Wealth preservation isn't just about playing defense; it's a proactive discipline for safeguarding your financial future. It requires a clear understanding of the threats you face and a coordinated plan to address them. This article provides a roadmap, covering foundational strategies like insurance, advanced tools like trusts, and how to integrate everything into a comprehensive plan that protects what you’ve built.

TL;DR: Key Wealth Preservation Takeaways

- Preservation vs. Protection: Preservation guards against market risks (inflation, volatility), while protection shields assets from legal threats (lawsuits, creditors).

- Identify Your Risks: Common threats include lawsuits, divorce, market downturns, inflation, and poorly planned taxes.

- Build a Strong Foundation: Start with essential, non-negotiable steps like maximizing liability insurance, securing retirement accounts, and diversifying investments.

- Use Advanced Tools: Fortify your assets with legal structures like LLCs and irrevocable trusts to create powerful liability shields.

- Proactive Planning is Crucial: A coordinated plan developed with a professional before a threat arises is the only way to ensure your strategies are effective.

Wealth Preservation vs. Wealth Protection: A Critical Distinction

While often used interchangeably, "wealth preservation" and "wealth protection" address different risks. Understanding this distinction is the first step toward building a holistic strategy that covers all your bases.

Wealth Preservation: Defending Against the Storm

Think of wealth preservation as protecting your ship from a storm. The goal is to safeguard your assets from market volatility, inflation, and economic downturns. It’s about maintaining the purchasing power of your money, ensuring that the wealth you have today can provide for your lifestyle tomorrow.

Inflation is a silent but powerful threat. Data from the Federal Reserve Bank of Minneapolis highlights this erosion: what cost $1 in 1913 would cost over $33 today. Preservation strategies like diversification are designed to help your assets weather these economic storms and maintain their real value over time.

Wealth Protection: Guarding Against Pirates

Wealth protection, also known as asset protection, is about protecting your ship from pirates. These pirates are external, third-party claims that can arise from lawsuits, creditors, or divorce settlements. The focus here is on structuring the ownership of your assets in a way that makes them difficult for unintended parties to reach. This involves legal tools like trusts and limited liability companies (LLCs) to build a fortress around your wealth.

Identifying the Primary Threats to Your Wealth

Identifying the Primary Threats to Your Wealth

An effective wealth preservation plan begins with a clear assessment of the risks. For high-net-worth individuals, pre-retirees, and business owners, threats can come from multiple directions.

Legal and Personal Risks

We live in a litigious society. A simple car accident, an injury on your property, or a liability claim against your business can quickly escalate into a lawsuit that puts your personal assets at risk. According to the Insurance Information Institute, the average auto liability claim for bodily injury was $28,278 in 2024.

However, severe accidents can result in judgments far exceeding standard insurance limits. Divorce is another significant personal risk that can divide a lifetime of accumulated assets without proper planning.

Market and Economic Risks

The markets that help build wealth also pose a constant threat to it.

- Inflation: As mentioned, inflation slowly erodes the value of your cash and fixed-income investments.

- Market Volatility: Sudden stock market downturns can significantly reduce the value of your portfolio, especially if you’re nearing or in retirement and don't have time to wait for a recovery.

- Interest Rate Changes: Fluctuating interest rates impact bond values and the cost of borrowing, affecting everything from your investment returns to your business's bottom line.

Tax-Related Risks

Without careful planning, taxes can take a substantial bite out of your wealth, particularly when passing assets to the next generation. The federal estate tax exemption is $15 million per person for 2026, but assets above that amount can be taxed at rates as high as 40%.

Capital gains and income taxes can also significantly diminish your assets if you don't have a tax-efficient strategy in place.

Foundational Strategies: Your First Line of Defense

Before diving into complex legal structures, every asset owner should have these non-negotiable protections in place. Think of them as the essential sea walls that provide your first and most cost-effective layer of defense.

Maximize Your Liability Insurance

Insurance is the simplest and most efficient way to transfer risk. For a relatively small premium, you can protect yourself from potentially catastrophic financial losses.

- Review primary policies: Ensure your homeowners and auto liability limits are high enough to protect your total net worth, not just meet state minimums.

- Add umbrella insurance: This cost-effective policy provides extra liability coverage (typically $1 million or more) that activates after your primary policies are exhausted.

- Match coverage to your net worth: A common guideline is to secure an umbrella policy with a limit equal to or greater than your net worth.

Secure Your Retirement Accounts

Certain retirement accounts come with powerful, built-in creditor protection.

- Prioritize ERISA-qualified plans like 401(k)s, which generally receive unlimited protection from creditors under federal law.

- Understand state-specific laws for IRAs (Traditional, Roth, SEP, SIMPLE), as their protection from creditors can vary from robust to minimal.

- Confirm your specific protections, as the rules can be complex and depend on your state of residence.

Diversify Your Investment Portfolio

Diversification is the bedrock of wealth preservation. The goal isn't just to maximize growth but to minimize the impact of a downturn in any single asset class. By spreading investments across different stocks, bonds, real estate, geographies, and sectors, you reduce the risk of a single event wiping out a large portion of your portfolio.

Historical data from Vanguard shows just how effective this can be. A well-diversified portfolio has historically weathered market downturns better than an all-stock portfolio, reducing the severity of losses.

Portfolio Performance, 1926–2024

| Allocation (Stocks/Bonds) | Average Annual Return | Worst Year | Number of Loss Years (out of 99) |

|---|---|---|---|

| 100% / 0% | 10.2% | -43.1% | 25 |

| 60% / 40% | 8.7% | -26.6% | 22 |

| 40% / 60% | 7.6% | -18.4% | 20 |

Source: Vanguard model portfolio data

As the table shows, while adding bonds reduces the average return, it significantly softens the blow during the worst years and reduces the overall frequency of losses.

Advanced Strategies: Fortifying Your Legacy and Assets

Once your foundation is secure, the next step is to fortify your assets. These advanced strategies use legal structures to provide robust protection, separate personal and business liabilities, and give you greater control over how your assets are managed and distributed.

Utilize Legal Entities for Business and Real Estate Assets

If you own a business or rental properties, it's crucial to separate those liabilities from your personal assets. Placing these assets into a Limited Liability Company (LLC) creates a protective barrier.

Should a lawsuit arise from your business or a rental property, the claim is generally limited to the assets held within that specific LLC. This structure shields your personal home, savings, and investments from business-related claims.

Implement Strategic Estate Planning with Trusts

Trusts are powerful and flexible tools for both asset protection and legacy planning.

- Irrevocable Trusts: When you move assets into an irrevocable trust, you legally relinquish ownership and control. This removes the assets from your personal estate, which can offer significant protection from future creditors and potentially reduce estate taxes. This must be done proactively, long before any claim arises.

- Lifetime Trusts for Heirs: Instead of leaving an inheritance to your children outright, you can leave it in a lifetime trust. This protects the inheritance from a child's potential creditors, lawsuits, or a future divorce settlement, ensuring the assets remain in your family line as you intended.

Review and Optimize Asset Titling

How you own an asset—its "title"—has major legal consequences. For married couples, a form of ownership called Tenancy by the Entirety (TBE), available in states like Indiana, Florida, and Michigan, can provide powerful protection.

Assets titled as TBE are owned by the marital unit, not the individuals. This means a creditor of only one spouse generally cannot seize the property to satisfy a debt.

Plan for Strategic Gifting

Gifting assets during your lifetime can be an effective way to reduce the size of your taxable estate and help your loved ones. The annual gift tax exclusion allows you to give up to a certain amount per person each year without filing a gift tax return ($18,000 in 2024). Over time, a strategic gifting plan can move significant wealth out of your estate and beyond the reach of potential personal creditors.

Building Your Comprehensive Wealth Preservation Plan

These strategies are not à la carte options to be picked at random. They are interlocking pieces of a puzzle that must be assembled into a single, coordinated plan tailored to your unique situation.

Most importantly, wealth protection planning must be done before a threat emerges. Waiting until you're facing a lawsuit or financial trouble is often too late. Courts can view last-minute asset transfers as fraudulent and unwind them, leaving your wealth exposed.

Creating a comprehensive plan requires a holistic approach that considers your financial goals, risk tolerance, and specific vulnerabilities. This is where working with a fiduciary financial planning firm like Endeavor Financial Group becomes critical.

As fiduciaries, we are legally obligated to act in your best interest. This ensures our advice is free from the conflicts of interest that can arise from commission-based product sales.

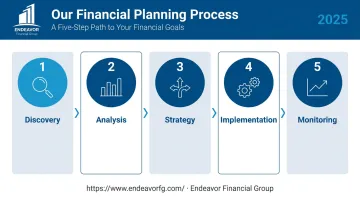

Our five-step process provides the structured framework needed to build and maintain your plan:

- Discovery: We start by identifying your goals, priorities, and concerns.

- Analysis: We analyze your complete financial picture to understand your risks and opportunities.

- Strategy: We design a personalized roadmap with short, intermediate, and long-term recommendations.

- Implementation: We help you put the plan into action, coordinating with your legal and tax legal and tax professionals to ensure every piece works together seamlessly.

- Monitoring: We conduct regular reviews to adapt your plan as your life and goals evolve.

Frequently Asked Questions

How do I protect my wealth in retirement?

Protecting wealth in retirement involves creating diversified income streams to avoid selling assets at the wrong time, planning for long-term care costs, and using trusts to ensure your legacy is passed on efficiently.

What is the difference between wealth preservation and wealth growth?

Wealth growth focuses on increasing your net worth, which often involves taking on higher levels of risk for potentially higher returns. Wealth preservation prioritizes protecting your existing principal from loss due to market, legal, or economic threats.

Can a revocable living trust protect my assets from a lawsuit?

Generally, no. Because you retain control over the assets in a revocable trust and can amend it at any time, creditors can typically reach them. Irrevocable trusts are the tool used for asset protection.

How much umbrella insurance coverage is typically recommended?

A common rule of thumb is to have umbrella coverage equal to your total net worth. However, a financial advisor can assess your specific risk factors to determine the most appropriate amount for your situation.

When is the right time to start wealth preservation planning?

Planning should begin as soon as you have significant assets to protect. Because the best strategies require proactive implementation, the ideal time to start is now—well before any potential liabilities arise.