Ignoring this complexity is a high-stakes gamble. This article provides a clear roadmap for integrating your equity compensation into a long-term financial plan. We'll show you how to turn this valuable but volatile asset into a strategic tool for achieving your most important life goals, from early retirement to funding your next big venture.

Key Takeaways

- Treat equity compensation as an active asset requiring a clear strategy, not a passive windfall.

- Navigate key challenges like concentration risk, complex tax implications, and potential illiquidity.

- Build a solid plan by understanding your specific awards, setting goals, diversifying assets, and optimizing for taxes.

- Use a structured process to avoid costly mistakes like inaction, emotional decisions, and tax surprises.

Why Integrating Equity Compensation is Crucial for Your Financial Future

Failing to plan for your equity compensation is like leaving one of your most significant assets to chance. Because its value is tied directly to your employer's performance, it creates a single point of failure in your financial life.

Your income and a huge chunk of your net worth depend on the same company.

A proactive integration strategy transforms this risk. It turns a volatile asset into predictable fuel for your most ambitious goals, whether that's retiring a decade early, funding a new business, or building generational wealth.

A well-managed equity plan is a strategic investment that builds your future. An unmanaged one is just a lottery ticket.

Understanding the Building Blocks: A Guide to Your Equity Awards

Before you can build a plan, you need to know your materials. Equity awards come in several forms, each with its own rules and tax treatment. Here are the most common types you'll encounter.

Restricted Stock Units (RSUs)

RSUs are a straightforward grant of company shares that you receive after meeting a vesting schedule. Once your RSUs vest, the shares are yours, and their value is taxed as ordinary income in that year. They are simple and have value as long as the company's stock price is above zero.

Stock Options (ISOs vs. NSOs)

Stock options give you the right to buy a set number of company shares at a predetermined price (the "strike price") in the future.

Incentive Stock Options (ISOs) offer potential tax advantages. If you meet key holding requirements—at least one year post-exercise and two years post-grant—your profit may be taxed at lower long-term capital gains rates.

However, exercising ISOs can trigger the Alternative Minimum Tax (AMT), a complex rule that requires careful financial planning.

Non-qualified Stock Options (NSOs) are more common and have simpler tax rules. When you exercise them, the difference between the strike price and the current market price is taxed as ordinary income. Any future growth is then treated as a capital gain when you sell the shares.

Employee Stock Purchase Plans (ESPPs)

ESPPs are a company benefit that allows you to buy company stock at a discount, typically 10-15% off the market price. They are a great way to build an ownership stake over time and can be a valuable part of a broader equity strategy, but they still contribute to concentration risk if left unmanaged.

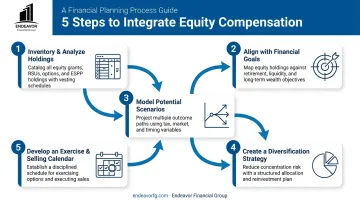

A Step-by-Step Guide to Integrating Equity into Your Financial Plan

Building a strategy for your equity awards doesn't have to be complicated. By following a structured process, you can move from uncertainty to clarity and control.

Inventory and Analyze Your Holdings Get organized by creating a master spreadsheet of all your equity grants. For each one, document the grant date, vesting schedule, number of shares, and strike price for options. This provides a clear picture of what you own and when.

Align Equity with Your Financial Goals Connect your equity to tangible life goals by earmarking specific grants for purposes like a home down payment or college funding. This reframes your shares from an abstract value into an active component of your financial plan.

Model Potential Scenarios Since stock prices are unpredictable, model a few outcomes. Calculate your equity's potential value in best-case, worst-case, and realistic scenarios. This exercise helps you understand the range of possibilities and make rational, not emotional, decisions.

Create a Diversification Strategy Create a written diversification strategy to manage risk by systematically selling vested shares over time. This isn't about timing the market; it's about methodically reducing concentration risk. Base your plan on time (e.g., sell 25% quarterly) or price targets.

Develop an Exercise and Selling Calendar Map everything out on a calendar. Plot vesting dates against your financial milestones and any company restrictions like open trading windows or blackout periods. This creates an actionable roadmap for when to execute your decisions.

Key Strategies for Managing Concentration Risk and Taxes

Once your plan is in place, success hinges on navigating two key hurdles: concentration risk and taxes.

Managing Concentration Risk

Having too many eggs in one basket is the single greatest threat to a financial plan built on equity compensation. While it feels good to have a large stake in a company you believe in, the data shows this is an incredibly risky bet. A landmark study by Hendrik Bessembinder found that historically, four out of every seven common stocks delivered returns lower than one-month Treasury bills over their lifetimes.

The solution is a systematic selling approach. By pre-committing to selling a set percentage of shares at regular intervals—every quarter, for example—you remove emotion from the equation.

You're no longer trying to guess the peak or agonizing over daily price movements. Instead, you are executing a disciplined plan to convert a concentrated position into a diversified portfolio to fund your long-term goals.

Tax Optimization Strategies

Different equity types have vastly different tax treatments, and a misstep can lead to a surprisingly large tax bill.

- RSUs: Taxed as ordinary income when they vest.

- NSOs: Taxed as ordinary income on the "bargain element" (the spread between the market price and your strike price) when you exercise.

- ISOs: Not taxed at exercise for regular tax purposes, but the bargain element can trigger the costly Alternative Minimum Tax (AMT).

A common tax-smart strategy is to sell RSU shares immediately upon vesting. Since they are taxed as income at that moment, selling right away means there is little to no additional capital gain, effectively locking in the value and allowing you to diversify immediately without a second tax hit.

For those with a higher risk tolerance, holding shares for more than a year after acquisition can qualify them for lower long-term capital gains tax rates. However, this strategy re-introduces the very concentration risk you're trying to manage.

For high-net-worth individuals, more advanced strategies exist. For example, donating appreciated shares to a Donor-Advised Fund (DAF) can reduce concentration, provide a current-year tax deduction, and support charitable causes.

Common Mistakes That Can Derail Your Long-Term Goals

The immense value of an equity plan is often lost not to market crashes, but to a few simple and avoidable behavioral mistakes.

Mistake 1: The "Set It and Forget It" Approach

Inaction is the default for many busy professionals. They let vested shares pile up, leading to extreme concentration risk. It's crucial to remember that once shares vest, they are no longer just a "work benefit"—they are a core part of your net worth and must be managed with the same discipline as any other investment.

Mistake 2: Emotional Decision-Making

Company loyalty and market-timing temptations are powerful forces. Phrases like "I'll sell when it goes up just another 10%" or "I can't sell now, it would feel disloyal" are common.

This emotional attachment often leads to holding on too long through a downturn or selling in a panic near the bottom. Survey evidence reveals that only 16% of employees believe their company's stock is riskier than a broad market index—a clear sign of familiarity bias at work.

Mistake 3: Ignoring the Tax Consequences and Trying to Go It Alone

The complexity of equity awards, tax laws, and risk management is easy to underestimate. A surprise six-figure tax bill from an RSU vesting event or an unexpected AMT hit from exercising ISOs can cause immense financial stress and derail your goals.

Trying to navigate these complexities alone is a common mistake. Partnering with a professional can provide the clarity and confidence needed to make sound decisions.

At Endeavor Financial Group, our Certified Financial Planners™ act as fiduciaries, legally bound to act in your best interest. We help you avoid costly errors and integrate your equity into a cohesive financial strategy.

Our consultative process builds a clear, actionable roadmap for your wealth:

- Discovery: We start by getting to know you and understanding your unique goals and priorities.

- Analysis: We take a deep dive into your financial situation to build a preliminary plan tailored to your objectives.

- Implementation: We deliver a clear, easy-to-follow roadmap and help you execute each step.

- Monitoring: As your life changes, we adapt your plan to ensure it always aligns with your evolving priorities.

This structured approach helps you avoid costly mistakes and turn your equity into a true long-term asset.

Frequently Asked Questions

Can equity be a long-term financial instrument?

Yes, but only when it is actively managed. By systematically converting concentrated company stock into a diversified portfolio over time, you can use it to fuel long-term goals rather than holding it indefinitely as a high-risk single-stock position.

What is the difference between RSUs and stock options?

RSUs are a direct grant of shares that you receive after a vesting period. Stock options are the right to buy shares at a fixed price in the future; they only have value if the stock's market price is above your purchase price.

How is equity compensation taxed?

Generally, RSUs and NSOs are taxed as ordinary income when you receive the shares or exercise the options. ISOs have special rules that can provide capital gains treatment but may also trigger the Alternative Minimum Tax (AMT).

What is concentration risk and why is it dangerous?

Concentration risk means having too much of your net worth in a single asset, such as company stock. This is dangerous because a sharp decline in that one asset can jeopardize your entire financial plan, even if other investments do well.

Should I sell my company stock as soon as it vests?

For many people, selling vested shares immediately is a sound strategy to lock in value, manage taxes, and diversify. However, the right choice depends on your personal risk tolerance, overall financial goals, and specific tax situation.

What is a 10b5-1 plan?

A 10b5-1 plan is a pre-arranged trading plan that allows company insiders to sell their shares at predetermined times and prices. It helps automate a diversification strategy and provides an affirmative defense against potential insider trading allegations.