The good news is that you don't need a crystal ball to build a secure future. You need a plan. This guide will demystify long-term financial planning, breaking it down into a clear, step-by-step process. We’ll cover everything from laying the foundation and setting goals to building and monitoring a strategy that can adapt as your life changes.

TL;DR: Your Long-Term Financial Planning Checklist

- Define Your "Why": Set specific, time-bound goals for what you want to achieve in five, ten, or thirty years.

- Know Your Starting Point: Calculate your net worth and track your cash flow to understand your current financial health.

- Build a Multi-Part Strategy: Create an integrated plan that addresses retirement, investments, debt, and insurance.

- Automate Your Actions: Set up automatic transfers to your savings and investment accounts to ensure consistency.

- Review and Adapt: Life changes, and so should your plan. Revisit it annually and after any major life event.

What is Long-Term Financial Planning (And Why It Matters)

Long-term financial planning is the strategic process of managing your finances to achieve goals that are five or more years away. Unlike short-term planning (saving for a vacation) or mid-term planning (saving for a new car), it focuses on major life milestones like retirement, funding a child's education, or achieving financial independence.

Think of it as a roadmap for your financial life. It provides direction for your day-to-day decisions, reduces stress, and dramatically increases the likelihood that you’ll reach your most important goals.

The power of having a written plan is clear. According to Schwab's 2024 Modern Wealth Survey, while only 36% of Americans have one, 75% of those who do say it makes them feel more in control of their finances.

A plan isn't a rigid, unchangeable document; it's a living guide that provides clarity and peace of mind as you navigate the future.

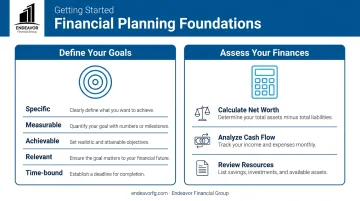

Step 1: Laying the Foundation - Define Your Goals & Assess Your Finances

Step 1: Laying the Foundation - Define Your Goals & Assess Your Finances

Before building a long-term financial plan, you must define your goals and assess your starting point. This foundational step provides the clarity needed for every decision that follows.

Set SMART Financial Goals

Vague wishes like "I want to retire comfortably" are hard to act on. Transform those wishes into SMART goals: Specific, Measurable, Achievable, Relevant, and Time-bound. This framework turns abstract dreams into concrete targets.

For example:

- Vague Wish: "I want to buy a house someday."

- SMART Goal: "I will accumulate a $100,000 down payment for a house in my target neighborhood within the next 7 years."

- Vague Wish: "I need to save for retirement."

- SMART Goal: "I will save $1.5 million for retirement by age 65 by contributing 15% of my income to my 401(k) and IRA."

Once you have your goals, categorize them into "needs" (like paying off high-interest debt) and "wants" (like a vacation home). This helps you prioritize and make smart trade-offs.

Conduct a Thorough Financial Assessment

With your goals defined, it's time to take a snapshot of your current financial situation.

- Calculate Your Net Worth: This is your financial starting line. Simply subtract your liabilities (what you owe) from your assets (what you own).

- Assets: Cash, savings accounts, investment balances, retirement accounts, home equity, vehicles.

- Liabilities: Mortgages, car loans, student loans, credit card debt.

- Analyze Your Cash Flow: Track your income and expenses for a couple of months to see where your money is actually going. This exercise almost always reveals opportunities to save more or cut back on non-essential spending.

- Review Existing Resources: Look at your current financial products. Do you have adequate life or disability insurance? Are you taking full advantage of your employee benefits, like a 401(k) match? Understanding what you already have helps you identify gaps.

Step 2: Building Your Comprehensive Financial Plan

This is where you design the strategies to bring your goals to life. A comprehensive plan has several interconnected components that all work together.

Retirement Planning

For most people, this is the cornerstone of long-term planning. The goal is to grow a nest egg that can support you when you stop working. Key tools include:

- 401(k)s: Employer-sponsored plans that often come with a valuable company match. Always contribute enough to get the full match—it's free money.

- IRAs (Traditional vs. Roth): Individual Retirement Accounts that offer tax advantages. A Traditional IRA may give you a tax deduction now, while a Roth IRA provides tax-free withdrawals in retirement.

These limits are adjusted annually for inflation. For example, here are the 2024 limits. For those 50 and older, "catch-up" contributions allow you to save even more.

| Account Type | 2024 Contribution Limit | Age 50+ Catch-Up |

|---|---|---|

| 401(k), 403(b), etc. | $23,000 | $7,500 |

| Traditional & Roth IRA | $7,000 | $1,000 |

Source: Internal Revenue Service (IRS)

Once you've established your retirement accounts, the next step is defining a strategy for the money inside them.

Investment Strategy

Investing is how you put your money to work to outpace inflation. A core principle is asset allocation—dividing your portfolio among different asset classes like stocks, bonds, and cash based on your time horizon and risk tolerance. Diversification, or spreading your money across various investments within those classes, helps reduce risk.

This isn't about picking winning stocks. It's about building a balanced portfolio designed for steady, long-term growth.

While growing your assets is crucial, managing liabilities like high-interest debt is just as important for your plan's success.

Debt Management

High-interest debt can sabotage even the best financial plan. The Consumer Financial Protection Bureau outlines two popular strategies for paying it down:

- The Avalanche Method: You focus on paying off the debt with the highest interest rate first. This approach saves you the most money in interest over time.

- The Snowball Method: You focus on paying off the smallest debt balance first, regardless of the interest rate. This method can provide powerful psychological wins, building momentum and motivation.

Beyond growing assets and reducing debt, a durable plan must also protect you from the unexpected.

Risk Management and Insurance

A solid plan includes a safety net to protect you from the unexpected. This starts with an emergency fund containing 3-6 months' worth of essential living expenses. It prevents you from derailing your goals or going into debt for a surprise cost, like a major car repair.

Beyond cash reserves, insurance is also crucial. Life and disability policies protect your family and your income if something happens to you.

Finally, a truly comprehensive plan considers what happens beyond your own lifetime.

Estate and Legacy Planning

Estate planning isn't just for the wealthy. It's about ensuring your assets are distributed according to your wishes and your loved ones are cared for. Basic components include a will, trusts, and power of attorney. For business owners, this also involves succession planning to ensure a smooth transition for the company you've built.Integrating these different elements is complex, which is why working with a financial professional can provide clarity and confidence.

Step 3: Implementing and Automating Your Strategy

A financial plan is only a document until you put it into action. The most effective way to ensure you stay on track is to automate the process.

Automate Your Contributions Set up recurring transfers from your checking account to your savings, investment, and retirement accounts. This "pay yourself first" approach removes willpower from the equation and turns saving into a consistent habit. Key benefits include:

- Building discipline by making saving non-negotiable.

- Ensuring consistency in funding your long-term goals.

- Reducing the temptation to spend money earmarked for the future.

Once your savings are automated, the next step is to simplify your existing accounts.

Consolidate and Simplify If you have old 401(k)s from previous jobs or multiple scattered investment accounts, consolidating them can make your portfolio much easier to manage. The advantages are clear:

- Clearer oversight of your overall asset allocation.

- Simplified paperwork with fewer statements to track.

- Potentially lower fees by moving out of expensive legacy plans.

This process, known as a rollover, can have tax implications, so it’s often best to work with a financial advisor to ensure it’s done correctly.

Step 4: Monitoring Your Plan and Adapting to Life's Changes

Your financial plan should evolve with you. Schedule time to review it—a comprehensive check-in annually and a quick look quarterly is a good cadence.

More importantly, certain life events should always trigger a plan review. These milestones can significantly impact your goals, income, and expenses.

- Marriage or divorce

- Birth or adoption of a child

- A significant change in income (a raise, promotion, or job loss)

- Changing jobs or starting a business

- Receiving a significant gift or inheritance

Beyond these major life events, proactive plan maintenance is also essential. This includes rebalancing your investment portfolio. Market movements can cause your asset allocation to drift from your original targets. Rebalancing involves periodically selling assets that have performed well and buying more of those that have lagged to bring your portfolio back into alignment.

This disciplined process of reviewing and adapting is crucial for long-term success and is a primary reason why an ongoing partnership with a financial advisor can be so valuable.

Partnering with a Professional for Your Financial Journey

While a DIY approach to financial planning is possible, the complexity can be overwhelming. A financial professional provides expertise, discipline, and an objective perspective, especially when navigating major life transitions, nearing retirement, or managing the unique finances of a business.

When seeking guidance, look for professionals with credentials like CFP® (Certified Financial Planner) or CFA® (Chartered Financial Analyst). These designations indicate a high level of education, experience, and ethical commitment.

At Endeavor Financial Group, we are fee-only fiduciaries, legally obligated to act in your best interest. Our compensation comes directly from clients, not product commissions. This model removes conflicts of interest, ensuring our advice is always aligned with your goals.

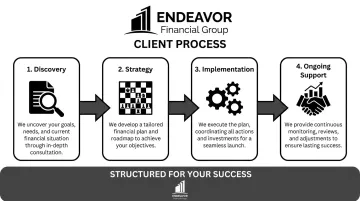

We use a structured, four-step process to build a clear roadmap tailored to your life:

- Discovery: We start by listening. Our first meeting is dedicated to understanding your goals, priorities, and concerns to ensure we are the right fit.

- Strategy: Our team develops a personalized plan with short-, intermediate-, and long-term strategies designed to work in harmony.

- Implementation: We provide an easy-to-follow roadmap, guiding you through every step from investment decisions to estate plans.

- Ongoing Support: As your life evolves, so should your plan. We conduct regular reviews and make adjustments to keep you on track toward your financial goals.

If you're ready to build confidence in your financial future, we invite you to schedule a consultation with our team.

Frequently Asked Questions

What is the 50/30/20 rule in your financial plan?

It's a popular budgeting guideline where 50% of your after-tax income goes to needs (housing, utilities), 30% to wants (dining out, hobbies), and 20% to savings and debt repayment. It was popularized by Elizabeth Warren and Amelia Warren Tyagi in their book, All Your Worth.

What's the smartest thing to do with $100,000?

This depends on your goals, but common strategies include paying off high-interest debt, maxing out retirement accounts, investing in a diversified portfolio, or funding a major purchase like a home.

What is the average net worth of a 70-year-old couple?

The Federal Reserve's 2022 data shows a median net worth of $409,900 for households aged 65-74. However, this is just a benchmark; what matters is having enough to support your unique retirement goals.

How often should I review my long-term financial plan?

You should review your plan at least annually. It's also critical to revisit it after any major life event—like a marriage, new child, or job change—to ensure it still aligns with your goals.

What is the difference between financial planning and investment management?

Investment management focuses only on growing your assets. Comprehensive financial planning is a more holistic process that includes investment management plus goal setting, budgeting, tax strategy, and estate planning.