For many retirees, this new season brings a wave of legitimate concerns. A recent AARP survey found that 61% of U.S. adults over 50 worry about outliving their savings. Add in the anxieties of market volatility and rising inflation, and it's easy to feel overwhelmed.

The key is to replace that anxiety with a clear, disciplined strategy. These five tips provide a framework to help you build a resilient retirement portfolio that delivers both the income you need and the peace of mind you deserve.

TL;DR: 5 Keys to Retirement Portfolio Success

- Shift your mindset from growing wealth to distributing it wisely.

- Use a "bucket strategy" to align assets with short, mid, and long-term needs.

- Create a tax-efficient withdrawal plan to keep more of your money.

- Actively manage major risks like inflation and market downturns early in retirement.

- Review regularly and work with a professional to stay on course.

Tip 1: Reassess Your Financial Landscape: From Accumulation to Distribution

The single biggest mental shift in retirement is moving from the accumulation phase to the distribution phase. For decades, your goal was to grow your nest egg. Now, your goal is to make that nest egg last for the rest of your life, which could be 30 years or more.

Define Your Retirement Income Needs

Before you can structure your portfolio, you need to know exactly what you'll be asking it to do. Start by calculating your annual expenses.

- List Essential Expenses: Tally up the costs you can't avoid, like housing (mortgage/rent, property taxes, utilities), healthcare (premiums, co-pays, prescriptions), food, and transportation.

- List Discretionary Expenses: Account for the things that make retirement enjoyable, such as travel, hobbies, dining out, and entertainment.

- Identify the "Income Gap": Add up your guaranteed income sources, like Social Security and any pensions. Subtract this total from your annual expenses. The remaining amount is the income gap—the annual income your portfolio must generate to cover your lifestyle.

Re-evaluate Your Time Horizon and Risk Tolerance

While you're no longer 30 years from retirement, a 65-year-old today still has a life expectancy of nearly 20 years on average, meaning many will live much longer. Your portfolio still needs to grow to support you through a long-term investment period.

This is where you must distinguish between your willingness to take risks and your ability to take them.

- Risk tolerance is your emotional comfort with market swings—how well you sleep at night when the market is down.

- Risk capacity is your financial ability to withstand losses without jeopardizing your essential income needs.

Someone who was comfortable with a 70% stock portfolio while working might now prefer a 50% or 60% allocation. The key is finding a balance where you can still achieve the growth needed to beat inflation without taking on undue stress or risk.

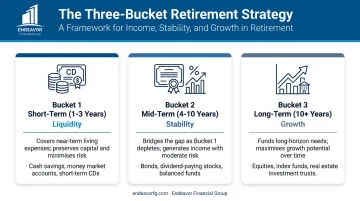

Tip 2: Master Your Asset Allocation with the "Bucket" Strategy

One of the most effective ways to structure a retirement portfolio is the "bucket" strategy. This approach divides your assets into three distinct pools, or buckets, each with a specific purpose and time horizon. The framework ensures you have cash for today, stability for tomorrow, and growth for the future.

Understanding the Three-Bucket Approach

Bucket 1: Short-Term (1-3 Years of Expenses)

This is your liquidity bucket, designed to cover your immediate living expenses without forcing you to sell other assets during a market downturn. It’s your financial safety net.

- Purpose: Cash flow for near-term needs.

- What it holds: High-yield savings accounts, money market funds, short-term CDs, and Treasury bills.

Bucket 2: Mid-Term (4-10 Years of Expenses)

This is your income and stability bucket. Its primary job is to generate steady returns with moderate risk, providing the funds to refill Bucket 1 as you spend it down. It acts as a buffer between your cash and your long-term growth investments.

- Purpose: Capital preservation and reliable income generation.

- What it holds: High-quality corporate and municipal bonds, bond ladders, dividend-paying stocks, and low-volatility equity funds.

Bucket 3: Long-Term (10+ Years)

This is your growth engine. Assets in this bucket should be left largely untouched for a decade or more, giving them time to ride out market cycles and grow. This bucket is essential for outpacing inflation and ensuring your portfolio lasts for your entire retirement.

- Purpose: Long-term growth to fight inflation and prevent you from outliving your money.

- What it holds: Diversified stock market ETFs (U.S. and international), growth-oriented mutual funds, and real estate investment trusts (REITs).

By segmenting your portfolio this way, you create a clear structure that helps you face market volatility with confidence, knowing your immediate needs are covered.

Tip 3: Create a Disciplined and Tax-Efficient Withdrawal Plan

How you take money out of your retirement accounts is just as important as how you put it in. A smart withdrawal strategy can add years to your portfolio's life and save you thousands in taxes.

Choosing a Sustainable Withdrawal Rate

The "4% Rule" has long been a popular benchmark. Originating from a 1994 study by William Bengen, it suggested that withdrawing 4% of your portfolio in the first year of retirement, and adjusting that amount for inflation each year after, had a high probability of success.

However, today's market is different. With lower expected returns, many experts suggest a more conservative starting point. For 2024, Morningstar's research suggests a starting safe withdrawal rate of 3.7%.

A more flexible "dynamic withdrawal" strategy is often a better approach. This involves adjusting your withdrawal percentage based on market performance. For example:

- After a year of strong returns, you might take a slightly larger withdrawal for a discretionary expense.

- After a down year, you might tighten your belt and withdraw a smaller percentage to give your portfolio time to recover.

A dynamic strategy helps protect your portfolio during downturns. But the withdrawal rate is only half the equation; the other half is which account you pull from. This decision has major tax implications.

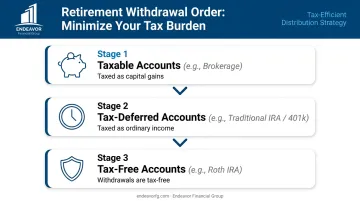

Tapping Your Accounts in the Right Order

To maximize your portfolio's longevity, you need to minimize your tax bill. The general hierarchy for tax-efficient withdrawals is to pull from accounts in this order:

- Taxable Accounts: This includes standard brokerage accounts. You'll owe capital gains tax on any appreciation, but these accounts have the most flexibility and don't come with the same restrictions as retirement accounts.

- Tax-Deferred Accounts: This includes Traditional 401(k)s and Traditional IRAs. Every dollar you withdraw from these is taxed as ordinary income. It's generally wise to let this money grow tax-deferred for as long as possible before Required Minimum Distributions (RMDs) kick in.

- Tax-Free Accounts: This includes Roth IRAs and Roth 401(k)s. Qualified withdrawals are completely tax-free. By saving these accounts for last, you allow them to grow for the longest possible time without any tax drag.

This order provides a strong foundation, but the right strategy often depends on your specific tax situation and income needs. Crafting a personalized plan helps ensure you minimize taxes and make your savings last.

Tip 4: Proactively Manage Retirement's Biggest Risks

Two of the biggest threats to a retirement portfolio are poor market timing and the steady erosion of inflation. A well-designed plan actively defends against both.

Guarding Against Sequence of Returns Risk

Sequence of returns risk is the danger of experiencing a major market downturn in the first few years of retirement. Withdrawing funds from a portfolio that has just suffered a significant loss can permanently cripple its ability to recover and last for the long term.

This is where the bucket strategy proves its worth. Bucket 1 is your primary defense, holding 1-3 years of living expenses in cash and stable assets. This allows you to pay bills without being forced to sell stocks (Bucket 3) when they are down, giving your growth assets time to rebound.

Countering the Effects of Inflation

Inflation is the steady force that reduces your purchasing power over time. Even a modest 3% inflation rate can have a dramatic impact over a 20- or 30-year retirement.

For example, at that rate, $1 million today would have the purchasing power of only about $477,000 in 25 years.

Your best long-term tool for combating inflation is your growth allocation. Bucket 3, with its diversified holdings in stocks and real estate, is designed to generate returns that outpace the rising cost of living.

Being too conservative and avoiding growth assets is one of the biggest risks a long-term retiree can take.

Tip 5: Stay on Course with Regular Reviews and Professional Guidance

A retirement portfolio plan is not a "set it and forget it" document. Your life, the market, and your goals will change. A disciplined review process is essential to staying on track. We recommend a quick check-in quarterly and a comprehensive review at least once a year.

During these reviews, you should ask:

- Is my asset allocation still aligned with my risk tolerance?

- Do my buckets need to be rebalanced or refilled?

- Is my withdrawal rate still sustainable?

- Have any life events (health changes, family needs) changed my financial picture?

Navigating complexities like dynamic withdrawals, tax-efficient rebalancing, and risk management is where professional guidance becomes invaluable.

At Endeavor Financial Group, our consultative approach uses a structured five-step process—from discovery and analysis to implementation and ongoing monitoring. We work with you to build a clear roadmap, ensuring your strategy remains aligned with your goals and provides the financial confidence you need to enjoy retirement.

If you're ready to create a clear, resilient plan for your retirement income, schedule a consultation with our team today.

Frequently Asked Questions

How do I manage a portfolio in retirement?

The focus shifts from growth to capital preservation and income. Key strategies include using a bucket system for your assets, implementing a tax-efficient withdrawal plan, and regularly reviewing your portfolio with an advisor.

What is a safe withdrawal rate in retirement?

The traditional 4% rule is a common starting point, but many planners now consider 3-5% to be more sustainable. Dynamic strategies that adjust withdrawals based on market performance are also popular for preserving capital.

Should I still own stocks in retirement?

Yes, owning stocks is crucial for combating inflation and ensuring your money lasts. Your portfolio should balance these growth assets with less volatile investments, like bonds, to help manage overall risk.

How often should I review my retirement portfolio?

A brief quarterly check-in is a good habit, but a comprehensive review with a financial advisor should occur at least annually. You should also review your portfolio after any major life event, like a change in health or family needs.

How do I protect my portfolio from inflation in retirement?

The best long-term protection is a diversified allocation to growth assets. Stocks and real estate (like REITs) have historically generated returns that outpace inflation, preserving your purchasing power over time.

What is the role of bonds in a retirement portfolio?

Bonds provide stability and predictable income, acting as a counterbalance to stock market volatility. This helps preserve your capital while generating steady cash flow to cover living expenses in retirement.