This is the classic "good problem to have," but it's a problem nonetheless. Selling that stock to diversify your portfolio, fund your retirement, or make a large purchase can trigger a massive tax bill, potentially eroding years of growth. Many investors feel "locked in," afraid to touch their successful investment for fear of the tax consequences.

This article breaks down exactly how those taxes accumulate and explores practical, tax-efficient strategies for managing your appreciated stock. We'll cover everything from foundational concepts to advanced tactics, giving you a clear path forward.

Key Takeaways

- Selling a highly appreciated stock triggers a large capital gains tax bill.

- Your final tax depends on cost basis, holding period, and income bracket.

- Mitigate taxes by gifting shares, donating to charity, or using a Donor-Advised Fund (DAF).

- Manage the sale by staggering it over years or using tax-loss harvesting to offset gains.

How Capital Gains Taxes on Appreciated Stock Accumulate

A capital gain is the profit you make from selling an asset—in this case, stock—for more than you paid for it. The original purchase price is known as your cost basis. The difference between the sale price and your cost basis is the taxable gain.

As long as you hold the stock, this gain is "unrealized," meaning the tax liability is deferred. The tax event is only triggered when you sell the shares. This creates a compounding problem: as the stock's value grows, so does your potential tax bill.

This can make you hesitant to sell, even if your portfolio has become dangerously over-concentrated in a single position. Many experts define this as having more than 10-20% of your portfolio in one stock.

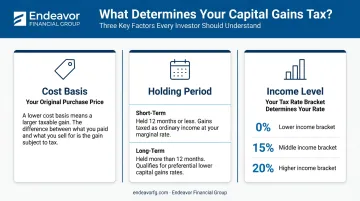

Key Drivers of Your Capital Gains Tax Liability

The total capital gains tax you pay depends on several key factors that can dramatically change the final amount.

Cost Basis

Your cost basis is the original value of an asset for tax purposes. For stock you purchased, it's typically the purchase price plus any commissions. A very low cost basis—common with early employee stock options or an investment held for decades—means that nearly the entire value of the stock is a taxable gain. The lower your basis, the larger your potential tax bill.

Holding Period

The length of time you own an asset is critical. The IRS makes a sharp distinction between short-term and long-term gains.

- Short-Term Capital Gains: Apply to assets held for one year or less. These gains are taxed at your ordinary income tax rates, which are significantly higher than long-term rates.

- Long-Term Capital Gains: Apply to assets held for more than one year. These gains are taxed at preferential rates of 0%, 15%, or 20%. Simply holding an investment for at least one year and a day can cut your tax bill substantially.

Your Income and Filing Status

The specific long-term capital gains rate you pay depends on your total taxable income. The thresholds are adjusted annually for inflation. For the 2024 tax year, the federal long-term capital gains tax brackets are as follows:

| Filing Status | 0% Rate | 15% Rate | 20% Rate |

|---|---|---|---|

| Single | Up to $47,025 | $47,026 – $518,900 | Over $518,900 |

| Married Filing Jointly | Up to $94,050 | $94,051 – $583,750 | Over $583,750 |

Source: IRS Revenue Procedure 2023-34

State Taxes

On top of federal taxes, many states levy their own capital gains taxes. This can add a significant layer to your total tax burden, so it's crucial to factor in your state's rules.

For example, states like California and New York have top income tax rates exceeding 10%, while others like Florida, Texas, and Nevada have no state income tax at all.

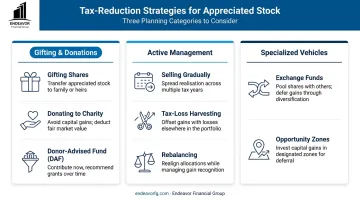

Tax-Reduction Strategies for Highly Appreciated Stock

The best strategy for you will depend on your financial goals, philanthropic intentions, and timeline. The following tactics are grouped by the type of action they require.

Strategies That Involve Proactive Planning & Gifting

These methods focus on moving the stock out of your name before a sale to reduce or eliminate the tax liability.

- Gift Shares to Family Members: You can gift shares to children or other family members who are in a lower tax bracket. For 2024, you can gift up to $18,000 per person without filing a gift tax return. When they sell the stock, the gains are taxed at their lower rate.

- Donate Stock Directly to Charity: Donating appreciated stock to a qualified charity is one of the most powerful tax-planning tools. You can potentially eliminate the capital gains tax on the donated shares and receive a charitable deduction for the stock's full fair market value.

- Use a Donor-Advised Fund (DAF): Use a Donor-Advised Fund (DAF) by donating stock for an immediate tax deduction. The fund sells the shares tax-free, allowing you to recommend grants to various charities from the proceeds over time.

- Establish a Charitable Remainder Trust (CRT): For larger estates, establish a Charitable Remainder Trust (CRT). You transfer stock to an irrevocable trust that sells it tax-free, pays you an income for a set period, and donates the remainder to charity.

Strategies That Focus on Diversification & Active Management

If your goal is to convert the stock into a more diversified portfolio for your own use, these active strategies can help manage the tax impact.

- Sell Gradually Over Multiple Years: Instead of selling a large position all at once, you can sell it in portions over several years. This spreads the tax liability out and can help you stay in a lower capital gains tax bracket each year.

- Offset Gains with Tax-Loss Harvesting: Use tax-loss harvesting by selling other investments at a loss to offset your stock gains. Capital losses cancel out capital gains, and you can deduct up to $3,000 in net losses against ordinary income each year.

- Rebalance with New Contributions: If you are still in your wealth-accumulation years, you can use new cash to invest in other assets. Over time, this will reduce the concentrated stock's portion of your portfolio without triggering a tax event.

Strategies That Use Specialized Investment Vehicles

For high-net-worth investors, certain investment structures offer unique tax-deferral opportunities.

- Contribute to an Exchange Fund: Contribute shares to an exchange fund (or swap fund) to pool them with other investors. You receive a share in a new, diversified portfolio, which allows you to diversify while deferring capital gains taxes. This option is typically limited to high-net-worth investors.

- Invest Gains in an Opportunity Zone: Defer tax on a stock sale by reinvesting the gain into a Qualified Opportunity Fund (QOF). These funds invest in designated low-income communities, and holding the investment for at least 10 years can eliminate tax on the QOF's future growth.

Build Your Personalized Strategy with Endeavor Financial Group

Managing the tax liability from highly appreciated stock isn't about finding a single magic bullet. It requires building a cohesive strategy that aligns with your complete financial picture, from retirement goals to estate planning. The most effective approach often combines several of these tactics and requires careful, forward-looking planning.

At Endeavor Financial Group, we partner with clients to navigate these complexities. Our consultative, five-step structured process—from discovery to ongoing monitoring—is designed to create a clear, personalized roadmap.

As a fee-only fiduciary, our advice is always in your best interest, eliminating the conflicts common in commission-based models. We ensure every decision supports your long-term goals for financial freedom and peace of mind.

If you're looking for a partner to help you protect the value of your investments from unnecessary taxes, let's start a conversation.

Frequently Asked Questions

What should I do with highly appreciated stocks?

The best action depends on your goals but often involves a combination of tax-efficient selling, gifting, or donating. The primary objective is usually to diversify your risk and manage the built-in tax liability in a way that aligns with your financial plan.

What is the difference between long-term and short-term capital gains tax?

Long-term gains, from assets held over one year, are taxed at lower preferential rates (0%, 15%, or 20%). Short-term gains, from assets held one year or less, are taxed at your higher, ordinary income tax rates.

Is it better to gift or inherit highly appreciated stock for tax purposes?

Inheriting is often more tax-efficient, as heirs receive a "step-up in basis" to the market value at the time of death, which can eliminate capital gains tax. In contrast, a person receiving gifted stock inherits your original low cost basis.

What is a donor-advised fund (DAF)?

A DAF is a charitable giving account. You can donate assets like appreciated stock, receive an immediate tax deduction, and then recommend grants from the fund to IRS-qualified public charities over time.

Can I completely avoid taxes on appreciated stock?

You can effectively eliminate your capital gains tax liability on specific shares by donating them directly to a qualified charity. Passing stock to heirs upon death also eliminates the tax for them due to a "step-up in basis."