The pattern is real, and the cause isn't usually bad investing.

Research tied to Roy Williams and Victor Preisser's work on wealth transfer, referenced by Stanford Graduate School of Business, found that 70% of attempted inheritances result in loss of control of assets — with unprepared heirs and family communication failures driving most of that erosion.

Family governance is the framework that breaks this pattern. Not a legal document, not an estate plan — a living system for how families make decisions, communicate across generations, and protect what they've built. This guide explains what it is, why it matters, and how to build one.

Key Takeaways

- 70% of wealth transfers fail — driven by communication breakdowns and unprepared heirs, not poor investment returns

- Family governance is the operating framework for your family's financial life: shared values, clear roles, and defined decision-making processes

- Core components: family mission statement, constitution, council, succession plan, and conflict resolution process

- Start before a crisis forces the conversation — an imperfect framework in place today beats a perfect one that never gets built

- A fee-only fiduciary advisor can serve as a neutral facilitator, helping families build and sustain governance structures from wealth accumulation through estate transfer

What Is Family Governance?

Family governance is the agreed-upon set of principles, roles, and processes a family uses to make financial decisions, communicate across generations, and plan for leadership and wealth transitions. Think of it as the operating system for your family's financial life.

That distinction matters — because family governance is not the same as estate planning. Estate planning creates legal structures: wills, trusts, powers of attorney, beneficiary designations. Those documents govern what happens to assets. Family governance governs how family members work together before, during, and after those transitions. The two should complement each other closely, but neither replaces the other.

Governance isn't reserved for the ultra-wealthy. Any of the following creates a strong case for it:

- Families with meaningful assets heading toward a generational transfer

- Business owners whose children or heirs may eventually inherit or run the company

- Multi-generational families who will share financial decisions over time

Even a simple written mission statement and a commitment to regular family conversations provide real structural value.

Why Family Wealth Rarely Survives Three Generations

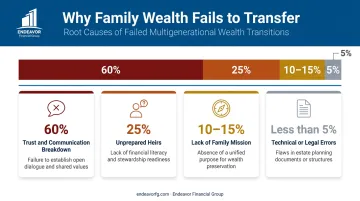

According to a 2022 Vanguard/FPA presentation citing Williams and Preisser's research, 70% of wealthy families lose control of their assets by the second generation, and 90% by the third. The Institute for Preparing Heirs breaks down the causes:

- 60% of failures stem from a breakdown of trust and communication among family members

- 25% from heirs who weren't prepared for the responsibilities they inherited

- 10–15% from a lack of a defined family mission

- Less than 5% from technical or legal-document errors

The legal mechanics — the trust structures, the wills — account for almost none of the failure. The human dynamics account for nearly all of it.

The Communication Gap

When families avoid discussing wealth openly, younger generations inherit assets without context, without expectations, and without the financial vocabulary needed to steward them. The result is management failures and family conflict — often simultaneously.

Money conversations feel uncomfortable, so families put them off. But silence doesn't protect the next generation; it leaves them unprepared for decisions they'll eventually have to make. And when preparation is missing, the behavioral gaps don't stay abstract — they show up as real financial mistakes.

The Unprepared Heir Problem

Heirs often face the same behavioral traps that wealth-creators spent decades overcoming — impulsive spending, chasing returns, difficulty maintaining long-term discipline — because they never received structured financial education. Research on mental accounting from the Federal Reserve Bank of St. Louis shows that people tend to treat inherited or gifted money as less tied to effort, which can lead to spending it more freely than wages.

The Succession Gap

For business-owning families, the stakes are especially high. A 2023 PwC Family Business Survey found that only 34% of US family businesses had a robust, documented, and communicated succession plan in place. When a family business has no written plan, a death, disability, or unexpected retirement can force rushed decisions that damage both the business and family relationships.

The Essential Components of a Family Governance Structure

No two families have identical governance, but effective structures share core building blocks that can be scaled to the family's size and complexity.

Family Mission Statement and Constitution

A family mission statement captures the shared values behind the wealth — the purpose it serves, the principles that guide decisions, and the legacy the family is working toward. Putting it in writing creates a reference point for disagreements; without one, every major financial decision becomes a fresh negotiation.

The family constitution (sometimes called a charter or protocol) is the practical extension of that mission. It defines:

- How decisions are made and who holds authority in which areas

- Whether decisions require consensus or voting — and how voting works

- What happens during major transitions (business sales, deaths, divorces)

- Policies on employment, ownership, and compensation for family members

The constitution won't prevent every disagreement, but it gives families a defined process to follow when one arises — which is often the difference between a resolved dispute and a fractured relationship.

Family Council and Defined Roles

The family council is the governing body that meets on a regular cadence — typically two to six times per year, according to Family Business UK's guidance, with sibling-stage families often meeting at least quarterly. Effective meeting agendas typically include:

- Business and financial updates

- Progress on succession or transition planning

- Family education and next-generation development

- Policy decisions and open concerns

Clearly defined roles matter as much as the meeting itself. Ambiguous authority breeds resentment. Specify who manages day-to-day finances, who communicates with outside advisors, who represents different family branches, and what authority each role carries.

Succession Plan and Conflict Resolution

The succession plan outlines how leadership, financial stewardship, and business ownership transition from one generation to the next — including the triggers and timelines that govern those transitions. Treat it as a living document, reviewed on a set schedule rather than drafted once and filed away.

A well-structured succession plan typically addresses:

- Leadership transition triggers (retirement, incapacity, voluntary exit)

- Ownership transfer timelines and valuation methodology

- Roles for family members who aren't involved in day-to-day operations

- Contingency provisions for unexpected events

Every governance structure also needs a built-in conflict resolution mechanism. When disagreements follow an agreed-upon process — mediation, an advisory vote, an outside facilitator — they're far less likely to damage relationships permanently. Fair process matters even when the outcome isn't unanimous.

Building Your Family Governance Framework Step by Step

Most families that struggle with governance do so because they started with documents instead of dialogue. These five steps build the framework in the right order.

Start with values, not rules. Before drafting any documents, have honest conversations about what the wealth is for, what legacy matters most, and what principles should anchor every financial decision. Let those conversations shape the structure — not the other way around.

Involve all generations from the beginning. Governance handed down from one generation rarely takes hold. Bring younger family members into the process early and create genuine space for their perspectives, even if their formal decision-making roles will grow over time.

Define roles and decision-making authority with specificity. Vague assignments breed resentment. Be explicit about who does what, which decisions require full-council input, and how authority shifts as the family evolves — when children become adults, when a business is sold, when the family grows.

Commit to regular, structured family meetings. Governance only works if the family practices it. Establish a meeting cadence, use an agenda, and treat these meetings as non-negotiable. A family that meets twice a year reliably will outperform one with ambitious schedules that go unfollowed.

Build flexibility into the framework. Families change through marriages, divorces, births, and shifting priorities. Design structures that can adapt without abandoning their core foundation. Schedule periodic reviews to update the charter and roles as circumstances change.

How a Financial Advisor Supports Family Governance

Family dynamics — parental authority, sibling rivalries, wide gaps in financial literacy — make these conversations genuinely difficult to have internally. A trusted, objective advisor changes that. When an outside professional structures the discussion, every voice gets heard and the conversation stays productive rather than personal.

What a Comprehensive Advisor Brings

A financial advisor working with multigenerational families will:

- Structure family meetings with clear agendas and facilitation

- Identify gaps in existing plans — misaligned estate documents, unfunded succession plans, undefined roles

- Coordinate with estate attorneys and CPAs to ensure legal documents align with governance goals

- Provide ongoing monitoring as the family's situation evolves through marriages, business events, and generational transitions

Endeavor Financial Group structures this kind of work through a five-step process — from discovery and analysis through implementation and ongoing monitoring. The firm coordinates across estate planning, tax strategy, business succession, and family financial education, functioning as the central point of contact for the client's complete financial picture.

What to Look for in an Advisor

When choosing an advisor for governance support, prioritize:

- CFP® or CFA® credentials, which signal rigorous training and adherence to ethical standards

- A fiduciary obligation — meaning the advisor is legally required to put your interests first, not their own

- Hands-on experience with multigenerational families or business owners, since governance conversations require a different skill set than portfolio management

- A structured process that covers estate planning, succession, tax strategy, and family communication — not just investment returns

Frequently Asked Questions

How is family governance different from estate planning?

Estate planning creates the legal structures — wills, trusts, powers of attorney — that govern what happens to assets. Family governance is the operational framework for how family members communicate, make decisions, and prepare for transitions. The two work in tandem: governance frameworks guide behavior and culture, while estate documents carry legal weight.

Do you need to be very wealthy to benefit from family governance?

No. While governance structures tend to be more formal for larger or more complex families, any family with meaningful assets, a family business, or multiple generations involved in financial decisions can benefit. Even a simple written mission statement and regular family meetings provide real, measurable value.

What is the most common reason family wealth fails to transfer to the next generation?

Research consistently points to a lack of preparation and communication — not poor investing. Unprepared heirs, undefined expectations, and the absence of shared financial education account for the vast majority of wealth erosion across generations. Technical or legal errors account for less than 5% of failures.

How often should a family council meet?

Quarterly or semiannual meetings work well for most families. Consistency matters more than frequency — a family that meets twice a year reliably will outperform one with ambitious schedules that never get followed. More complex families or those navigating active transitions may benefit from meeting more frequently.

Should in-laws or spouses be included in family governance discussions?

Many families include spouses in meetings and educational programs but reserve formal decision-making roles for blood relatives or designated members. Establish a clear, consistent policy early and apply it uniformly across all family branches.

How do we start governance conversations with reluctant family members?

Start with willing participants and build a structure that demonstrates value over time — reluctant members often come around once they see it working. A neutral facilitator or experienced advisor can open these conversations in a way that lowers defensiveness and keeps everyone at the table.