Most standard retirement advice simply doesn't account for the realities of being a lawyer. You face hurdles like high student debt, irregular income streams from bonuses or contingency fees, a significant tax burden, and a compressed timeline for your peak earnings. These factors demand a more specialized approach.

This guide breaks down the foundational and advanced investment strategies tailored specifically for legal professionals. We'll provide a clear roadmap to help you navigate these complexities and build a secure financial future.

A Quick Summary of Key Strategies

- Address Your Unique Challenges First: Create a custom plan for irregular income, high debt, and complex tax situations.

- Master the Core Accounts: Maximize your 401(k) match or choose a SEP IRA/Solo 401(k) if you are a partner.

- Leverage Advanced Plans: Use Cash Balance Plans in peak years to save over $100,000 annually and lower taxable income.

- Invest Strategically: Align portfolio risk with your career stability and diversify into tax-efficient assets.

- Seek Expert Guidance: Partner with a financial professional who understands the unique complexities of a lawyer's finances.

Why Retirement Planning is Uniquely Complex for Lawyers

Retirement planning for lawyers involves navigating financial hurdles unique to the profession. Your path to building wealth isn't a straight line—it's shaped by several key factors that demand a specialized approach.

Irregular Income & Cash Flow

Unlike a corporate executive with a predictable annual salary, many lawyers experience significant income fluctuations. This is especially true for:

- Contingency-fee litigators, whose income arrives in large, unpredictable sums.

- Solo practitioners, whose revenue can vary month to month.

- Firm partners, whose compensation often depends on annual distributions and bonuses.

This "lumpy" cash flow makes maintaining a consistent savings rate—a cornerstone of traditional retirement planning—extremely difficult. You need a more dynamic strategy that capitalizes on high-income years without derailing your plan during leaner ones.

This challenge is compounded by the famously bimodal salary distribution for lawyers. NALP data shows salaries clustering around $55,000-$100,000 on one end and over $225,000 on the other, highlighting the profession's vastly different financial paths.

Significant Student Loan Debt

The cost of a legal education is a major financial drag that can delay the start of aggressive retirement saving. According to the American Bar Association, the average law school graduate carries $108,000 in student debt, a figure that can take years to pay down.

This delay shortens your compounding period—the time your money has to grow on its own. Every year spent paying down debt instead of investing is a year you lose the powerful effect of compound returns, making it crucial to catch up once you're on solid ground.

The High Tax Burden

As a high-income professional, you face a substantial tax burden that can significantly reduce your take-home pay. With top federal tax brackets reaching 37% for the highest earners, a large portion of your income goes to the IRS before you ever have a chance to save or invest it. This makes tax-advantaged retirement accounts not just a good idea, but an absolute necessity for effective wealth building.

Building Your Foundation: Core Retirement Accounts for Lawyers

Before exploring advanced options, every lawyer needs a solid foundation built on the right core retirement accounts. The best choice depends on your employment structure.

For Lawyers Employed by a Firm

If you work for a law firm, your first stop is the company-sponsored retirement plan.

- Maximize Your 401(k): Your firm's 401(k) is your most powerful tool. Start by contributing enough to get the full employer match—it's free money you can't afford to leave on the table. After that, aim to hit the maximum annual employee contribution limit, which is $23,000 for 2024.

- Utilize the Backdoor Roth IRA: High-earning lawyers often exceed the income limits for direct Roth IRA contributions (for 2024, the phase-out for single filers is $146,000-$161,000). A Backdoor Roth IRA is a strategy to bypass these limits by contributing to a Traditional IRA and then converting it to a Roth, securing tax-free growth.

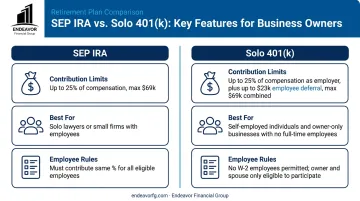

For Solo Practitioners and Small Firm Partners

If you're self-employed or a partner in a small firm, you have more control and can choose from more powerful options.

- SEP IRA (Simplified Employee Pension): This plan is easy to set up and allows for high contribution limits—up to 25% of your compensation, with a maximum of $69,000 for 2024. It's a great, straightforward option. However, if you have employees, you must contribute the same percentage of salary for them as you do for yourself, which can become expensive.

- Solo 401(k): A Solo 401(k) is often the best choice for a solo practitioner or a lawyer whose only employee is a spouse. It allows you to contribute as both the "employee" (up to $23,000 in 2024) and the "employer" (up to 25% of compensation). This dual structure allows for a higher potential contribution, with a combined limit of $69,000 for 2024.

Ultimately, the Solo 401(k) offers the highest potential savings for a solo lawyer. In contrast, the SEP IRA provides a simple, effective solution for small firms with employees.

Leveling Up: Advanced Retirement Strategies for High-Income Lawyers

Once you've maxed out your foundational accounts, it's time to explore advanced strategies. These are designed for established partners and successful solo practitioners in their peak earning years who want to accelerate savings and get serious about tax reduction.

The Game-Changer: Cash Balance & Defined Benefit Plans

Think of these plans as a super-charged pension you create for yourself. A Cash Balance Plan is a type of defined benefit plan that allows you to save far more than the standard 401(k) limits. For many lawyers, this means contributing well over $100,000 or even $200,000 per year.

Here’s how it works:

- Contributions are made by the firm and are 100% tax-deductible.

- This drastically lowers the owner's taxable income for the year.

- The amount you can contribute is determined by an actuary based on factors like your age, income, and retirement goals.

For example, a 50-year-old law firm partner earning $700,000 could potentially contribute over $150,000 pre-tax into a cash balance plan. In a 37% federal tax bracket, that single contribution could save them over $55,000 in federal taxes in one year alone.

Strategic Tax-Efficiency in Your Investment Portfolio

Effective tax planning goes beyond just your retirement accounts. The investments you hold in your taxable brokerage accounts also need a smart strategy.

- Tax-Loss Harvesting: Sell investments at a loss to offset capital gains from winning investments, lowering your overall tax bill.

- Municipal Bonds: Generate federally tax-exempt income, which often provides a better after-tax return than corporate bonds for high earners.

- Asset Location: Place tax-inefficient, high-growth assets in tax-advantaged accounts (401k, Roth IRA) and tax-efficient assets in taxable accounts.

Crafting Your Investment Portfolio: A Lawyer's Guide to Asset Allocation

Choosing the right accounts is only half the battle. What you invest in inside those accounts is just as important. Your asset allocation—the mix of stocks, bonds, and other investments—should be tailored to your unique professional circumstances.

Balancing Professional Risk with Investment Risk

A lawyer's career stability should directly influence their investment risk tolerance.

For example, a partner at a large, diversified firm with a steady income can likely tolerate more volatility. They might allocate a higher percentage of their portfolio to stocks for greater long-term growth.

Conversely, a contingency-fee litigator with unpredictable income might prefer a more conservative portfolio. A larger allocation to bonds can provide stability during years with lower cash flow.

A Diversified Approach for Long-Term Growth

No matter your risk tolerance, diversification is key. Spreading your investments across various asset classes—such as U.S. and international stocks, bonds, real estate, and alternatives—helps smooth out returns and protect your portfolio from market downturns. This becomes increasingly important as you get closer to retirement and your focus shifts from growth to capital preservation.

Adjusting Your Allocation Over Time

Your investment strategy shouldn't be static. The common approach is to start with a more aggressive, equity-heavy portfolio in your 30s and 40s to maximize growth. As you move into your 50s and 60s, you can gradually shift toward a more conservative, income-focused allocation to protect what you've built. For example, you might move from an 80% stock/20% bond mix to a 60% stock/40% bond mix as retirement nears.

Building Your Roadmap: Why Partnering with a Financial Advisor Matters

The strategies discussed here—from choosing between a SEP IRA and a Solo 401(k) to designing a cash balance plan—involve complex rules and have significant financial consequences. This isn't a DIY project.

At Endeavor Financial Group, we specialize in providing comprehensive financial planning for professionals like you. Working with a CERTIFIED FINANCIAL PLANNER™ (CFP®) or Chartered Financial Analyst® (CFA®) ensures you have an expert who can build a holistic plan tailored to your unique situation. We act as the quarterback for your financial team, coordinating with your accountant and attorney to make sure everyone is working from the same playbook.

Our structured five-step process creates a clear roadmap to financial freedom. We start with discovery and analysis to understand your goals, then move to implementation and ongoing monitoring.

This ensures all aspects of your financial life work together, helping you build a future where practicing law is an option, not an obligation.

To see how we can build a personalized plan for your future, book a meeting with our team today.

Frequently Asked Questions

What investment allocation rules should lawyers use for retirement planning?

There's no single rule, as your allocation should be based on your age, risk tolerance, and career stability. Younger lawyers can often be more aggressive (e.g., 80% stocks), while those nearing retirement should shift to a more conservative mix (e.g., 50-60% stocks) to preserve capital.

What is the best retirement plan for a solo practice lawyer?

The Solo 401(k) is often the best choice. It allows you to contribute as both an "employee" and an "employer," which typically results in a much higher savings potential than a SEP IRA for a business owner with no other employees.

How can lawyers reduce their high tax burden when saving for retirement?

Maximize contributions to pre-tax accounts like 401(k)s and SEP IRAs to lower your taxable income. High earners can also use advanced tools like Cash Balance Plans, which allow for very large, tax-deductible contributions.

What are the biggest retirement planning mistakes lawyers make?

Common errors include starting too late due to student loan debt, investing too conservatively and missing out on growth, and failing to create a cohesive plan that addresses their unique income structure and high tax liability.

How much should a lawyer have saved for retirement?

A common guideline is saving 1x your salary by 30, 3x by 40, and 6x by 50. Because lawyers often have high incomes and start saving later, a personalized analysis with a financial advisor is crucial to define your specific retirement number.