This guide is designed to cut through the noise. We'll provide a clear, comprehensive roadmap to understanding your equity compensation, helping you create a strategic plan to maximize its value and align it with your personal financial goals.

TL;DR: Key Takeaways on Equity Compensation

- Equity compensation includes stock options (ISOs/NSOs) and restricted stock (RSUs/RSAs), each with unique tax rules.

- Taxable events occur at different times (vesting, exercise, sale), requiring careful planning to manage income and capital gains tax.

- A strategic plan is essential to manage concentration risk and align your equity with long-term goals like retirement or major purchases.

- Working with a financial professional can help you navigate vesting schedules, tax implications, and diversification strategies.

What is Equity Compensation and Why Is It Important?

Equity compensation is non-cash pay that gives you an ownership stake in the company you work for. From an employer's perspective, it’s a strategic tool used to attract and retain top talent. By making employees part-owners, companies align individual interests with long-term company performance. When the company thrives, so do its employees.

For employees, the benefits are substantial:

- Offers potential for financial growth that can far exceed a traditional salary, especially if the company's stock value appreciates.

- Fosters a sense of ownership, creating a deeper connection to the company's mission and success.

- Directly rewards your contributions, as your hard work can influence the value of your compensation.

It's a popular and effective tool. According to a 2024 study from Morgan Stanley at Work, 76% of HR leaders report their companies offer equity compensation. It's also a powerful retention tool, with 56% of participants in a Fidelity survey saying their stock plan makes them more likely to stay at their job.

The Common Types of Equity Compensation Explained

Equity compensation comes in several forms, each with unique rules and tax implications. Understanding the key differences is the first step toward making informed decisions.

Stock Options

Stock options give you the right, but not the obligation, to buy a set number of company shares at a predetermined price, known as the "grant" or "strike price." The value comes from the "spread"—the difference between the strike price and the market price when you exercise the option.

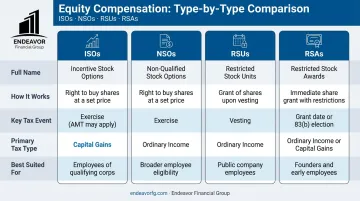

- Incentive Stock Options (ISOs): These are often preferred for their tax advantages. If you meet specific holding period requirements (typically holding the stock for at least two years from the grant date and one year from the exercise date), your profit is taxed at the more favorable long-term capital gains rate.

- Non-Qualified Stock Options (NSOs or NQSOs): These are more common. When you exercise NSOs, the spread between the strike price and the market price is taxed as ordinary income for that year. Any subsequent growth in value is then treated as a capital gain when you sell the shares.

Restricted Stock

Unlike options, restricted stock involves receiving actual company shares. These shares are granted to you but are subject to a vesting schedule, meaning you don't fully own them until you've met certain conditions, usually based on time or performance milestones.

- Restricted Stock Units (RSUs): An RSU is your employer's promise to give you company shares in the future, once vesting is complete. You don't pay anything for the shares. Upon vesting, the total value of the shares is taxed as ordinary income.

- Restricted Stock Awards (RSAs): With an RSA, you receive the actual shares on the grant date. While you often have voting rights immediately, the stock is still restricted by a vesting schedule. A key feature of RSAs is the ability to make an 83(b) election, a strategic tax decision we'll cover shortly.

Other Common Forms of Equity

While options and restricted stock are the most common, you might also encounter:

- Employee Stock Purchase Plans (ESPPs): These plans allow you to purchase company stock, often at a discount of up to 15%, through convenient payroll deductions.

- Stock Appreciation Rights (SARs): A SAR gives you the right to the profit from an increase in the company's stock value over a set period. This is typically paid in cash or stock, so you never have to purchase the underlying shares.

Navigating the Tax Maze of Equity Compensation

Taxes are can be the most complex part of managing equity compensation. Each type of award is taxed differently, and the timing of those taxes can have a major impact on your net worth. The key is to understand the taxable events: grant, vesting, exercise, and sale.

Here’s a breakdown of how the most common types are taxed, according to guidelines from the IRS:

- RSUs: Taxed as ordinary income on the full market value at vesting, not at grant. Employers typically withhold shares to cover the tax liability.

- NSOs: Taxed as ordinary income on the spread between the market price and your strike price when exercised. There is no tax at the time of grant.

- ISOs: No regular tax is due at grant or exercise, but the spread can trigger the Alternative Minimum Tax (AMT). Gains are taxed as long-term capital gains at sale if holding requirements are met.

The 83(b) Election: A Strategic Tax Decision

If you receive Restricted Stock Awards (RSAs), you have a unique and time-sensitive opportunity: the 83(b) election. This IRS provision allows you to pay ordinary income tax on the total fair market value of your stock at the time of grant, rather than waiting until the shares vest.

Why would you do this? If you believe the stock's value will increase significantly, making an 83(b) election can be a powerful strategy. You pay tax on a much lower value upfront. Then, all future appreciation is taxed as a capital gain (potentially long-term) when you eventually sell.

What's the risk? You have to file the election within 30 days of the grant date. If you leave the company before your shares vest, you forfeit the stock and you don't get a refund for the taxes you already paid. It's a high-risk, high-reward decision best made with professional guidance, as an advisor can help you model the potential outcomes.

Creating Your Strategic Equity Compensation Plan

Your equity awards shouldn't be managed in a vacuum. They are a powerful component of your overall financial picture and should be integrated into a holistic plan.

Step 1: Align Equity with Your Financial Goals

Start by defining what you want to achieve. Are you saving for a down payment on a house in three years? Funding a child's college education in ten? Planning for retirement in twenty? Map your vesting schedule against these timelines. Knowing when you’ll have access to the shares—and potential cash—allows you to earmark specific grants for specific goals.

Step 2: Manage Concentration Risk

Concentration risk is the danger of having too much of your net worth tied up in a single asset. While it’s exciting to own a large stake in your company, it exposes you to significant volatility. Financial planners often consider a position concentrated if it represents more than 5% of your total portfolio.

A core part of your strategy should be diversification. This doesn't necessarily mean selling everything at once. Common strategies include:

- Establishing a systematic selling plan to gradually sell a portion of shares after each vesting date.

- Using the proceeds from sold shares to invest in a diversified portfolio of stocks, bonds, and other assets.

- For executives, using a Rule 10b5-1 plan to set up a pre-scheduled trading plan.

Step 3: Develop a Hold vs. Sell Framework

Deciding whether to hold or sell vested shares is a personal decision with no single right answer. To build your framework, ask yourself these questions:

- What is my confidence in the company's long-term future? Do you see continued growth potential?

- Do I have immediate or short-term cash needs? A planned sale can fund a major purchase without taking on debt.

- How does this stock fit into my overall asset allocation? Are you over-exposed?

- What are the tax implications of selling now versus later?

Answering these questions honestly will help you move from emotional reactions to strategic decisions.

Step 4: Work with a Financial Professional

Navigating these decisions requires a blend of expertise in investment management, tax planning, and risk assessment. The rules are complex, the stakes are high, and a misstep can be costly.

A firm like Endeavor Financial Group can help you navigate these complexities. As fee-only fiduciaries, we are legally bound to act in your best interest, ensuring our advice is always unbiased.

We use a structured, five-step process to build a personalized roadmap that integrates your equity compensation into a comprehensive wealth plan. Our goal is to ensure every decision supports your long-term financial success.

Key Terms and Common Risks to Understand

To effectively manage your equity, you need to speak the language. Here are a few critical terms and risks to keep on your radar.

- Vesting Schedule: The timeline dictating when you earn full ownership of your shares. Common types are cliff vesting (100% ownership on one date) and graded vesting (ownership in increments over time).

- Blackout Periods and Trading Windows: These are restricted periods, usually around earnings reports, when employees cannot trade company stock to avoid any appearance of insider trading. You can only trade during an open "trading window."

- Major Life & Corporate Events: Events like an IPO, acquisition, or leaving your job can significantly affect your equity. Your plan documents outline the rules for these scenarios, such as forfeiting unvested shares or having a limited window (e.g., 90 days) to exercise vested options.

Frequently Asked Questions

What are the different types of equity compensation?

The main types are stock options (ISOs and NSOs), which give you the right to buy stock at a set price, and restricted stock (RSUs and RSAs), which are grants of company shares that you own after a vesting period. Other forms include ESPPs and SARs.

Are ISOs better than RSUs for equity compensation?

It depends on your financial goals. ISOs may offer tax advantages but come with risks like the Alternative Minimum Tax (AMT). RSUs provide more certainty, as they hold value as long as the stock price is above zero.

What does 20% equity mean in an equity compensation package?

This typically means you have the right to own a percentage of the company's total shares through options or grants. The actual dollar value depends entirely on the company's valuation at the time you sell or exercise, which can change dramatically.

What is a vesting schedule?

A vesting schedule is the timeline over which you earn the right to your equity awards. Until you are "vested," you don't fully own the shares or options, and you could forfeit them if you leave the company.

What is concentration risk in equity compensation?

This is the risk of having too much of your net worth tied up in a single company's stock. It makes your financial well-being overly dependent on that one stock's performance, which can be highly volatile.

Should I sell my company stock as soon as it vests?

While every situation is unique, many advisors suggest selling a portion of vested shares to diversify and reduce concentration risk. The right strategy depends on your financial goals, tax situation, and confidence in the company.