Fortunately, the U.S. tax code provides a powerful set of tools designed to help you save more efficiently. These tax-advantaged retirement plans are specifically built to reduce your tax burden while your investments grow.

This guide will walk you through the major types of tax-advantaged retirement plans available. We’ll cover options for employees, individuals, and small business owners, giving you the clear, straightforward information you need to make the right decisions for your financial future.

TLDR: Your Guide to Tax-Smart Retirement Saving

- Use tax deductions or tax-free withdrawals to help your money grow faster.

- Common options include employer-sponsored 401(k)s and individual IRAs.

- Business owners can use plans like SEP IRAs for much higher contribution limits.

- Your ideal plan depends on your goals; an advisor can help build your strategy.

What Are Tax-Advantaged Retirement Plans?

A tax-advantaged account is a savings or investment vehicle that receives preferential tax treatment from the government. The goal is to encourage people to save for important long-term goals, especially retirement. This tax advantage typically comes in one of two forms.

The Two Main Types of Tax Advantages

Understanding the difference between "tax-deferred" and "tax-exempt" is the key to choosing the right account for your situation.

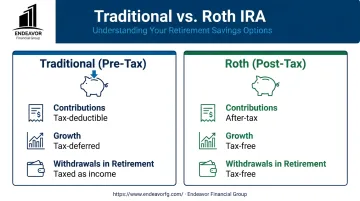

Tax-deferred (pre-tax) plans allow contributions that may be tax-deductible in the year you make them. This lowers your current taxable income, which can mean a smaller tax bill today. Your investments grow tax-deferred, and you only pay income tax when you withdraw the funds in retirement.

- Examples: Traditional 401(k), Traditional IRA, SEP IRA.

Tax-exempt (post-tax) plans use contributions made with money that has already been taxed, so you don’t get an upfront deduction. In exchange, your investments grow completely tax-free, and qualified withdrawals in retirement are also free from federal income tax.

- Examples: Roth 401(k), Roth IRA.

Employer-Sponsored Retirement Plans: Building Your Foundation

For many Americans, the journey to retirement savings starts at work. If your employer offers a retirement plan, it's often the best place to begin, especially if they offer a company match.

The 401(k) Plan

The 401(k) is the cornerstone of retirement savings for those working in the private sector. You contribute a portion of your paycheck automatically, making it an easy and consistent way to save.

Key features of a 401(k) include:

- Pre-Tax Contributions: Your contributions are taken from your paycheck before income taxes are calculated, which reduces your current taxable income.

- Tax-Deferred Growth: Your investments grow over time without being taxed on dividends or capital gains.

- Employer Match: Many companies offer to match your contributions up to a certain percentage of your salary. This is free money and one of the best returns on investment you can get. A common matching formula is a 50% match on the first 6% of your pay, according to Vanguard's annual How America Saves report.

- High Contribution Limits: For 2024, you can contribute up to $23,000. If you're age 50 or over, you can contribute an additional $7,500 as a "catch-up" contribution.

Beyond the traditional pre-tax model, many companies now offer a Roth 401(k) option. While it uses the same payroll deductions and may include an employer match, your contributions are made with after-tax dollars. The advantage? Qualified withdrawals in retirement are completely tax-free.

The 403(b) Plan

A 403(b) plan is very similar to a 401(k), but it’s offered to employees of public schools, colleges, hospitals, and certain non-profit or religious organizations. The contribution limits and tax-deferred structure are generally the same as a 401(k). For 2024, the employee contribution limit is also $23,000, with a $7,500 catch-up for those 50 and older.

Individual Retirement Accounts (IRAs): Take Control of Your Savings

An Individual Retirement Account (IRA) is a powerful tool available to anyone with earned income. IRAs often provide a much wider range of investment choices—including stocks, bonds, ETFs, and mutual funds—giving you more control over your portfolio.

Traditional IRA

A Traditional IRA lets your investments grow tax-deferred. Depending on your income and whether you have a retirement plan at work, your contributions may be tax-deductible.

For 2024, you can contribute up to $7,000 to an IRA, or $8,000 if you are age 50 or older. Withdrawals are taxed as ordinary income in retirement. Under the SECURE 2.0 Act, you must begin taking Required Minimum Distributions (RMDs) from your Traditional IRA starting at age 73.

Roth IRA

The Roth IRA is a favorite for many savers because of its powerful tax benefit: tax-free growth and tax-free withdrawals in retirement (as long as you're over 59½ and have had the account for at least five years).

Contributions are made with after-tax dollars, so they are not deductible. For 2024, the ability to contribute phases out for single filers with incomes between $146,000 and $161,000.

Another major benefit is that Roth IRAs do not have Required Minimum Distributions (RMDs) for the original owner. For high-income earners above the limit, a "backdoor Roth IRA" strategy may be an option.

Retirement Plans for Small Business Owners & Self-Employed

Retirement Plans for Small Business Owners & Self-Employed

If you're a business owner or self-employed, you have access to some of the most powerful retirement savings vehicles available. These plans are designed to help you save aggressively for your own future while potentially offering benefits to your employees.

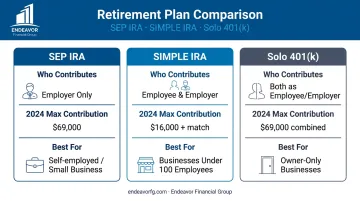

SEP IRA (Simplified Employee Pension)

A SEP IRA is a straightforward, low-administration plan that's perfect for self-employed individuals and small businesses.

- How it works: Only the employer (or the self-employed individual acting as the employer) makes contributions.

- High limits: You can contribute up to 25% of compensation, not to exceed $69,000 for 2024.

- Flexibility: You can decide how much to contribute each year, or even skip contributions if business is slow.

SIMPLE IRA (Savings Incentive Match Plan for Employees)

Designed for businesses with fewer than 100 employees, the SIMPLE IRA is easier and less costly to set up than a 401(k).

- How it works: It allows for both employee and employer contributions.

- Employee contributions: In 2024, employees can contribute up to $16,000 (or $19,500 if age 50 or over).

- Mandatory employer contributions: Employers must either match employee contributions up to 3% of their salary or make a 2% non-elective contribution for all eligible employees.

Solo 401(k)

For a self-employed individual with no employees (other than a spouse), the Solo 401(k) is often the most powerful option. It allows you to contribute as both the "employee" and the "employer," maximizing your savings potential.

- Employee contribution: You can contribute up to $23,000 in 2024 (plus a $7,500 catch-up if 50 or older).

- Employer contribution: You can also contribute up to 25% of your compensation as the "employer."

- Combined limit: The total combined contributions cannot exceed $69,000 for 2024, according to the IRS.

- Roth option: Allows for post-tax Roth contributions as the employee.

- Loan availability: May permit you to take a loan from your plan balance, offering more flexibility.

How to Choose the Right Retirement Plan for You

Selecting the best plan—or combination of plans—depends entirely on your personal circumstances. There's no single right answer, but you can narrow down your choices by considering a few key factors:

- Your employment status: Are you an employee, a business owner, or self-employed?

- Your income: Do you expect to be in a higher or lower tax bracket in retirement? This helps decide between Traditional (pre-tax) and Roth (post-tax) accounts.

- Your savings goals: How much can you realistically afford to save each year?

- Your business structure: If you're a business owner, do you have employees?

Here is a simple framework to guide your decisions:

- Get the full match. If you have a 401(k) or 403(b) at work with an employer match, contribute at least enough to capture every dollar. It's an unbeatable return.

- Max out an IRA. After getting your match, consider contributing to an IRA. A Roth IRA is often a great choice if you qualify, as tax-free income in retirement is incredibly valuable.

- Leverage a business plan. If you own a business or have self-employment income, use a SEP IRA, SIMPLE IRA, or Solo 401(k) to save significantly more than you could in an IRA alone.

Navigating these options to build a strategy that aligns with your long-term goals can be complex. This is where professional guidance can provide clarity and confidence.

Partnering with Endeavor Financial Group means working with a fee-only fiduciary. Our legal and ethical obligation is to always act in your best interest, ensuring our advice is unbiased and tailored to your unique situation.

Our team specializes in creating personalized roadmaps for pre-retirees and small business owners. We help you make sense of choices like a SEP vs. Solo 401(k) and integrate them into a cohesive financial plan.

This process includes crucial tax planning and risk management, transforming complex financial goals into a clear, actionable plan for the future.

Frequently Asked Questions

What is a tax-advantaged retirement savings plan?

It's a government-approved account like a 401(k) or IRA that offers tax benefits, such as tax-deductible contributions or tax-free growth, to encourage you to save for retirement.

Can you have a retirement account and still receive Social Security benefits?

Having a retirement account does not disqualify you from receiving Social Security retirement benefits. However, withdrawals from tax-deferred accounts (like a Traditional 401(k) or IRA) are taxable income, which could affect whether your Social Security benefits are taxed.

Can I retire at 62 with $400,000 in my 401(k)?

This depends entirely on your lifestyle, health, expected expenses in retirement, and other sources of income. Working with a financial advisor to create a comprehensive plan is the best way to determine if this amount is sufficient for your specific needs.

What is the difference between a Traditional and a Roth account?

Traditional accounts use pre-tax dollars, giving you a potential tax deduction now, but you pay taxes on withdrawals later. Roth accounts use after-tax dollars, so you get no upfront deduction, but qualified withdrawals are tax-free.

What should I do with my 401(k) when I change jobs?

You generally have four options: leave it with your old employer (if allowed), roll it into your new employer's 401(k), roll it over into an IRA, or cash it out (which usually triggers taxes and penalties).