The solution isn't just about how much you've saved, but how you withdraw it. A tax-savvy withdrawal plan is one of the most powerful tools you have to protect your savings and make your money last. This guide provides a complete roadmap for pre-retirees, small business owners, and executives looking to create a durable, tax-efficient income stream for life.

Key Takeaways

- Strategically choosing which accounts to tap minimizes your lifetime tax bill.

- Use the "Three-Bucket" strategy (taxable, tax-deferred, tax-free) to organize assets.

- Withdrawal order matters—a blended approach often beats a sequential one.

- Advanced tactics like Roth conversions and QCDs can lower your taxable income.

- A personalized plan is crucial, as the best strategy depends on your unique goals.

How Your Retirement Accounts Are Taxed: A Quick Primer

Before building a tax-savvy withdrawal strategy, it's crucial to understand how your accounts are treated by the IRS. Your retirement assets fall into three distinct tax categories, and knowing the difference is the first step toward an efficient retirement.

Taxable Accounts (The "Pay-as-You-Go" Bucket)

These are your standard investment accounts funded with money you’ve already paid taxes on. Think of a brokerage account, mutual fund, or high-yield savings account.

- Funding: Funded with after-tax dollars.

- Tax on Growth: You pay taxes on earnings—like interest and dividends—annually as you receive them.

- Tax on Withdrawals: When you sell an investment, you pay capital gains tax. Assets held for more than one year are taxed at lower long-term capital gains rates (currently 0%, 15%, or 20%, depending on your income). Assets held for one year or less are taxed at higher ordinary income rates.

Tax-Deferred Accounts (The "Tax-Me-Later" Bucket)

This bucket includes the most common retirement accounts, such as Traditional 401(k)s, 403(b)s, and Traditional IRAs. You get a tax break today in exchange for paying taxes tomorrow.

- Funding: Funded with pre-tax dollars, which reduces your taxable income in the year you contribute.

- Tax on Growth: Your investments grow tax-deferred, meaning you don’t pay any taxes on gains year to year.

- Tax on Withdrawals: Every dollar you withdraw in retirement is taxed as ordinary income. According to the IRS, distributions from traditional IRAs are generally taxed as ordinary income.

- RMDs: You are required to take Required Minimum Distributions (RMDs) starting at age 73, which will increase to age 75 in 2033.

Tax-Free Accounts (The "Never-Taxed-Again" Bucket)

These accounts, including Roth IRAs, Roth 401(k)s, and Health Savings Accounts (HSAs), offer the most attractive tax treatment in retirement.

- Funding: Funded with after-tax dollars, so there's no upfront tax deduction.

- Tax on Growth: Your money grows completely tax-free.

- Tax on Withdrawals: Qualified withdrawals of both your contributions and the earnings are 100% tax-free.

- RMDs: Roth IRAs have no RMDs for the original owner, allowing the money to continue growing tax-free for your entire life.

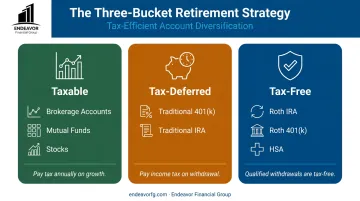

The “Three-Bucket” Strategy: A Framework for Tax Diversification

Visualizing your assets in these three buckets is the key to building a flexible withdrawal plan. The goal is to build a healthy mix across all three. This tax diversification gives you control.

Imagine you have a year with unexpectedly high expenses or want to take a big trip. If all your money is in a Traditional 401(k), pulling out a large sum could push you into a much higher tax bracket.

With assets in all three buckets, you can navigate different financial scenarios strategically:

- For high-income years: Withdraw from your tax-free Roth accounts to avoid being pushed into a higher tax bracket.

- For low-income years: Draw from tax-deferred accounts (like a Traditional IRA) to take advantage of lower tax brackets.

Here's a simple breakdown of which accounts fall into each bucket:

| Taxable Bucket | Tax-Deferred Bucket | Tax-Free Bucket |

|---|---|---|

| Brokerage Accounts | Traditional 401(k)s & 403(b)s | Roth IRAs |

| Mutual Funds | Traditional IRAs | Roth 401(k)s & 403(b)s |

| High-Yield Savings | SEP & SIMPLE IRAs | Health Savings Accounts (HSAs) |

| Stocks & Bonds | Pensions | Roth 457(b)s |

This flexibility allows you to actively manage your tax bracket year by year, which is the core of a smart retirement income plan.

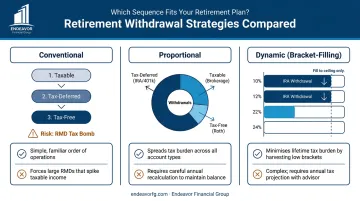

Strategic Withdrawal Sequences: Which Order is Best for You?

With your assets organized into tax buckets, the key question becomes: which one do you tap first? The answer depends on your goals, but there are three primary strategies to consider.

The Conventional Wisdom: Taxable First

The traditional approach is to spend down your accounts in this order:

- Taxable Accounts

- Tax-Deferred Accounts

- Tax-Free (Roth) Accounts

This approach allows your tax-advantaged accounts—especially the powerful tax-free Roth—to grow for as long as possible.

However, this strategy has a major pitfall. By saving tax-deferred accounts for last, you can create a "tax time bomb." Balances can grow so large that when Required Minimum Distributions (RMDs) kick in, the forced withdrawals can push you into a higher tax bracket for life.

The Proportional Withdrawal Strategy

A more balanced approach is to pull a proportional amount from each bucket every year. This helps smooth out your tax liability over your entire retirement, potentially keeping you in a lower marginal tax bracket each year.

For example, if you need $80,000 for living expenses and your portfolio is split:

- 50% in tax-deferred accounts

- 30% in taxable accounts

- 20% in tax-free accounts

You would withdraw $40,000, $24,000, and $16,000 from each bucket, respectively. This bucket. This method avoids the RMD "tax bomb" by gradually drawing down your tax-deferred accounts over time.

The Dynamic or "Bracket-Filling" Strategy

This advanced strategy optimizes your taxes on a year-by-year basis. The goal is to "fill up" the lower tax brackets with income from your tax-deferred accounts.

For instance, you might withdraw just enough from your Traditional IRA to take full advantage of the 12% and 22% federal tax brackets. Once you've hit the top of that bracket, any additional money you need for the year is taken from your taxable or tax-free accounts. This approach gives you precise control over your taxable income each year.

Advanced Tax-Saving Strategies for Retirees

Beyond your withdrawal sequence, several powerful tools can further reduce your tax bill in retirement.

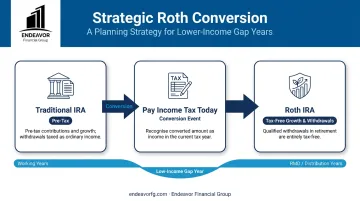

Strategic Roth Conversions

A Roth conversion involves moving money from a tax-deferred account (like a Traditional IRA) to a tax-free Roth IRA. You pay ordinary income tax on the converted amount today in exchange for all future growth and withdrawals being tax-free.

The best time to do this is often in the "gap years"—the period after you retire but before you start taking Social Security and RMDs. During these low-income years, you can convert funds at a much lower tax rate, reducing your future RMDs and building up your tax-free bucket.

Managing Required Minimum Distributions (RMDs)

For retirees who are charitably inclined and over the age of 70½, the Qualified Charitable Distribution (QCD) is a valuable tool. A QCD allows you to donate up to $113,000 in 2025 (an amount indexed for inflation) directly from your IRA to a qualified charity. The distribution counts toward your RMD for the year but is excluded from your taxable income.

Leveraging a Health Savings Account (HSA)

An HSA is a uniquely powerful retirement account available due to its triple tax advantage:

- Contributions are tax-deductible.

- The money grows tax-free.

- Withdrawals are tax-free when used for qualified medical expenses.

In retirement, you can use your HSA to pay for Medicare premiums, co-pays, dental work, and even long-term care insurance with completely tax-free dollars.

Tax-Loss Harvesting and Asset Location

Tax-loss harvesting involves selling investments in your taxable brokerage account at a loss. These losses can then be used to offset capital gains from your winning investments, reducing your tax liability.

Asset location is another key strategy. This involves placing tax-inefficient assets (like corporate bonds) in tax-deferred accounts, while keeping tax-efficient assets (like index funds) in your taxable accounts to minimize the annual tax drag.

Putting It All Together: Creating Your Tax-Savvy Withdrawal Plan

Creating an optimal withdrawal plan involves more than just picking an account. It requires a holistic strategy that coordinates your income sources, manages your tax bracket, and anticipates future liabilities.

This is where professional guidance becomes invaluable. An effective plan must navigate the complex interplay between RMDs, Social Security taxation (the “tax torpedo”), and income-related adjustments to Medicare premiums.

According to the Social Security Administration, up to 85% of your benefits can become taxable depending on your other income—a threshold that IRA withdrawals can easily trigger.

At Endeavor Financial Group, our team of CFP® and CFA® professionals builds personalized roadmaps to manage these complexities. As a fee-only fiduciary, our advice is legally bound to your best interest. We don't sell products or earn commissions; we provide unbiased guidance tailored to your unique situation.

Our process ensures your plan is actively managed and adjusted as your life changes, including:

- Discovery and strategy planning

- Coordinated implementation

- Ongoing support and adjustments

Frequently Asked Questions

What is the best tax strategy for retirement?

There is no single "best" strategy. An effective plan typically combines tax diversification (the three-bucket system), a smart withdrawal sequence, and advanced tactics like Roth conversions, all tailored to your personal financial situation and goals.

How long will $500,000 last using the 4% rule?

Using the 4% rule, you could withdraw $20,000 in the first year. However, minimizing taxes is crucial because it helps your principal last longer and more effectively sustain your income needs.

How do Required Minimum Distributions (RMDs) impact my withdrawal plan?

RMDs are mandatory, fully taxable withdrawals that can push you into a higher tax bracket. A sound financial plan anticipates RMDs and uses strategies like Roth conversions or Qualified Charitable Distributions (QCDs) to manage their tax impact.

Is a Roth conversion a good idea for me?

A Roth conversion may be beneficial if you expect a higher tax bracket in retirement or want to reduce future RMDs. It requires paying taxes upfront on the converted amount, so the decision must be weighed carefully against your financial situation.

What is the "tax torpedo" and how can I avoid it?

The "tax torpedo" occurs when a small income increase, such as an IRA withdrawal, causes a much larger portion of your Social Security benefits to become taxable. This can be avoided by managing withdrawals to keep your income below key tax thresholds.

Does my state tax retirement income?

State tax laws vary significantly. Some states have no income tax (e.g., Florida, Texas, Nevada), while others offer partial or full exemptions for retirement income. It is critical to factor state-level taxes into your overall withdrawal strategy.