For those with a taxable investment portfolio, there's a more strategic and tax-efficient way to be generous. Gifting highly appreciated stock—securities you've held for over a year that have grown in value—can significantly amplify your impact.

This article will break down the practical benefits of this strategy, the common mistakes to avoid, and the key steps to executing it effectively. You’ll learn how to maximize your generosity while minimizing your tax bill.

TL;DR: Key Takeaways on Gifting Appreciated Stock

- Eliminate capital gains tax by gifting stock held for over one year.

- Deduct the stock's full market value when donating to charity.

- Transfer stock to individuals tax-free up to the annual exclusion amount.

- Avoid taxes by gifting stock directly instead of selling it for cash first.

- Consult a financial advisor to ensure this strategy fits your overall plan.

What Is Gifting Highly Appreciated Stock?

Gifting highly appreciated stock is the direct transfer of ownership of stocks or mutual funds—that have grown significantly in value since you bought them—to another person or organization.

This strategy is most powerful for "long-term" holdings, which are assets you've owned for more than one year. If you were to sell these assets, the gains would be subject to long-term capital gains tax.

By transferring the shares directly, you bypass that taxable event entirely. This transforms the gift into a strategic tool for achieving philanthropic or estate planning goals in a tax-efficient way.

Key Benefits of Gifting Highly Appreciated Stock

Gifting appreciated stock offers two key advantages: significant tax savings for you and a larger potential gift for the recipient. The benefits differ slightly depending on whether you're gifting to a charity or to family members.

Maximize Your Charitable Impact & Tax Efficiency

When you donate appreciated stock directly to a qualified charity, you unlock a powerful "double tax benefit."

First, you can generally avoid paying the capital gains tax you would have owed if you sold the stock. This means the charity receives the full, pre-tax value of the asset. A larger gift for them, no tax bill for you.

Second, if you itemize deductions, you may be eligible for a charitable tax deduction for the stock's full fair market value at the time of the gift. This is subject to certain Adjusted Gross Income (AGI) limits, typically 30% for this type of donation to a public charity.

Let's look at a hypothetical comparison. Imagine you're a high-income earner wanting to donate $50,000 from stock that you originally purchased for $20,000.

| Metric | Scenario A: Sell Stock, Then Donate Cash | Scenario B: Donate Stock Directly |

|---|---|---|

| Asset Value | $50,000 | $50,000 |

| Capital Gain | $30,000 | $0 (not realized by you) |

| Capital Gains Tax Paid | $7,140 (at 23.8% combined rate) | $0 |

| Net Donation to Charity | $42,860 | $50,000 |

| Value of Your Deduction | $42,860 | $50,000 |

As the table shows, donating the stock directly results in $7,140 more for the charity and a larger potential tax deduction for you. This strategy is most effective for investors who itemize deductions and hold appreciated assets in a taxable brokerage account.

Transfer Wealth to Family Strategically

You can also gift stock to children, grandchildren, or other individuals. While you don't get a charitable deduction, you still avoid paying capital gains tax at your own, likely higher, tax rate.

The recipient inherits your original cost basis (what you paid for the stock) and holding period. They will be responsible for capital gains tax when they eventually sell, but they may be in a much lower tax bracket. This can result in a significantly lower overall tax bill for the family.

You can do this tax-free using the annual gift tax exclusion. For 2024, you can give up to $18,000 per person without filing a gift tax return. A married couple can combine their exclusions to gift up to $36,000 per recipient.

However, keep a few important considerations in mind:

- A child's unearned income over a certain threshold ($2,600 for 2024) could be subject to the "Kiddie Tax" and taxed at your higher rate.

- Gifted assets can reduce a student's eligibility for college financial aid, as they are assessed at a much higher rate (20%) than parental assets.

This strategy is often best for transferring wealth to adult children or grandchildren who are in a lower tax bracket and can let the investment continue to grow.

The Common Mistake: What Happens When You Sell First?

The most frequent and costly error people make is selling the appreciated stock and then gifting the cash. This single mistake negates the primary advantage of the strategy.

When you sell first, you create an immediate tax liability. You must pay federal and potentially state capital gains tax on the profit, which instantly shrinks the amount of money available to give.

This turns a tax-efficient transfer into a tax-inefficient one, leaving thousands of dollars with the IRS instead of your chosen recipient.

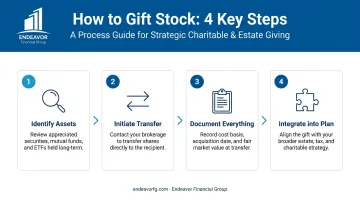

How to Get the Most Value from Your Gift: 4 Key Steps

Maximizing this strategy requires careful planning. The process isn't complex, but following these steps is crucial for success.

1. Identify the Right Assets and Recipient

Look through your taxable brokerage account for securities you've held for more than one year with the largest unrealized gains. These assets provide the greatest tax benefit. For charitable gifts, confirm the organization is a qualified 501(c)(3) that can accept stock transfers. For gifts to individuals, make sure they have a brokerage account ready to receive the shares.

2. Initiate the Transfer (Do Not Sell)

Contact your brokerage firm to begin the process. Request a direct transfer of the shares from your account to the recipient's account. This typically involves completing a specific form or providing a letter of instruction with the recipient's brokerage details. Do not click the "sell" button.

3. Document Everything

Keep meticulous records. For your tax files, you'll need to note the fair market value on the date of the transfer. For charitable donations, you must file IRS Form 8283 if your total non-cash contributions exceed $500 for the year. While a formal appraisal is often required for non-cash donations over $5,000, this rule generally doesn't apply to publicly traded securities.

4. Integrate the Gift into Your Financial Plan

A stock gift shouldn't be an isolated decision; it should be part of a holistic wealth management strategy. At Endeavor Financial Group, we integrate these decisions into our comprehensive planning process. A Certified Financial Planner™ professional can help you select the right assets without disrupting your portfolio's balance or jeopardizing long-term goals, ensuring your generosity aligns with your complete financial picture.

A Smarter Way to Be Generous

Gifting highly appreciated stock is one of the most powerful yet underutilized strategies for tax-efficient giving. By transferring securities directly, you can eliminate a significant tax liability for yourself while maximizing the value of the gift for the people and causes you care about most.

If you're ready to make your wealth work harder for others, start by reviewing your portfolio for these opportunities. To see how this powerful strategy fits into your personal financial roadmap, schedule a complimentary meeting with the team at Endeavor Financial Group.

Frequently Asked Questions

Can I gift highly appreciated stock?

Yes, you can gift appreciated stock to both qualified charities and individuals. It is a common and tax-smart financial strategy for assets held for more than one year in a taxable account.

How can I avoid capital gains tax when gifting highly appreciated stock?

You avoid the tax by transferring the shares directly to the recipient instead of selling them first. By doing this, you as the donor do not realize the capital gain and therefore do not trigger a taxable event.

What do I need to report to the IRS when donating appreciated stock valued at more than $5,000?

For non-cash charitable gifts over $500, you must file IRS Form 8283. For donations of publicly traded securities over $5,000, you report it in Section A of the form; a qualified appraisal is generally not required.

What is the difference between gifting stock to family versus a charity?

Gifting to a qualified charity can provide a "double benefit": avoiding capital gains tax and potentially receiving an income tax deduction. Gifting to family avoids the capital gains tax for you but does not provide a tax deduction.

Will I have to pay gift tax if I give stock to my children?

You likely won't pay gift tax as long as the stock's value is below the annual gift tax exclusion limit, which is $18,000 per recipient in 2024. Any amount gifted above that simply reduces your lifetime gift and estate tax exemption.

What is "cost basis" and why does it matter for the recipient?

Cost basis is the original purchase price of the stock. When you gift stock to an individual, they inherit your cost basis, which is used to calculate their capital gains tax if they decide to sell it in the future.