This isn't just about picking stocks; it's about building a fortress. The top 1% of U.S. taxpayers pay over 38% of all federal individual income taxes, making tax mitigation a critical component of wealth preservation, not just an afterthought. This article outlines seven essential wealth management strategies that form the foundation of a robust financial plan designed to protect what you've built.

Key Takeaways

- Wealth management for HNWIs requires integrated strategies for tax mitigation, estate planning, and risk management that go beyond standard financial advice.

- Key tactics include advanced tax planning, diversifying with alternative investments, creating a comprehensive estate plan, and robust asset protection.

- Philanthropy and business succession planning are crucial for legacy building and transferring wealth efficiently.

- A successful plan depends on creating a cohesive strategy and partnering with an expert advisory team.

Why High-Net-Worth Wealth Management Requires a Specialized Approach

As wealth grows, financial complexity increases exponentially. The standard advice that works for the average investor—like maxing out a 401(k)—is often just the starting point for a high-net-worth individual. The financial landscape is simply different.

The key differences boil down to three areas:

- Higher Tax Burdens: With greater income and assets comes a significantly higher tax liability. HNWIs need sophisticated strategies that go far beyond standard deductions to minimize their tax exposure legally and effectively.

- Greater Liability Exposure: Significant wealth can also attract legal risks and lawsuits. A survey from Chubb found that 68% of affluent families worry about the size of an adverse liability verdict, making asset protection a critical defensive strategy.

- Complex Investment Opportunities: HNWIs have access to exclusive and more complex investment vehicles like private equity, hedge funds, and private credit. While these can offer higher returns and diversification, they also come with illiquidity and unique risks that require expert analysis.

These complexities explain why HNW planning is not a single service but a coordinated effort. It integrates multiple disciplines—investment, legal, tax, and insurance—into a unified strategy.

7 Key Wealth Management Strategies for High-Net-Worth Individuals

A comprehensive wealth plan integrates the following seven strategies to protect and grow your assets effectively.

Strategy 1: Advanced Tax Planning & Mitigation

For HNWIs, minimizing tax liability is a primary goal. This involves proactive strategies that look years, or even decades, ahead.

- Tax-Loss Harvesting: Selling investments at a loss to systematically offset capital gains in other parts of your portfolio.

- Asset Location: Strategically placing tax-inefficient assets (like corporate bonds) inside tax-advantaged accounts (like an IRA) and tax-efficient assets (like index funds) in taxable brokerage accounts.

- Managing Capital Gains: Deferring gains where possible, timing sales to align with lower-income years, or using vehicles like Qualified Opportunity Zones to defer and potentially reduce taxes on gains.

- Roth Conversions: Converting traditional IRA assets to a Roth IRA, especially during lower-income years or in anticipation of higher future tax brackets, to secure tax-free growth and withdrawals in retirement.

Strategy 2: Strategic Investment & Portfolio Diversification

To manage volatility and improve risk-adjusted returns, HNWIs must diversify beyond traditional stocks and bonds. This means incorporating alternative investments that have a low correlation to public markets.

HNWI portfolios often include allocations to assets like:

- Private Equity: Investing in private companies, which can offer high growth potential but requires capital to be locked up for up to 10-12 years.

- Private Credit: Lending money directly to companies, providing income streams that are often insulated from public market swings.

- Real Estate: Direct ownership of commercial or residential properties, or investing in private real estate funds.

- Hedge Funds: Utilizing sophisticated strategies to generate returns in various market conditions.

These assets can enhance returns, but they also bring illiquidity and complexity. A disciplined rebalancing strategy is essential to ensure your portfolio remains aligned with your long-term goals.

Strategy 3: Comprehensive Estate & Legacy Planning

Effective estate planning goes beyond a simple will. It’s a strategic tool for ensuring your wealth is transferred according to your wishes with minimal tax erosion. While the federal estate tax exemption is currently high, it is scheduled to be cut by nearly half in 2026, making advanced planning critical for many high-net-worth families.

Key instruments include:

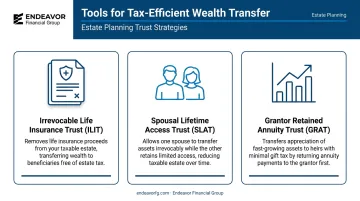

- Irrevocable Life Insurance Trusts (ILITs): Holds a life insurance policy outside of your taxable estate, providing tax-free liquidity to heirs for paying estate taxes or other expenses.

- Spousal Lifetime Access Trusts (SLATs): Allows one spouse to make a gift into a trust for the benefit of the other spouse, removing assets from their combined estates while still allowing indirect access to the funds.

- Grantor Retained Annuity Trusts (GRATs): Enables you to pass asset appreciation to heirs with little to no gift or estate tax.

Legacy planning also involves preparing heirs for their inheritance through education and establishing clear family governance structures to preserve wealth and harmony across generations.

Strategy 4: Robust Risk Management & Asset Protection

Asset protection involves structuring your assets to shield them from potential creditors and lawsuits. This creates a significant protection gap, as studies show that 81% of affluent individuals do not carry excess liability insurance.

Effective asset protection tools include:

- LLCs and Partnerships: Placing assets like real estate or business interests into separate legal entities to shield them from personal liabilities.

- Adequate Umbrella Insurance: Securing a personal liability policy with high limits ($5 million, $10 million, or more) that extends far beyond standard homeowners or auto policies.

- Strategic Use of Insurance: Using life and disability insurance not just for income replacement, but to provide liquidity for an estate or to fund a business buy-sell agreement.

Strategy 5: Strategic Philanthropy & Charitable Giving

For many HNWIs, philanthropy is a core part of their legacy. Strategic giving moves beyond simply writing a check to using more efficient vehicles.

- Donor-Advised Funds (DAFs): Allows you to make a charitable contribution and receive an immediate tax deduction, then recommend grants to your favorite charities over time.

- Charitable Remainder Trusts (CRTs): Generates an income stream for you or your heirs for a set term, with the remaining assets going to a designated charity.

- Donating Appreciated Assets: Gifting highly appreciated stocks or real estate directly to a charity allows you to avoid the capital gains tax you would have paid if you sold the asset, while still getting a fair market value tax deduction.

Strategy 6: Business Succession & Exit Planning

For business owners, their company is often their largest and most illiquid asset. A formal succession or exit plan is essential for maximizing its value and ensuring a smooth transition. This is especially critical when you consider that only about 13% of U.S. family-owned businesses are passed successfully to a third generation.

A strong exit plan includes:

- A Clear Business Valuation: Understanding what your business is worth today.

- Successor Identification: Deciding whether the business will pass to family, be sold to management, or be acquired by an outside party.

- Transaction Structure: Structuring the sale or transfer to be as tax-efficient as possible.

- Personal Financial Integration: Ensuring the proceeds from the sale are integrated into your personal wealth and retirement plan.

Planning years in advance is the key. A rushed exit almost always leaves money on the table.

Strategy 7: Building Your Integrated Financial Team

No single person can be an expert in all these complex areas, so the final strategy is to assemble a team of trusted professionals who work together on your behalf.

The key players on your team should include:

- A Financial Advisor (CFP® or CFA®): This professional, often from a comprehensive firm like Endeavor Financial Group, acts as the "quarterback" to coordinate the overall strategy.

- A Certified Public Accountant (CPA): Provides specialized tax planning and preparation.

- An Estate Planning Attorney: Drafts the necessary legal documents, such as wills and trusts.

- An Insurance Specialist: Analyzes risk and secures appropriate coverage.

True value is unlocked when these professionals collaborate, ensuring your investment strategy aligns with your tax plan and your estate plan reflects your business succession goals.

How to Build a Cohesive Wealth Management Plan

Having individual strategies is not enough; they must be woven into a single, dynamic plan. This requires a structured process that moves from high-level goals to detailed implementation.

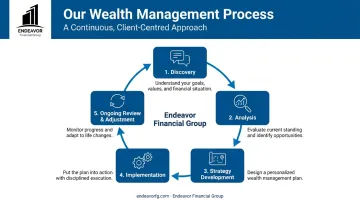

At Endeavor Financial Group, we use a five-step process to build this cohesive roadmap. A well-defined plan should include:

- Discovery: We start by getting to know your values, long-term goals, and risk tolerance. This initial step is about understanding what you truly want to achieve with your wealth.

- Analysis: Our team analyzes your complete financial picture—including assets, liabilities, income, and cash flow—to establish a clear baseline and identify opportunities.

- Strategy Development: Based on the analysis, we develop personalized strategies for the short, intermediate, and long term, presenting them in an easy-to-follow roadmap.

- Implementation: We work alongside you to put the plan into action. This can involve making investment decisions, setting up trusts, or adjusting retirement savings contributions.

- Ongoing Review & Adjustment: A financial plan is never static. We continuously monitor progress and make adjustments as your life, the markets, and tax laws inevitably change.

Your Roadmap to Financial Security

Managing significant wealth is a proactive, ongoing process. A successful plan integrates tax planning, sophisticated investing, risk management, and legacy goals into one cohesive strategy. The power of these seven strategies lies not in using them individually, but in how they work together to protect and grow your assets.

Successfully implementing these strategies requires deep expertise and coordination. At Endeavor Financial Group, our team of CFP® and CFA® professionals specializes in creating comprehensive wealth plans for business owners and pre-retirees. Contact us today to see how these strategies can be tailored into a clear roadmap for your financial future.

Frequently Asked Questions

What wealth management strategies do high-net-worth individuals use?

HNWIs use integrated strategies that combine advanced tax and estate planning with diversified investment portfolios. Key tactics include using trusts for wealth transfer, adding alternative investments, and implementing robust asset protection plans.

What is the difference between wealth management and financial planning for HNWIs?

Financial planning creates the foundational roadmap. Wealth management is a more comprehensive, ongoing service that integrates this plan with sophisticated investment, tax, and legal strategies to manage a client's entire financial life.

How can I protect my assets from potential lawsuits?

Key asset protection tools include securing a high-limit umbrella liability insurance policy, placing assets like real estate or business interests into separate LLCs, and using specific types of trusts designed to shield assets from creditors.

What role do alternative investments play in a HNWI portfolio?

Alternatives like private equity and real estate help diversify a portfolio and reduce its reliance on public markets. While they can offer higher returns, these investments also come with greater risk and are less liquid than traditional assets.

How do I choose the right wealth management advisor?

Seek a fiduciary advisor with credentials like CFP® or CFA®, as they are legally required to act in your best interest. Ensure they have experience with clients like you and use a comprehensive, team-based approach to planning.

Why is tax planning so critical for high-net-worth individuals?

Because HNWIs face higher tax rates and complex finances, strategic tax planning is critical for wealth preservation. It helps maximize after-tax returns, allowing more of your assets to grow and be passed on to future generations.