This is the power of pre-sale estate and tax planning. It's the process of structuring your assets before a sale to dramatically reduce taxes and ensure the wealth you've built is transferred smoothly to your family and legacy goals. Many owners start this process too late, leaving millions of dollars on the table for the IRS.

This guide is for business owners who are planning a future liquidity event. We'll break down what pre-sale planning is, why the timing is critical, and the key strategies you can use to protect your legacy.

Key Takeaways

- Pre-sale planning involves transferring business interests to trusts or heirs before a sale is final to lock in lower valuations and minimize future estate and gift taxes.

- The primary goal is moving the company's future appreciation out of your taxable estate. This should happen well before a sale is "practically certain" to avoid IRS challenges.

- Key strategies include gifting shares to trusts like IDGTs and SLATs, using charitable vehicles like CRTs, and leveraging valuation discounts for private companies.

- The process demands a coordinated team of experts and should ideally begin at least 2-5 years before a potential sale.

What Is Pre-Sale Estate & Tax Planning?

Pre-sale estate and tax planning is a set of proactive legal and financial strategies used to transfer business assets to heirs or charities before a sale. Its primary goal is to separate the business's current value from its much higher future sale value for tax purposes.

By transferring a portion of the company at its current, lower valuation, you allow all future growth to occur outside of your taxable estate. This growth represents the difference between today's value and the final sale price.

This is fundamentally different from post-sale planning. After a sale, you’re left with cash. Cash is simple, liquid, and impossible to discount for tax purposes. In contrast, pre-sale planning leverages the unique nature of the private business itself. Its illiquidity and lower current valuation create tax-saving opportunities that vanish the moment the deal closes.

Why Timing is Everything: The Critical Benefits of Pre-Sale Planning

When transferring business equity, timing is the single most critical factor determining your financial outcome. Acting years before a sale can unlock benefits that are impossible to achieve once a letter of intent is on the table.

Locking in a Lower Valuation

Before a sale is imminent, your business is valued based on its current financial performance. Gifting or selling shares to a trust at this stage uses up far less of your lifetime gift and estate tax exemption. For 2026, the federal exemption is $15 million per person, but a rapidly growing business can exceed that limit quickly. Transferring shares when the company is worth $5 million is far more efficient than waiting until it’s worth $25 million.

The Risk of Waiting: Anticipatory Assignment of Income

If you wait too long, the IRS can invoke a powerful tool called the "Anticipatory Assignment of Income Doctrine." This rule states that if a sale was "practically certain to occur" when you transferred the shares, the IRS can disregard the transfer and tax the entire capital gain to you, the original owner.

While many people see a signed Letter of Intent (LOI) as the point of no return, the reality is more nuanced. A U.S. Tax Court ruling clarified there is no bright-line rule, but the closer a deal is to closing, the higher the risk. The best way to avoid this risk is to plan and act early.

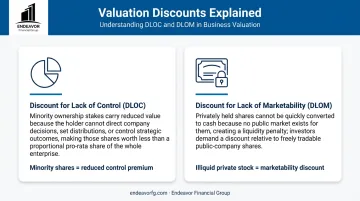

Maximizing Valuation Discounts

Because interests in a privately held business lack the control and marketability of public stocks, tax law allows for valuation discounts. A qualified appraiser can apply discounts that reduce the company's value for tax purposes. These discounts can be substantial, often reducing the reported value by 20-40% or more, according to valuation experts.

The two most common discounts are:

- Discount for Lack of Control (DLOC): Minority shares can't direct company policy, control distributions, or force a sale, making them less valuable than a controlling interest.

- Discount for Lack of Marketability (DLOM): There is no ready market to sell private company stock, making it illiquid and less valuable than a publicly-traded security.

These discounts allow you to transfer more of the company to your heirs while using less of your lifetime gift tax exemption.

Removing Future Appreciation from Your Estate

Imagine you gift a 40% interest in your company, valued today at $5 million, to a trust for your children. The value of that gift, after discounts, might be around $1.5 million.

Now, fast forward three years. You sell the company for $20 million. The 60% you retained is worth $12 million. The 40% in the trust is now worth $8 million. That $6.5 million of appreciation ($8M - $1.5M) grew completely outside of your taxable estate, saving potentially millions in future estate taxes.

How Pre-Sale Planning Works: A 5-Step Framework

Successful pre-sale planning isn't a single transaction but a structured, five-step process that aligns your business exit with your personal financial goals. It requires a coordinated effort and a clear roadmap.

Define Your Personal and Financial Goals This first step answers a critical question: how much of the business can you afford to gift away? To find out, you must quantify your post-exit life. How much capital do you need to fund retirement, support family, or pursue philanthropic goals? The answers define the size and scope of your estate plan.

Assemble Your Advisory Team This is not a DIY project. A successful plan requires a team of specialists working in concert. Key players include:

- A fee-only Wealth Advisor/CFP®: Acts as the "quarterback," coordinating the entire process and ensuring the legal and tax strategies align with your overall comprehensive financial plan.

- An Estate Planning Attorney: Drafts the necessary legal documents, such as trusts and wills.

- A CPA or Tax Advisor: Analyzes the tax implications of each strategy and ensures compliance.

- A Business Appraiser: Provides a qualified, defensible valuation of the business to substantiate any gifts or transfers.

Obtain a Qualified Business Valuation An independent, third-party valuation is the non-negotiable foundation of your entire plan. It provides the basis for all gifting strategies and is your primary defense against a potential IRS challenge. A weak or poorly documented valuation can cause the entire plan to collapse under scrutiny.

Structure and Implement the Strategies With your goals defined, team assembled, and valuation in hand, your advisory team executes the plan. This involves creating trusts, transferring shares, and signing legal documents. The specific strategies chosen will depend on your goals (which we cover below).

Regular Review and Adjustment Pre-sale planning isn't a "set it and forget it" activity. Tax laws change, business performance fluctuates, and family situations evolve. It's essential to review the plan annually with your advisory team and make adjustments as needed in the years leading up to a sale.

Essential Pre-Sale Strategies to Maximize Your Exit

There are several powerful tools available to business owners. The right combination depends on your specific goals, whether they are focused on family wealth transfer, charitable giving, or personal tax reduction.

Gifting and Trust-Based Strategies

Intentionally Defective Grantor Trust (IDGT): Sell shares of your company to a trust for a promissory note. This "freezes" the business's current value in your estate, so all future appreciation grows within the trust and passes to beneficiaries estate-tax-free.

Spousal Lifetime Access Trust (SLAT): Make a large gift to an irrevocable trust for your spouse and descendants to remove assets from your estate. Your spouse can still receive distributions, providing indirect access to the funds if needed.

Grantor Retained Annuity Trust (GRAT): Contribute shares to a trust in exchange for a fixed annuity payment over several years. Any growth above the IRS "hurdle rate" passes to beneficiaries tax-free when the term ends.

Charitable Planning Strategies

Charitable Remainder Trust (CRT): Donate appreciated stock to a CRT pre-sale to get an immediate tax deduction and a lifetime income stream. This defers capital gains tax, and the remaining assets eventually go to your chosen charity.

Donor-Advised Fund (DAF): Contribute company stock to a DAF before the sale to get a fair market value tax deduction now and avoid capital gains. You can then recommend grants to charities from the fund over time.

Tax-Specific Strategies

- Qualified Small Business Stock (QSBS): If your company is a qualifying C-Corporation, Section 1202 may let you exclude 100% of the federal capital gains tax on your sale. This applies to gains up to $10 million or 10x your cost basis, provided you've held the stock for over five years.

Building Your Expert Team & Avoiding Common Pitfalls

The most sophisticated strategies are worthless without proper execution. Two mistakes consistently undermine otherwise brilliant plans:

- Waiting too long. As U.S. Bank advises, effective planning should begin 3 to 5 years before an exit. Starting after a buyer emerges is often too late.

- A disjointed advisory team. When your CPA, attorney, and financial advisor don't communicate, you get conflicting advice and flawed execution. A tax strategy might undermine an estate goal, or a legal structure could create unintended financial consequences.

This is why having a central wealth advisor to act as the "quarterback" is so critical. A comprehensive financial planning firm like Endeavor Financial Group ensures a holistic and coordinated approach.

Our team, which includes professionals with CFP® and CFA® credentials, coordinates directly with your attorney and tax advisors. This ensures every part of your pre-sale plan works in harmony with your long-term retirement and legacy goals, preventing costly oversights.

Frequently Asked Questions

What is the most tax-efficient way to sell a business?

There isn't a single method. The most efficient approach combines pre-sale strategies like gifting shares to irrevocable trusts (IDGTs, SLATs) and using charitable vehicles (CRTs) to reduce both capital gains and future estate taxes before the sale occurs.

What are the 7 steps in the estate planning process?

The process involves defining goals, gathering documents, creating legal structures like wills or trusts, and implementing tax strategies. A crucial final step is to regularly review and update the plan to keep it current.

What does pre-liquidity mean?

Pre-liquidity is the phase before a major financial event, like a business sale, when an owner's wealth is still primarily tied up in illiquid assets. This period is the optimal time for tax and estate planning because you have far more strategic flexibility.

What is a tax planning strategy?

A tax planning strategy is a legal analysis used to reduce tax liability. For business owners, it involves structuring transactions and using tools like trusts or retirement plans to minimize income, capital gains, and estate taxes.

How far in advance of a sale should I start estate planning?

Ideally, you should start planning 2-5 years before a sale. Certain powerful strategies, like those for Qualified Small Business Stock (QSBS), require a five-year holding period to maximize tax benefits.