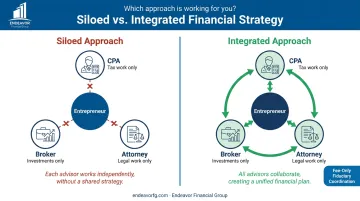

Many business owners make the costly mistake of handling their finances in silos. They have a CPA for taxes, a broker for investments, and an attorney for estate planning, with these professionals rarely, if ever, speaking to one another. This disconnected approach creates gaps, inefficiencies, and missed opportunities that can silently erode wealth over time.

This guide provides a roadmap for breaking down those silos. We'll explore how to integrate your tax, investment, and estate strategies into a single, powerful financial plan designed for the unique journey of a business owner.

TL;DR: Key Integrated Strategies for Entrepreneurs

- Choose a business structure (LLC, S-Corp) that aligns tax, liability, and estate goals.

- Leverage SEP IRAs and Solo 401(k)s to cut taxes and build personal wealth.

- Mitigate risk by diversifying investments outside your business as a financial safety net.

- Implement buy-sell agreements and trusts to protect your business, partners, and family.

- Integrate tax, investment, and estate strategies for effective long-term wealth creation.

Why Entrepreneurs Need an Integrated Financial Strategy

An integrated financial strategy creates synergy, where the combined effect of your financial decisions is greater than the sum of its parts. This approach ensures all your financial components work in concert, much like a high-performance engine. A siloed strategy, in contrast, is like building that engine with mismatched parts—even quality components fail when they aren't designed to work together.

A disconnected approach creates significant risks. For instance, imagine your investment advisor executes an aggressive strategy that generates significant short-term capital gains. Without coordinating with your tax advisor, you could face a massive, unexpected tax bill at the end of the year, wiping out a chunk of your returns.

When all the pieces work in concert, the benefits are clear:

- Minimize your overall tax burden by structuring investment and estate planning decisions together.

- Manage personal and business risks cohesively to protect your company, assets, and family.

- Create a seamless succession plan by aligning your business exit, retirement, and legacy goals.

Core Pillar 1: Foundational Tax & Business Structure Strategies

Your business structure is the bedrock of your financial plan. It dictates how you're taxed, the level of liability you assume, and how you can build and transfer wealth.

Choosing the Right Business Entity

The choice between a Sole Proprietorship, LLC, S-Corporation, or C-Corporation has profound financial implications. While a Sole Proprietorship is simple, it offers no liability protection, putting your personal assets at risk. An LLC provides a liability shield, but by default, a single-member LLC is taxed just like a sole proprietorship.

For many profitable service-based businesses, electing for an LLC to be taxed as an S-Corp can be a powerful move. It allows you to pay yourself a "reasonable salary" subject to self-employment taxes, while any additional profits can be distributed as dividends, which are not. This can lead to significant tax savings.

C-Corporations, on the other hand, face double taxation but open the door to advanced strategies like Qualified Small Business Stock (QSBS), which can offer substantial tax benefits upon exit.

Maximizing Tax-Advantaged Retirement Savings

Retirement plans are one of the most powerful tools for entrepreneurs. They allow you to reduce your current taxable business income while simultaneously building a personal, tax-deferred nest egg. Yet, many business owners aren't taking full advantage. A study from the Transamerica Institute found that only 31% of self-employed individuals were saving in a Traditional or Roth IRA.

Two popular options for business owners are:

- SEP IRA: Simple to set up and allows for significant employer-only contributions (up to 25% of compensation, not to exceed $69,000 in 2024). It's a great option for businesses with few or no employees.

- Solo 401(k): More flexible, allowing contributions as both the "employee" and "employer." This structure enables you to contribute more at lower income levels and may also permit plan loans and a Roth contribution option, which a SEP IRA does not.

Leveraging Business Deductions

Meticulous bookkeeping is non-negotiable for maximizing tax efficiency. Many entrepreneurs overlook or underutilize legitimate business deductions that can significantly reduce their taxable income. Common examples include:

- The home office deduction

- Vehicle expenses, using either the standard mileage rate or actual costs

- Health insurance premiums for yourself and your family

- Costs of business-related travel and education

Core Pillar 2: Strategic Investment Planning Beyond Your Business

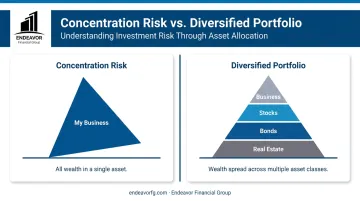

For most entrepreneurs, their business is their single largest asset. While this creates incredible potential for wealth, it also creates a significant vulnerability: concentration risk.

The Critical Need for Diversification

FINRA defines concentration risk as the risk of amplified losses that may result from having a large portion of your holdings in a particular investment. When your income, net worth, and future exit are all tied to one company, your entire financial well-being is exposed to the fortunes of that single entity.

Your personal investment portfolio should be designed to complement, not mirror, the high-risk, high-growth nature of your business. The goal is to systematically move profits from the business into a diversified portfolio of stocks, bonds, and other assets. This strategy builds a financial safety net that is insulated from your company's day-to-day volatility.

Tax-Efficient Investing

A successful investment strategy isn't just about what you earn; it's about what you keep after taxes. Integrating your investment and tax planning is essential to maximizing your real returns.

Two key strategies include:

- Placing tax-inefficient assets, like corporate bonds or funds with high turnover, inside tax-advantaged accounts while keeping tax-efficient assets like index funds in taxable accounts.

- Selling investments at a loss to strategically offset capital gains taxes from other profitable investments, turning a market downturn into a tax-saving opportunity.

Beyond tax efficiency, your investment strategy should also directly support your long-term vision for the business itself.

Aligning Your Investments with Your Business Exit Plan

Think of your personal investment portfolio as your "freedom fund." Every dollar you save and invest outside the business reduces your dependence on a successful exit, giving you more options. It means you can sell when the time is right, not because you're forced to by financial circumstances.

Whether your goal is to sell to a third party, pass the business to the next generation, or simply wind it down, having a strong personal balance sheet puts you in control of your own timeline.

Core Pillar 3: Proactive Estate Planning to Protect Your Legacy

For an entrepreneur, estate planning is not just about personal assets; it's about ensuring the continuity and survival of the business you've worked so hard to build.

The Buy-Sell Agreement: Your Business's "Prenup"

If you have partners, a buy-sell agreement is one of the most important legal documents you can create. It's a binding contract that dictates what happens if an owner needs to leave the business. It provides a clear roadmap for handling the "5 D's":

- Death

- Disability

- Divorce

- Departure (voluntary)

- Disqualification (involuntary)

A well-drafted buy-sell agreement sets a valuation method for the business and outlines the terms of the buyout, preventing contentious disputes and ensuring a smooth transition. These agreements are often funded with life or disability insurance policies, providing immediate liquidity to buy out a departing owner's share without draining the company's cash reserves.

While a buy-sell agreement prepares the business for an owner's exit, trusts are essential for protecting the assets you've accumulated and managing them for your heirs.

Using Trusts for Asset Protection and Succession

Trusts are a powerful tool for modern estate planning. They can be used to separate your business and personal assets, creating a layer of protection from potential creditors or lawsuits. A Revocable Living Trust is particularly valuable for business owners, as it allows business interests to be transferred to your heirs outside of the public, time-consuming, and often costly probate process. This ensures business operations can continue without interruption after your passing.

Beyond planning for your own transition, it's also critical to protect the business from the unexpected loss of other essential leaders.

Key Person Insurance

What would happen to your business if you or another critical employee were suddenly gone? Key person insurance is a policy a business takes out on a crucial owner or employee. If that person passes away, the company receives the death benefit. This tax-free infusion of cash can be used to:

- Recruit and train a replacement

- Pay down debt

- Reassure lenders and customers

- Fund a buy-sell agreement

This is a vital risk management tool that provides financial stability when the business loses its most important asset—its people. Integrating these legal and insurance strategies into your comprehensive financial plan is key to ensuring your legacy is secure.

Bringing It All Together: A Holistic Approach to Your Wealth

Effectively managing the interconnected pillars of tax, investments, and estate planning requires a coordinated effort and specialized expertise. A piecemeal approach often leads to missed opportunities and costly mistakes, which is why working with a comprehensive financial planning firm is so valuable.

At Endeavor Financial Group, we specialize in providing the integrated financial strategies that entrepreneurs need. We understand that your business and personal finances are deeply intertwined. Unlike asset managers who may only focus on investments, we act as your family's CFO, looking at your entire financial picture to ensure every decision is aligned with your goals.

We use a five-step structured process to build and monitor your holistic financial strategy:

- Discovery: We start by understanding your goals for your business, your family, and your future.

- Analysis: Our team analyzes your complete financial situation to identify opportunities and potential risks.

- Strategy Development: We build a clear, integrated roadmap tailored to your specific needs.

- Implementation: We coordinate with you and your other professionals (like your CPA and attorney) to put the plan into action.

- Monitoring: We regularly review your progress and adjust the plan as your life and business evolve.

This structured process ensures your financial plan becomes a dynamic tool, providing clarity and confidence as you move forward.

Frequently Asked Questions

What are the best tax strategies for LLC owners?

For many LLC owners, electing S-Corp tax status can reduce self-employment taxes on profits. This strategy requires paying yourself a "reasonable salary" while taking remaining profits as distributions, which are not subject to FICA taxes.

What is the best investment strategy to avoid taxes?

The goal is tax efficiency, not tax avoidance. Key strategies include maximizing tax-advantaged retirement accounts, using tax-loss harvesting, and holding investments long-term to qualify for lower capital gains rates.

How does my business structure affect my estate plan?

Your business structure dictates how ownership can be transferred, the potential for estate taxes, and what legal documents are needed. A well-designed plan uses documents like buy-sell agreements to ensure a smooth transition that aligns with your entity type.

What is a buy-sell agreement and why is it crucial for business partners?

It's a binding contract that outlines what happens to a partner's ownership stake if they die, become disabled, or leave the business. It protects the remaining owners and the company by pre-determining a valuation and buyout process.

When is the right time for an entrepreneur to start working with a financial planner?

The ideal time is as early as possible, especially when making foundational decisions like choosing a business entity. That said, it's never too late to get organized and build a cohesive financial strategy for your future.