taxed as income.

How can I avoid capital gains tax on RSUs?

You can't completely avoid capital gains tax if the stock appreciates after vesting, but you can manage it. Holding the shares for more than one year after they vest allows any gains to be taxed at the more favorable long-term capital gains rate.

What is the main tax difference between ISOs and NSOs?

The primary difference is at exercise. NSOs trigger ordinary income tax on the "bargain element" immediately. ISOs do not trigger regular income tax at exercise but can trigger the Alternative Minimum Tax (AMT).

What is the Alternative Minimum Tax (AMT) and how does it relate to stock options?

The AMT is a separate tax system to ensure high-income individuals pay a minimum tax amount. Exercising and holding Incentive Stock Options (ISOs) can trigger it because the "paper gain" is treated as income under AMT rules.