The core challenge is that succession planning is far more than a financial transaction. It's an emotional journey that touches on legacy, identity, and complex family dynamics. Without a clear roadmap, owners risk not only their company's future but also their family's harmony and financial security.

This guide provides that roadmap. We’ll walk through a clear, comprehensive process for navigating succession planning, turning a daunting challenge into a manageable, strategic process that secures your legacy for years to come.

Key Takeaways

- Family business succession is a multi-year process, not a one-time event, designed for a smooth transfer of leadership and ownership.

- Failing to plan can lead to business failure, diminished value, family conflict, and significant tax liabilities.

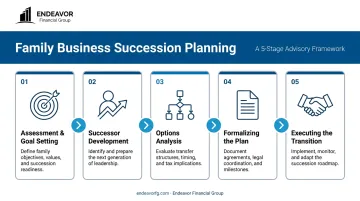

- A successful plan involves five key stages: Assessment, Successor Development, Options Analysis, Implementation, and Transition.

- Critical factors to manage include business valuation, family dynamics, governance structures, and tax implications.

- The most common mistakes are starting too late, poor communication, and the founder's inability to let go.

What Is Family Business Succession Planning?

Family business succession planning is the process of strategically transitioning a company's leadership and ownership to the next generation or new owners. It’s a deliberate, long-term strategy designed to ensure the business continues to thrive long after the founder steps away.

Its primary goals are to:

- Ensure business continuity and stability.

- Preserve family wealth and the founder's legacy.

- Maintain harmony among family members.

This goes far beyond a simple retirement plan. A comprehensive plan includes management training for the next leader and a structured transfer of ownership. It also involves strategic tax planning and formal legal agreements to govern the transition.

Why Is Succession Planning Critical for Family Businesses?

The stakes couldn't be higher. While 30% of family businesses make it to the second generation, only about 12% are still viable by the third. Despite this, a staggering number of owners are unprepared. According to a PwC survey, only 34% of North American family businesses have a robust, documented succession plan.

Inaction creates significant risks that can unravel a lifetime of work.

- Operational disruption if an owner's sudden departure halts operations, stalls key decisions, and threatens the company’s survival.

- Diminished business value from a rushed sale or poorly managed transition, which often triggers unnecessary taxes and erodes family wealth.

- Destructive family conflict when a lack of clarity over roles and fairness leads to disputes that poison the company culture.

How the Succession Planning Process Works: A Step-by-Step Guide

Thinking about succession can feel overwhelming. The best way to approach it is as a structured journey with manageable stages. A well-executed plan typically unfolds over five to ten years.

Step 1: Foundational Assessment and Goal Setting (5-10 Years Out)

Before you can plan your destination, you need to know your starting point. This initial phase is about gathering information and defining what success looks like for you and your family.

First, conduct a thorough business assessment. This means analyzing your company's financial health, operational strengths and weaknesses, and competitive position in the market. A key part of this step is getting a professional business valuation to establish a clear, objective baseline.

Next, clarify your personal and financial goals. What do you want your retirement to look like? What legacy do you want to leave? How much financial independence do you need from the business after you exit? Answering these questions honestly is crucial for building a plan that works for you personally.

Step 2: Identifying and Developing Potential Successors (3-7 Years Out)

With your goals defined, the focus shifts to future leadership. It's vital to objectively evaluate potential successors, whether they are family members or key employees. Don't let birthright be the only qualification. Define clear criteria for the role based on skills, experience, leadership potential, and genuine commitment to the business.

Once a successor is identified, create a formal leadership development plan. This isn't about shadowing you for a few months; it's a multi-year process.

- Provide broad exposure: Ensure they work across different departments like finance, operations, and sales.

- Encourage outside experience: Working for another company can provide invaluable perspective and credibility.

- Establish mentorship: Pair them with key non-family employees and trusted advisors to broaden their support network.

Step 3: Analyzing Succession Options and Financial Structuring (2-5 Years Out)

This is where the plan starts to take concrete shape. You’ll explore the primary succession strategies to determine the best fit for your business and family. The main options include:

- Pass the business to the next generation to preserve a family legacy. This path requires careful management of internal family dynamics.

- Sell to insiders through a management/employee buyout (MBO/EBO) or an Employee Stock Ownership Plan (ESOP) to maintain company culture.

- Sell to a third party, such as a strategic acquirer or private equity firm, which often yields the highest financial return and provides a clean exit.

This stage is financially and legally complex. You must develop a structure for the transfer that minimizes taxes, often using strategies like gifting shares or setting up trusts. A team of expert advisors is indispensable here.

Business owners should work with a comprehensive financial planner, like the fiduciary advisors at Endeavor Financial Group, to act as a "quarterback" coordinating with legal and tax professionals. This ensures your exit strategy aligns with your personal retirement and estate goals.

Step 4: Formalizing the Plan and Communication (1-2 Years Out)

With a clear strategy in place, it's time to document everything. Your succession plan should be a formal, written document that details timelines, roles, responsibilities, and contingency plans.

Work with legal counsel to draft all necessary agreements, such as buy-sell agreements, updated shareholder agreements, and estate planning documents. These legal structures turn your intentions into binding commitments, preventing confusion and conflict down the road.

Finally, develop a communication plan for all stakeholders. This includes family members (both those in the business and those who aren't), key employees, customers, and lenders. Transparency is key to building confidence and ensuring a smooth, stable transition.

Step 5: Executing the Transition and Letting Go (The Transition Period)

This is the final and often most emotionally challenging step. Implement the plan according to your timeline, gradually transferring responsibilities and decision-making authority to your successor.

As the founder, you must prepare to truly step back. This means redefining your role—perhaps as a board member or an informal mentor—and allowing the new leadership to take full control. Resisting the urge to intervene is critical for empowering your successor and allowing the business to move into its next chapter.

Key Factors That Influence a Succession Plan

Secure Your Family Business's Future with Expert Financial Planning

Request a quote and our experts will contact you within 24 hours with tailored solutions and pricing.

For immediate assistance, feel free to give us a direct call at 463-273-4062. You can also send us a quick email at team@endeavorfg.com.

For immediate assistance, feel free to give us a direct call at 463-273-4062. You can also send us a quick email at team@endeavorfg.com.