The solution isn’t just about saving a large sum; it’s about converting those savings into a reliable, sustainable income stream. This requires a strategic plan that accounts for everything from your withdrawal rate and tax obligations to inflation and market volatility.

This guide provides a clear framework for building a resilient retirement income plan. We'll walk through the essential steps to create a financial structure that can support you for the long haul, giving you confidence and peace of mind.

Key Takeaways

- A sustainable retirement income plan involves five steps: defining your lifestyle, inventorying income sources, creating a withdrawal strategy, managing risks, and performing regular reviews.

- Your plan's success hinges on key variables like your withdrawal rate, asset allocation, tax strategy, and planning for longevity and rising healthcare costs.

- A common pitfall is relying on a single income source or using a withdrawal strategy that isn’t flexible or tax-efficient.

- The goal is to create a reliable "paycheck" from your assets that lasts throughout your entire retirement, not just to accumulate a lump sum.

The 5 Steps to Creating Your Sustainable Retirement Income Plan

Building a durable income stream for retirement is a structured process. By following these five steps, you can move from a collection of accounts to a coordinated strategy that generates the cash flow you need.

Step 1: Define Your Retirement Vision and Calculate Your Needs

Before you can build a plan, you need to know what you're building for. Start by translating abstract retirement dreams into concrete numbers. Start by estimating your annual expenses, separating them into two categories:

- Essential Costs: Housing, healthcare, food, utilities, transportation, and taxes.

- Discretionary Costs: Travel, hobbies, entertainment, dining out, and gifts.

A common guideline is the 70-85% rule, which suggests you'll need 70% to 85% of your pre-retirement income to maintain your lifestyle. While T. Rowe Price notes 75% is a useful starting point, this is just a benchmark. A personalized budget based on your actual spending habits is far more accurate. Don't forget to factor in potential one-time expenses, like a new car, major home repairs, or helping family.

Step 2: Inventory and Optimize Your Income Sources

Next, create a comprehensive list of every potential income stream you'll have in retirement. Each source has its own rules and optimization strategies.

- Social Security: Your claiming age dramatically impacts your benefits. For those born in 1960 or later, claiming at age 62 provides 70% of your full benefit, while delaying to age 70 provides 124%. This decision can mean a difference of tens of thousands of dollars over your lifetime.

- Pensions: If you have a pension, you'll likely choose between a lump-sum payout or a lifetime annuity. The right choice depends on your health, other income sources, and whether you want to leave money to heirs.

- Retirement Accounts: Your 401(k)s, 403(b)s, and IRAs will likely be the primary engine of your income plan. This is the pool of money you'll draw from using a strategic withdrawal plan.

- Other Sources: Don't overlook other assets, such as rental property income, part-time work, or existing annuities.

Step 3: Design a Strategic Withdrawal Plan

How you pull money from your accounts is just as important as how much you've saved. A withdrawal strategy protects your portfolio while providing predictable income. Two popular methods are the 4% rule and the bucket strategy.

The 4% Rule: This traditional guideline suggests withdrawing 4% of your portfolio's initial value in your first year of retirement, then adjusting that amount for inflation each subsequent year. However, its effectiveness is debated in today's market. Morningstar's research shows the "safe" initial rate fluctuates, estimating it at 3.7% for 2024 based on projected market performance.

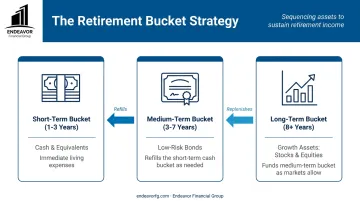

The Bucket Strategy: This method is designed to manage market volatility. You divide your assets into three "buckets":

- Short-Term Bucket (1-3 years of expenses): Held in cash and cash equivalents. This is your immediate income source, so it's not exposed to market risk.

- Medium-Term Bucket (3-7 years of expenses): Invested in low-risk assets like bonds. This bucket is used to refill your cash bucket.

- Long-Term Bucket (8+ years of expenses): Invested in growth assets like stocks. This is the engine of your portfolio, designed to outpace inflation over the long run. By only drawing from the cash bucket, you avoid selling growth assets during a market downturn.

Step 4: Implement a Tax-Efficient Withdrawal Sequence

The order in which you tap your accounts can significantly reduce your tax bill and maximize your after-tax income. The generally recommended sequence is:

- Taxable Brokerage Accounts: These are often tapped first. You'll pay long-term capital gains taxes on appreciated assets, which are typically lower than ordinary income tax rates.

- Tax-Deferred Accounts (Traditional IRAs/401(k)s): Withdrawals from these accounts are taxed as ordinary income. You'll also need to take Required Minimum Distributions (RMDs) starting in your 70s.

- Tax-Free Accounts (Roth IRAs/401(k)s): These are usually last. Qualified withdrawals are completely tax-free, and Roth IRAs have no RMDs for the original owner, allowing them to grow untouched for longer.

This sequence provides a strong foundation, but advanced strategies like Roth conversions can further optimize your tax situation, especially in the years before RMDs begin.

Step 5: Stress-Test Your Plan Against Key Risks

A solid plan must withstand challenges, not just assume best-case scenarios. Stress-test your strategy against the major risks that can derail retirement—which we cover in detail in the next section.

What You Need Before You Start Planning: Gathering Your Financial Puzzle Pieces

To build an accurate and realistic retirement strategy, you first need to gather all your essential financial documents. This process gives you a complete picture of where you stand today.

Here is a simple checklist to get you started:

- Financial Statements: Collect recent statements from all your accounts, including checking, savings, 401(k)s, IRAs, brokerage accounts, and HSAs.

- Income Information: Download your Social Security benefit estimates from ssa.gov and gather any pension plan documents.

- Debt and Liabilities: Make a list of all outstanding debts—mortgage, car loans, credit cards—along with their interest rates and monthly payments.

- Insurance Policies: Gather summaries of your life, disability, long-term care, and health insurance policies.

With this information in hand, you (and your financial advisor) can build a plan based on a clear and complete picture of your financial life.

Key Factors That Can Impact Your Retirement Income

A sustainable plan must account for external forces and personal circumstances that will inevitably change over a decades-long retirement. Here are the four biggest factors to consider.

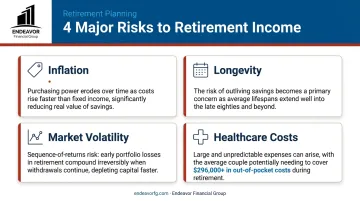

Inflation: The Silent Income Reducer

Inflation is one of the most significant long-term risks because it quietly erodes your purchasing power. An income that feels comfortable today may feel tight in 15 or 20 years. For example, an expense of $50,000 today would require approximately $104,689 in 25 years to cover the same costs, assuming 3% average annual inflation. Your investment strategy, especially your long-term bucket, must be designed to generate returns that outpace inflation to maintain your standard of living.

Longevity: Planning for a Longer Life

People are living longer than ever, which is great news—but it means your money needs to last longer, too. According to the Society of Actuaries, there is a 47% probability that at least one member of a 65-year-old couple will live to age 90.

Planning only for average life expectancy introduces longevity risk—the danger of outliving your assets. This underscores the need for a conservative withdrawal rate and a continued allocation to growth assets well into retirement.

Market Volatility and Sequence of Returns Risk

"Sequence of returns risk" is the danger of experiencing poor market returns in the early years of retirement. When you withdraw from a portfolio during a downturn, you lock in losses and permanently impair its ability to recover.

A U.S. Bank analysis shows that a portfolio suffering a -15% return early in retirement could be depleted in 25 years, while the same portfolio with strong early returns could last 40 years. This is precisely the risk that strategies like the bucket approach are designed to mitigate.

Healthcare and Long-Term Care Costs

Healthcare is one of the largest and most unpredictable expenses in retirement. According to Fidelity, a 65-year-old couple retiring in 2025 can expect to spend an estimated $345,000 on out-of-pocket healthcare costs throughout their retirement. This figure doesn't even include most dental services or the potentially crippling cost of long-term care. A comprehensive plan must account for these expenses to protect your other assets from being wiped out by a major health event.

Common (and Costly) Retirement Income Mistakes to Avoid

Building a solid plan also means sidestepping common pitfalls. Here are a few costly mistakes to avoid:

- Investing too conservatively. Shifting to cash or bonds too early means your portfolio may fail to outpace inflation, effectively reducing your purchasing power over time.

- Ignoring tax implications. Withdrawing funds without a clear strategy can trigger high tax bills, forcing you to draw down your portfolio much faster than planned.

- Underestimating healthcare costs. Medicare won't cover everything. It's essential to plan ahead for supplemental insurance, prescriptions, and potential long-term care.

Keeping Your Plan on Track: The Importance of Regular Reviews

A retirement income plan is not a "set it and forget it" document. It's a living strategy that requires ongoing monitoring and adjustments to stay aligned with your life and the markets.

We recommend an annual review with your financial advisor to assess key areas:

- Performance: Is your portfolio generating the returns needed to support your withdrawals?

- Spending: Have your expenses changed? Is your spending still in line with the plan?

- Life Events: Have you experienced major life changes, like health issues or family events, that require a plan update?

This regular check-in ensures your strategy remains relevant and effective. While you can monitor these areas yourself, partnering with a financial professional provides an objective perspective and expert guidance.

How a Fiduciary Partner Helps You Stay on Track

Retirement income planning is complex, and handling it alone can be daunting. Professional guidance from a fee-only fiduciary can help you build a durable, tax-efficient strategy tailored to your specific goals.

At Endeavor Financial Group, we specialize in helping pre-retirees and business owners create sustainable income plans. Our consultative approach is built on a structured five-step process:

- Discovery: We start by getting to know you and your goals on a personal level.

- Analysis: We conduct a thorough analysis of your complete financial picture to identify opportunities and potential challenges.

- Strategy: We design a personalized, comprehensive plan that addresses everything from investments to taxes and estate coordination.

- Implementation: We guide you step-by-step to ensure every component of your plan is put into action correctly.

- Ongoing Monitoring: We meet with you regularly to review your plan, making adjustments as your life and the markets change.

This process ensures you have a clear roadmap to financial freedom. If you’re ready to build a retirement income plan with confidence, schedule a consultation with our team today.

Frequently Asked Questions

What is a sustainable retirement withdrawal rate?

While the 4% rule is a common benchmark, a truly sustainable rate is personalized. It depends on your age, portfolio, and market conditions, but many advisors now recommend a more dynamic rate, often between 3.3% and 4.5%.

How can I protect my retirement income from inflation?

The best protection is a diversified portfolio with an allocation to growth assets like stocks, which have historically outpaced inflation. Treasury Inflation-Protected Securities (TIPS) can also play a role in a balanced strategy.

What are the main sources of guaranteed income in retirement?

The primary sources are Social Security, pensions, and certain types of annuities. These provide a predictable income floor, reducing your reliance on volatile market-based assets for essential expenses.

How do taxes affect my retirement income withdrawals?

Withdrawals from pre-tax accounts like Traditional IRAs are taxed as ordinary income, while qualified Roth withdrawals are tax-free. A strategic plan minimizes your overall tax burden by sequencing withdrawals from different account types.

When is the best time to start taking Social Security?

There's no single "best" time, as it depends on your health, longevity expectations, and other income. Delaying until age 70 maximizes your monthly benefit, but the optimal age is different for everyone.

Do I need a financial advisor to create a retirement income plan?

While not required, a fiduciary advisor can be invaluable for optimizing taxes and navigating complex Social Security or pension decisions. Their disciplined guidance helps ensure your plan stays on track through changing market conditions.