Why Estate Planning Looks Different When You Own a Business

Your business is probably your most valuable asset. It's also the one most at risk during an ownership transition.

For most small business owners, the company represents the majority of personal net worth. Unlike a brokerage account or rental property, a business can lose value fast during an unplanned ownership transition, a probate delay, or the sudden loss of a key person. Yet according to a 2022 MassMutual study, only 51% of business owners had an estate plan, and just 8% had completed exit planning.

That gap has real consequences.

This article covers what every small business owner needs: the foundational legal documents, a succession plan that holds up under pressure, buy-sell agreements, liquidity strategies, and tax-smart transfer tools.

Key Takeaways

- Your business is likely your largest asset — your estate plan needs to reflect that

- Without a succession plan, expect probate delays, operational disruption, and possible forced sales

- Key planning tools include a revocable living trust, buy-sell agreement, key person insurance, and liquidity reserves

- A plan that separates your personal finances from your business transition often falls short of both goals

- Tax-advantaged transfer strategies lose effectiveness as your business grows, so timing matters more than most owners realize

The Unique Challenges Small Business Owners Face

Concentration Risk and the Planning Gap

Most business owners carry a significant portion of their net worth in a single illiquid asset. The SBA Office of Advocacy found that business equity represented 34% of U.S. household nonfinancial assets in 2019 — second only to primary residences. And Gallup reported in 2025 that roughly one-third of all business owners lack a formal long-term plan or are uncertain they have one.

That's a structural problem. A stock portfolio can be liquidated in days. A business cannot.

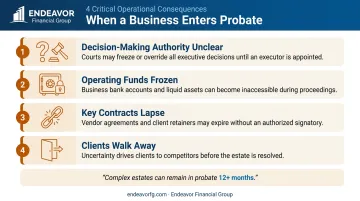

The Probate Problem for Business Assets

When a personal financial account passes through probate, it's a paperwork inconvenience. When a business does, it can be a crisis.

During probate, the operational impact is immediate:

- Decision-making authority becomes unclear

- Access to operating funds may be frozen

- Key contracts can lapse without an authorized signatory

- Clients may walk before the estate is settled

None of this is hypothetical. Complex estates involving business interests — particularly those requiring a federal estate tax return — can remain in probate for over a year.

Why Family Assumptions Are Dangerous

Many owners assume a spouse or child will step in and run things. That assumption needs to be tested early and put in writing, not discovered to be wrong during a crisis. PwC found that only 34% of family businesses have a formal, documented, and communicated succession plan, and less than half of family members even agree on the company's direction.

The Liquidity Mismatch

A business may be worth $2 million on paper but produce zero cash for the estate when it's needed most. Estate taxes, outstanding debt, and family income replacement all require actual money — and a business interest can't be split up and converted to cash overnight. Without advance planning, that gap often forces a distressed sale at a fraction of the business's real value.

The Foundational Documents Every Business Owner Needs

A complete estate plan for a business owner goes beyond a basic will. Here's what the foundation looks like:

Revocable Living Trust vs. Will

A last will and testament is a starting point, not a complete strategy. A revocable living trust offers three advantages a will cannot:

- Passes assets directly to beneficiaries without court involvement (avoiding probate)

- Lets a named successor trustee manage business assets immediately if you become incapacitated

- Keeps ownership details private — unlike a will, a trust never becomes a public record

The two documents aren't mutually exclusive. Most business owners use a "pour-over will" alongside the trust to catch any assets not transferred into it before death.

Durable Financial Power of Attorney

Without this document, no one can legally act on your behalf if you're incapacitated — not your spouse, not your business partner. That means no one can vote shares, execute contracts, or manage business accounts until a court appoints a guardian. The process takes time and money the business may not have.

Healthcare Directive and Healthcare POA

These documents address medical decisions, not financial ones. But for a sole proprietor, an extended hospitalization is functionally the same as a business crisis. These documents belong in every estate plan.

Buy-Sell Agreement (Preview)

For businesses with multiple owners, a buy-sell agreement governs what happens to each owner's share when someone exits — death, disability, divorce, or retirement. It works alongside the estate plan, not instead of it. This is covered in depth in the next section.

A Note on Coordination

Each of these documents must align with each other and with any existing shareholder agreements, operating agreements, or partnership agreements.

A conflict between a trust provision and a shareholder agreement can create exactly the kind of legal dispute you're trying to prevent — so review all documents together, not in isolation.

Building a Succession Plan That Actually Works

Identifying and Preparing Your Successor

There are three realistic successor paths:

| Path | Key Planning Requirements |

|---|---|

| Family member | Governance structures, gifting strategies, role clarity |

| Key employee | Buy-sell agreement, seller financing, leadership transition |

| Outside buyer | Business valuation, tax planning, deal structure |

The right path depends on your goals — but waiting too long to choose one is the most common mistake. A successor who hasn't been trained, given decision-making authority, or introduced to key clients cannot take over quickly. Start involving the right person in leadership gradually, not all at once when a crisis forces the decision.

Formalizing the Plan

Succession planning discussed verbally in a family meeting is a conversation, not a plan. To be enforceable, it must be documented through legally binding instruments:

- Trust provisions

- Buy-sell agreements

- Shareholder agreements

- Some combination of the above

Before any of that can happen, the business needs to be valued. Any ownership transfer — whether a sale, gift, or inheritance — requires knowing what the business is actually worth. The IRS has its own standards for this (rooted in Rev. Rul. 59-60, the benchmark for valuing closely held businesses), and a qualified business valuator familiar with your industry will produce a defensible number.

That's where coordinated planning matters. Endeavor Financial Group's five-step process — covering discovery, analysis, implementation, and ongoing monitoring — helps business owners move from recognizing the need for a plan to actually having one in place. The team works alongside estate attorneys, CPAs, and valuation professionals to ensure the succession strategy aligns with personal financial goals and adapts as the business and family situation evolve.

Buy-Sell Agreements: What You Need to Know

A buy-sell agreement is a legally binding contract that specifies what happens to each owner's share when someone exits — death, disability, divorce, retirement, or an involuntary departure. For multi-owner businesses, this is one of the most critical documents in the entire estate plan.

Two Primary Structures

Cross-purchase: Each remaining owner buys the departing owner's share directly. Surviving owners typically receive a stepped-up cost basis in the purchased interest, which reduces future capital gains exposure.

Entity redemption: The business itself buys back the interest. Simpler to administer with multiple owners, but surviving owners generally don't receive a basis increase.

The 2024 Supreme Court decision in Connelly v. United States added a significant wrinkle to entity redemption structures. The Court held that a corporation's obligation to redeem shares using life insurance proceeds did not offset those proceeds when valuing the deceased owner's estate for federal estate tax purposes.

That ruling directly increased estate tax exposure for surviving owners in entity redemption arrangements. Business owners with existing buy-sell agreements should review them with qualified tax and legal counsel to assess the impact.

Valuation Methodology

How the agreement defines business value matters enormously. Common approaches:

- Fixed price — easy to set, often outdated within a few years

- Formula-based — tied to earnings multiples or book value; more dynamic

- Independent appraisal — most accurate but requires a process to trigger

An outdated or ambiguous valuation method is among the most common sources of disputes between surviving partners and the deceased owner's heirs. Build a review schedule into the agreement itself — tied to a specific interval or a triggering event like a new partner joining or a significant change in revenue.

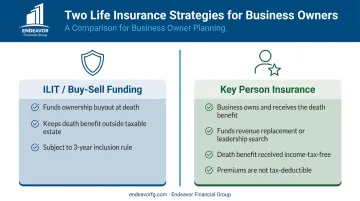

Solving the Liquidity Problem With Insurance

Even a well-structured succession plan can leave the surviving family in a difficult position. If the business owner's salary stops at death and the business can't require distributions to inactive family members, there's an income gap that can appear within weeks.

How Life Insurance Fits In

Life insurance addresses two problems at once:

- Buy-sell funding — gives the surviving owner or entity the cash to purchase the deceased's share without draining operating capital

- Income replacement — provides immediate liquidity for the surviving spouse or dependents

An Irrevocable Life Insurance Trust (ILIT) can hold the policy so the death benefit stays outside the taxable estate — an important consideration for larger estates. Policies transferred to an ILIT from the owner's direct ownership are subject to a three-year inclusion rule under IRC Section 2035, so timing matters.

Key Person Insurance

This is a separate strategy. The business owns a policy on a key owner or employee, pays the premiums, and receives the death benefit. The proceeds can replace lost revenue, fund a search for a replacement, or satisfy lender requirements that may require key person coverage.

Under IRC Section 264, premiums paid on policies where the business is the beneficiary are generally not tax-deductible. However, the death benefit is typically received income-tax-free — and for most businesses, that tax-free payout far outweighs the lost deduction on premiums.

Tax-Smart Strategies for Transferring Business Wealth

Lifetime Gifting and Valuation Discounts

Transferring minority interests in the business to family members or trusts while you're alive can reduce your taxable estate. Minority interests may qualify for valuation discounts — for lack of marketability or lack of control — which means a $500,000 interest might be valued lower for gift tax purposes.

Those discounts also interact with the broader estate tax picture. The federal estate tax exemption is $13,990,000 for 2025 — the Tax Cuts and Jobs Act increase was originally set to expire, but legislation retained the higher exemption. For most small business owners, that threshold isn't an immediate concern. For growing businesses, though, the math can shift faster than owners expect.

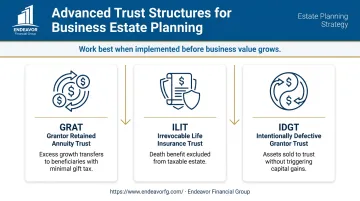

Advanced Trust Structures

For higher-value estates, three tools are worth understanding:

- GRATs (Grantor Retained Annuity Trusts) — the grantor receives an annuity; if trust assets grow faster than the IRS discount rate, the excess transfers to beneficiaries with minimal gift tax cost

- ILITs (Irrevocable Life Insurance Trusts) — keeps life insurance proceeds outside the taxable estate

- IDGTs (Intentionally Defective Grantor Trusts) — separate from the estate for estate and gift tax purposes, but owned by the grantor for income tax, so assets can be sold to the trust without triggering capital gains

All three work best when implemented before business value grows significantly. Endeavor Financial Group coordinates with estate planning attorneys to evaluate which structures fit a client's situation — choosing tools based on business structure, growth trajectory, and family dynamics.

Charitable Planning

Beyond trust structures, charitable giving can serve a dual purpose in estate planning. For owners with philanthropic goals, a Charitable Remainder Trust (CRT) reduces the taxable estate while generating an income stream during the owner's lifetime. CRTs tend to make the most sense when:

- The estate is large enough that tax reduction is a priority

- The owner holds appreciated assets (such as business stock) to contribute

- Long-term charitable intent is already part of their financial plan

Whether a CRT fits your strategy depends on the full estate picture — which is why it's worth reviewing alongside your other transfer tools, not in isolation.

Frequently Asked Questions

What are the 5 D's of succession planning?

The 5 D's are the key events that trigger a forced ownership transition: Death, Disability, Divorce, Disagreement (or Dispute), and Departure (retirement or voluntary exit). A strong succession plan addresses all five, not just death.

What is the 5 by 5 rule in estate planning?

The 5 by 5 rule is a trust provision under IRC Section 2041 that allows a beneficiary to withdraw the greater of $5,000 or 5% of trust assets each year without triggering gift tax consequences — preserving estate tax efficiency while giving beneficiaries limited access to funds.

When should a small business owner start estate planning?

Now — regardless of age or business size. Strategies like GRATs and lifetime gifting programs lose effectiveness as business value increases, so earlier planning almost always means better financial outcomes.

What happens to my business if I die without an estate plan?

Without an estate plan, the business enters probate — a court-supervised process that can take a year or more, freeze operating funds, and transfer ownership according to state intestacy laws rather than your wishes. That operational disruption often permanently erodes business value before a successor can take control.

Do I need both a will and a buy-sell agreement?

Yes. They serve different purposes. A will governs personal asset distribution at death; a buy-sell agreement governs how business ownership interests transfer among co-owners or the entity. Both are typically needed — and if they contradict each other, the conflict can trigger litigation, delay ownership transfers, and leave the business without clear leadership during the dispute.