The next few decades will witness the largest transfer of wealth in history. Projections estimate that $124 trillion will change hands in the U.S. through 2048, a staggering figure that represents a lifetime of work, innovation, and savings for millions of families. But intergenerational wealth transfer is about much more than just passing down money. It’s about transferring values, opportunities, and a lasting legacy.

Successfully navigating this process requires more than just a will. It demands thoughtful communication, careful preparation, and a strategic plan. This guide provides a clear roadmap for families looking to secure their financial future and ensure their legacy thrives for generations to come.

TL;DR: Key Takeaways

- Define Your Legacy: Successful wealth transfer starts with defining family values and goals, not just financial assets.

- Communicate Openly: A lack of communication is the primary reason wealth is lost. Regular family meetings are essential.

- Prepare Your Heirs: Financial education is crucial to equip the next generation to be responsible stewards of wealth.

- Use the Right Tools: A combination of wills, trusts, and strategic gifting is necessary to protect assets and minimize taxes.

- Build a Professional Team: Working with a financial advisor, attorney, and tax professional ensures a cohesive and effective plan.

Why Intergenerational Wealth Planning is More Critical Than Ever

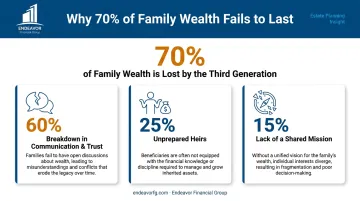

Passing on wealth is deceptively difficult. A widely cited 20-year study by The Williams Group found that 70% of families lose their wealth by the second generation and a shocking 90% lose it by the third. This isn't a matter of bad luck; it's a failure to plan.

The primary reasons for this breakdown are almost entirely preventable. Research shows the leading causes are:

- A breakdown in family communication and trust (60%)

- Heirs who are inadequately prepared to manage wealth (25%)

- Lack of a shared family mission or vision

This highlights a critical truth: without a proactive strategy, the assets you've worked a lifetime to build are at risk. Planning isn’t just for the ultra-wealthy; it’s a necessity for anyone who wants to secure their family's future and protect their legacy.

The Foundation: Building Your Legacy Beyond the Numbers

The most successful wealth transfers begin long before any legal documents are drafted. They start with defining wealth in broader terms than just financial assets and preparing the family for the responsibilities that come with it.

Clarify Your Family's Mission and Values

Before you can decide how to transfer wealth, you must define why. A family mission statement or a set of guiding principles creates a shared purpose that can guide decisions for generations. Ask yourself: what do you want your wealth to accomplish?

This isn't just an exercise. It's the glue that holds a multi-generational plan together. Your values might include:

- Education: Ensuring future generations have access to higher learning.

- Entrepreneurship: Providing seed capital for family members to start businesses.

- Philanthropy: Creating a legacy of giving back to the community.

- Financial Responsibility: Instilling principles of smart saving, investing, and debt management.

Once you have a clear vision for your legacy, the next step is to share it.

Foster Open and Honest Communication

Money is often a taboo topic, but silence is the single biggest threat to a successful wealth transfer. Holding regular family meetings is essential for creating transparency and managing expectations.

To make these conversations easier, start with values, not numbers. Discuss the family's mission and goals before diving into specific assets or inheritance amounts. This approach shifts the focus from entitlement to shared purpose and stewardship.

Open communication builds alignment, but true stewardship also requires financial competence.

Prioritize Financial Education for Heirs

An inheritance can be a burden if the recipient is unprepared to manage it. Preparing your heirs to be responsible stewards of wealth is one of the greatest gifts you can give them. This education should go beyond basic budgeting and cover key concepts like investing, managing debt, and understanding market cycles.

Practical ways to educate heirs include:

- Involving them in philanthropic decisions to teach them about impactful giving.

- Giving them a small investment portfolio to manage with guidance.

- Encouraging them to work and build their own financial foundation.

- Connecting them with a trusted financial advisor to build their own financial literacy.

Essential Estate Planning Tools for Wealth Transfer

Once your family’s vision is clear, it’s time to build the legal and financial structure to support it. The right combination of tools will depend on your goals, net worth, and family dynamics.

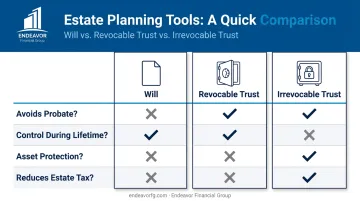

The Last Will and Testament

A will is the foundational document of any estate plan. It outlines how your assets should be distributed, names guardians for minor children, and appoints an executor to carry out your wishes. However, a will alone is often not enough. Assets passed through a will must go through probate—a public, often lengthy, and costly court process.

Leveraging Trusts for Control and Protection

A trust is a legal entity that holds and manages assets on behalf of your beneficiaries. A key advantage is that assets held in a trust typically avoid probate, allowing for a private and efficient transfer. Trusts also provide greater control over how and when assets are distributed.

Several types of trusts are common in wealth transfer planning:

- Revocable Living Trusts allow you to manage assets during your lifetime and can be changed or revoked at any time. A successor trustee distributes the assets according to your instructions, bypassing probate.

- Irrevocable Trusts cannot be easily changed but offer powerful benefits for tax reduction and asset protection. Common types include:

- Irrevocable Life Insurance Trust (ILIT): Helps life insurance proceeds pass to heirs tax-free.

- Spousal Lifetime Access Trust (SLAT): Allows one spouse to gift assets for the other’s benefit while removing them from their combined taxable estate.

Strategic Gifting During Your Lifetime

Beyond planning for the future, you can also transfer wealth during your lifetime. Gifting assets allows you to reduce your taxable estate and witness the positive impact of your generosity. The IRS allows you to give a certain amount to any individual each year without tax consequences.

- Annual Gift Tax Exclusion: For 2024, you can give up to $18,000 to as many individuals as you like, tax-free. A married couple can combine their exclusions to give up to $36,000 per person.

- Lifetime Gift Tax Exemption: Gifts above the annual exclusion amount count against your lifetime exemption. For 2024, this amount is $13.61 million per individual.

Titling Assets and Beneficiary Designations

Finally, some of the most effective wealth transfer tools aren't complex documents but simple administrative updates. How you own your assets matters.

Retirement accounts like 401(k)s and IRAs, as well as life insurance policies, pass directly to the individuals named as beneficiaries, bypassing your will entirely. It is critical to review these designations regularly, especially after major life events like marriage, divorce, or the birth of a child.

Navigating Common Challenges in Wealth Transfer

Even the best-laid plans can face obstacles. Anticipating common challenges is key to building a resilient wealth transfer strategy.

Minimizing the Tax Burden

Taxes can significantly erode an inheritance if not planned for properly. Understanding the two main types of tax is the first step:

- Estate Tax: A federal tax levied on an individual's estate before assets are distributed. Most estates fall below the high exemption threshold.

- Inheritance Tax: A state tax paid by the recipient of an inheritance. Only a handful of states impose this tax, and Indiana does not have an inheritance tax. The few states that do include Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania, according to the Tax Foundation.

Strategic tools like irrevocable trusts and lifetime gifting are the primary methods for legally minimizing exposure to federal estate taxes.

Managing Complex Family Dynamics

Wealth can amplify underlying family tensions, especially in blended families or when distributions are unequal. Transparency and clear communication are the best tools for preventing conflict. Appointing a professional trustee or an independent executor can also ensure impartiality and reduce the potential for family friction.

Planning for Business Succession

For business owners, succession planning is a critical component of intergenerational wealth transfer. A formal succession plan ensures the business can continue to operate smoothly after the owner’s death or retirement, protecting both the family’s wealth and the employees' livelihoods. This plan should be tightly integrated with the personal estate plan to avoid conflicts.

How Endeavor Financial Group Can Help You Build a Lasting Legacy

Transferring wealth to the next generation is complex, but our process makes it clear. At Endeavor Financial Group, we partner with you on everything from defining your values to executing detailed financial strategies. As fee-only fiduciaries, we are legally bound to act in your best interest, ensuring our advice is always unbiased.

Our five-step process provides a clear roadmap for your legacy:

- Discovery: We start with a conversation to understand your family, values, and vision for the future. This foundation ensures your plan is uniquely yours.

- Analysis: Our team conducts a deep review of your complete financial picture, identifying opportunities and potential risks to your estate.

- Recommendations: We present a clear, actionable strategy tailored to your goals, explaining how each component works to secure your legacy.

- Implementation: We coordinate with your estate planning attorney and tax professionals to ensure every will, trust, and account is properly structured and funded.

- Ongoing Monitoring: A legacy plan must adapt. We regularly review your plan to adjust for life events, law changes, and shifting family dynamics.

By looking at your complete financial picture, we help you build a cohesive strategy that preserves your wealth, prepares your heirs, and secures your legacy for generations to come.

Frequently Asked Questions

What is one of the biggest risks to intergenerational wealth transfer?

The biggest risks are unprepared heirs and a lack of communication within the family. These two factors are responsible for the majority of wealth transfer failures, leading to mismanagement, family conflict, and the rapid depletion of assets.

What is the best way to transfer wealth to heirs?

The best approach is a customized strategy using tools like trusts, wills, and strategic gifting based on your family's goals. It is essential to develop this plan with a team of financial, legal, and tax professionals.

How much can you gift to someone tax-free each year?

As of 2024, you can gift up to $18,000 to any individual without filing a gift tax return. A married couple can combine their exemptions to gift up to $36,000 to each recipient.

What is the difference between a will and a trust?

A will directs asset distribution after death and must go through the public probate process. In contrast, a trust can manage assets during and after your life and typically allows your estate to avoid probate.

Should I tell my children about their inheritance?

You don't need to share specific dollar amounts, but you should communicate that a plan exists. Discussing family values and the responsibilities of wealth helps prepare heirs to be good stewards of their inheritance.