Simply having the money isn't enough; you need a strategy to make it work for you. This article will break down seven distinct retirement income strategies. We'll explore how they work, their pros and cons, and how to think about choosing the right approach for your $500k portfolio.

TL;DR: Key Takeaways

- Common strategies range from systematic withdrawals (the 4% rule) to dividend investing and annuities.

- The best plan blends multiple strategies to match your personal risk tolerance and income needs.

- A financial planner can help build a personalized roadmap for a complex financial picture.

Why a Formal Income Strategy is Crucial for a $500K Portfolio

Reaching a $500,000 portfolio is a major milestone. At this level, growth from compounding can significantly outpace your contributions. A formal strategy is essential to harness this growth while protecting your nest egg from the risks of retirement.

Without a plan, you risk falling victim to three major challenges:

- Sequence of Returns Risk: Experiencing poor returns in early retirement can permanently damage your portfolio if you're forced to sell assets during a downturn. In fact, research from Morningstar shows this risk is present in nearly 70% of failed retirement simulations.

- Longevity Risk: Retirements can now last 25-30 years, creating the risk of outliving your savings. The Social Security Administration estimates that one in three 65-year-olds will live past 90, so your plan must account for a long lifespan.

- Inflation Risk: The rising cost of living erodes your purchasing power over time. With inflation averaging around 2.5% over the last 30 years, your income must grow just to maintain your current lifestyle.

7 Retirement Income Strategies for Your $500K Portfolio

Managing retirement income isn't one-size-fits-all. Different strategies address different needs, from simplicity and flexibility to security and growth. Here are seven distinct approaches to consider.

1. The Systematic Withdrawal Plan

This is the most straightforward strategy. You simply withdraw a fixed percentage or dollar amount from your portfolio each year to live on.

- Follows the "4% Rule" by taking out a set percentage—like $20,000 from a $500k portfolio—and adjusting annually for inflation.

- Ideal for retirees who value simplicity, predictability, and full control over their investments.

- Easy to implement and flexible enough to adjust withdrawals, keeping your portfolio invested for long-term growth.

- Vulnerable to market downturns (sequence of returns risk), as fixed withdrawals may force you to sell assets at a loss.

2. The Total Return Investing Approach

This strategy focuses on achieving the best possible total return from capital gains, dividends, and interest, rather than focusing only on income-producing assets. You generate your "paycheck" by selling assets as needed.

- Build a diversified portfolio for overall growth and sell assets as needed to generate income, ideally those that have performed well.

- Suits flexible retirees with a higher risk tolerance who want to maximize total portfolio growth.

- Enables a fully diversified, growth-oriented portfolio and can be more tax-efficient since you control when to realize capital gains.

- Lacks a predictable "paycheck" and requires the discipline to sell assets, which can be difficult during market downturns.

3. Dividend Growth Investing

With this approach, you build a portfolio of high-quality companies with a long history of consistently increasing their dividend payments. The goal is to live off the dividends without touching your principal investment.

- Create a portfolio of quality dividend-paying stocks to generate a regular, automatic cash flow without selling shares.

- Best for those who want a rising income stream to fight inflation and prefer not to sell their core assets.

- Delivers a tangible, growing income stream that can be less stressful than actively selling shares.

- Can be difficult to generate sufficient income; a 3% yield on $500k is only $15,000 per year.

- May lead to an under-diversified portfolio if you over-concentrate in dividend-heavy sectors, and companies can always cut dividends.

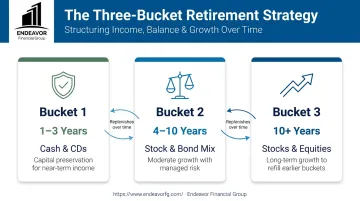

4. The Bucket Strategy

This is a risk-management strategy where you divide your portfolio into three distinct "buckets" based on time horizon.

- How it works:

- Bucket 1 (1-3 years of expenses): Held in cash, CDs, or very short-term bonds for immediate income needs.

- Bucket 2 (4-10 years of expenses): A balanced mix of stocks and bonds for moderate growth.

- Bucket 3 (10+ years): Primarily stocks and other growth assets for long-term appreciation.

- A great fit for retirees who want to stay invested for growth but worry about short-term market volatility.

- The cash bucket creates a psychological buffer against market downturns, protecting your long-term growth investments.

- More complex to manage, as it requires periodically rebalancing and refilling the cash bucket from the other buckets.

5. Fixed-Income Laddering

This strategy involves buying multiple bonds or CDs with staggered maturity dates. As each one matures, you can use the principal for income or reinvest it in a new bond at the long end of the ladder.

- Buy bonds or CDs with staggered maturity dates (e.g., 1, 2, 3, 4, and 5 years) and reinvest the principal as each one matures.

- Good for conservative retirees who prioritize capital preservation and predictable income over high growth.

- Creates a predictable income stream and reduces interest rate risk by not locking you into a single rate.

- Returns are typically lower than stock strategies and may not keep pace with inflation; principal is tied up until maturity.

6. Using Annuities for Guaranteed Income

An annuity is an insurance product where you pay a lump sum to an insurance company in exchange for a guaranteed stream of income for a set period or for life.

- Allocate a portion of your portfolio (e.g., $100,000) to an insurance company to create a "personal pension" that pays you for life.

- Designed for risk-averse retirees who want to guarantee essential expenses are covered and fear outliving their money.

- Provides a guaranteed lifetime income, which removes market and longevity risk for the annuitized portion of your funds.

- You lose control and liquidity over your principal, and fixed payments can lose purchasing power to inflation.

- Contracts are often complex, and fees can be high, so careful review is essential.

7. Real Estate Income via REITs

Real Estate Investment Trusts (REITs) are companies that own and operate income-producing real estate. Buying shares of REITs on the stock market is a simple way to earn real estate income without being a landlord.

- Buy shares of a publicly-traded REIT just like a stock. The REIT pays out rent it collects from its properties as dividends.

- Ideal for investors wanting diversification from stocks and bonds with a passive income stream tied to real estate.

- Offers the potential for high dividend yields, plus liquidity and diversification across many properties.

- Share prices can be as volatile as stocks and are sensitive to interest rates. Dividends are often taxed at a higher ordinary income rate.

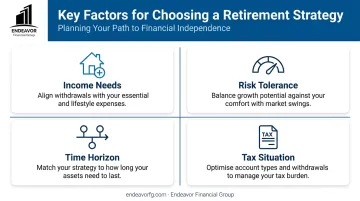

How to Choose the Right Mix of Strategies for Your Portfolio

The best plan rarely relies on a single strategy. Instead, it often involves combining two or more. For example, you might use an annuity to cover essential needs (Strategy 6) and a total return approach for discretionary spending (Strategy 2).

When building your personalized plan, consider these key factors:

- Assess your income needs by separating essential expenses (housing, healthcare) from discretionary wants (travel, hobbies). A strong plan covers necessities with more secure income sources.

- Define your risk tolerance. If you are uncomfortable with market fluctuations, you might lean toward bond ladders and annuities. A higher tolerance may favor a total return or dividend approach.

- Evaluate your time horizon. Your age and health are key factors, as a longer retirement requires growth-oriented strategies to ensure your money outpaces inflation.

- Analyze your tax situation. Where your assets are held (taxable, tax-deferred, or tax-free) is critical for building an efficient withdrawal strategy that minimizes taxes.

Common Pitfalls to Avoid When Building Your Income Plan

As you design your strategy, be mindful of common mistakes that can derail even a well-funded retirement plan.

Chasing Unsustainably High Yields

It's tempting to invest in assets just because they offer a high dividend yield. But these high yields often come with high risk, which can lead to dividend cuts and a loss of your principal investment.

Ignoring Tax Inefficiency

Not considering the tax implications of your withdrawals is a costly mistake. For example, pulling money from a traditional IRA is taxed as ordinary income, which could mean a 22% federal rate for a single filer in 2025.

In contrast, qualified dividends or long-term capital gains from a taxable account could be taxed at a lower 15% rate. A smart withdrawal strategy can save you thousands.

Being Too Conservative or Too Aggressive

There are risks on both ends of the spectrum. Investing too conservatively means your portfolio may not grow enough to outpace inflation, causing you to lose purchasing power over time. Being too aggressive exposes you to a major market crash that could permanently impair your portfolio. A balanced approach is key.

Build Your Clear Roadmap to Financial Freedom with Endeavor Financial Group

Turning a $500K portfolio into a reliable income stream is achievable, but it’s not simple. Navigating different strategies, managing taxes, and adapting to market changes can be overwhelming, which is where professional guidance becomes invaluable.

At Endeavor Financial Group, we are fee-only, fiduciary advisors specializing in creating personalized retirement strategies for pre-retirees. Our priority is to provide unbiased advice that always serves your best interests.

Our consultative, five-step process provides a clear roadmap from discovery to ongoing monitoring. We partner with you to build a plan that delivers the financial confidence you deserve for this new chapter of life.

Frequently Asked Questions

What should I do when my portfolio reaches $500,000?

This is the time to shift your focus from accumulation to distribution. Create a formal, written retirement income plan that outlines how you will generate cash flow and manage risks, then stress-test it against different market scenarios.

How much annual income can I safely withdraw from a $500,000 portfolio?

The 4% rule suggests an initial withdrawal of $20,000 per year, but this is just a starting point. A safe amount depends on your age and asset allocation, with most financial planners now recommending a more flexible range of 3.5% to 5%.

Is the 4% rule still a good guideline for retirement?

It's a useful starting point for planning, but it's no longer a set-it-and-forget-it rule. Many financial planners now suggest a more flexible approach or a lower initial withdrawal rate due to changing market conditions and longer lifespans.

How do I protect my $500k retirement fund from market downturns?

Key strategies include proper asset allocation (owning a mix of stocks and bonds), holding a cash reserve to cover 1-2 years of expenses (as in the Bucket Strategy), and owning non-correlated assets that can provide stability.

Do I need a financial advisor if I have a $500,000 portfolio?

While not required, an advisor is highly valuable at this stage. A fiduciary advisor helps optimize tax efficiency, manage withdrawal strategies, and provide objective guidance during market volatility to keep your plan on track.