Introduction

Most investors reach for a checkbook when they want to support a cause. It's familiar, simple, and feels generous. But for anyone holding appreciated stock in a taxable brokerage account, writing that check may be the most expensive way to give.

The math is straightforward: selling appreciated stock creates a taxable event, leaving you with less to donate and the charity receiving less than the full value of your investment. Donating those shares directly sidesteps the tax entirely.

Yet despite the clear advantage, this strategy rarely gets acted on. Most investors either don't understand how the mechanics work or underestimate how much they're leaving on the table by defaulting to cash.

What follows breaks down the mechanics, the numbers, and who stands to benefit most — so you can decide whether this strategy belongs in your giving plan.

Key Takeaways

- Donating stock held over one year directly to charity eliminates capital gains tax on the appreciation entirely

- Your deduction equals the stock's full fair market value—not your original purchase price

- Deductions are capped at 30% of AGI, with a 5-year carryforward for excess amounts

- Best suited for pre-retirees, executives with concentrated stock positions, and high-income earners

- Donor-advised funds (DAFs) let you claim the deduction now while deciding which charities to support later

What Is Donating Appreciated Stock?

Appreciated stock is any publicly traded security—individual shares, ETFs, or mutual funds—whose current market value exceeds your original purchase price (cost basis), and which you've held for more than one year.

The core mechanic is simple. Instead of selling the shares and donating the after-tax cash, you transfer the shares directly to the charity or a donor-advised fund. You never trigger a taxable sale. The charity receives the shares at full market value and liquidates them on its own.

The holding period determines the size of your deduction. Here's how the two scenarios compare:

- Held more than one year: You deduct the stock's full fair market value (FMV) — the most tax-efficient outcome

- Held one year or less: Your deduction is limited to your original cost basis, not the appreciated value

That distinction can mean a significant difference in your tax savings, which is why most stock donation strategies focus exclusively on long-term holdings.

Donating appreciated stock is a transfer method, not a separate charitable vehicle. Used correctly, it produces a better tax outcome and a larger charitable impact than donating the equivalent amount in cash.

The Tax Advantages That Make This Strategy Work

Avoiding Capital Gains Tax

When you sell appreciated stock, you owe federal capital gains tax on the gain. For long-term holdings, 2025 federal rates are 0%, 15%, or 20% depending on taxable income. High-income donors also face the 3.8% Net Investment Income Tax (NIIT) if modified AGI exceeds $200,000 (single) or $250,000 (married filing jointly)—pushing the combined federal rate to 23.8%.

Donate the shares directly, and that tax disappears entirely. The gain passes through to a tax-exempt entity that owes nothing on the sale.

Deducting Full Fair Market Value

IRS Publication 526 allows donors to deduct the fair market value of long-term appreciated securities on the transfer date—not the original cost basis. For publicly traded securities, FMV is calculated as the average of the high and low trading prices on the date of transfer.

A donor who paid $10,000 for stock now worth $60,000 claims a $60,000 deduction, not a $10,000 deduction.

Portfolio Rebalancing Without a Tax Hit

Donating an oversized position lets you rebalance without triggering a taxable sale. This is particularly valuable for:

- Pre-retirees with long-held positions that have grown disproportionate in their portfolio

- Executives holding concentrated employer stock who need to reduce single-stock risk

- Investors with legacy positions that have compounded for years

Resetting Your Cost Basis

That rebalancing move pairs naturally with a basis reset. After donating the appreciated shares, you can repurchase the same stock at today's market price—raising your cost basis and reducing future capital gains exposure on any shares you want to hold. The tax implications vary by situation, so run this through your advisor before acting.

Estate Planning Benefit

Removing highly appreciated assets from your estate reduces taxable estate value. For business owners and high-net-worth individuals, this compounds over time—particularly for positions that have built up over decades.

Sell vs. Donate: Seeing the Difference in Real Numbers

The numbers make the case clearly. Take stock with a $15,000 cost basis now worth $50,000, held more than one year — a $35,000 embedded gain. At the 20% long-term capital gains rate plus the 3.8% NIIT, here's how the two paths compare:

| Strategy | Federal Tax on $35,000 Gain | Charitable Deduction | Value Reaching Charity |

|---|---|---|---|

| Sell stock, donate after-tax proceeds | $35,000 × 23.8% = $8,330 | ~$41,670 | $41,670 |

| Donate stock directly | $0 | $50,000 (subject to AGI limits) | $50,000 |

The direct donation route saves the donor $8,330 in federal taxes (before state tax) and sends the charity $8,330 more. That's a 20% larger gift at no additional cost to the donor.

What About Short-Term Holdings?

If the stock was held for less than one year, the deduction is limited to your cost basis—not fair market value. The gain would also be taxed as ordinary income if sold. The tax benefit is substantially reduced, which is why the one-year holding period matters so much. Tracking acquisition dates at the individual lot level — before you decide which shares to donate — is one of the most practical steps you can take to protect that benefit.

IRS Rules and Deduction Limits to Know

Holding Period and Qualified Organizations

Stock must be held more than one year to qualify for the full FMV deduction. The recipient must be a qualified 501(c)(3) organization ; verify eligibility using the IRS Tax Exempt Organization Search. Contributions to private non-operating foundations face a lower 20% AGI limit.

AGI Deduction Limits and Carryforward

Appreciated stock donated to a public charity or DAF is deductible up to 30% of adjusted gross income in the year of the gift, compared to 60% for cash donations. Any excess carries forward for up to five additional tax years.

Example: A donor with $200,000 AGI donates stock worth $80,000. The 30% cap allows a $60,000 deduction this year. The remaining $20,000 carries forward to future years until used.

Documentation Requirements

| Situation | Requirement |

|---|---|

| Any gift of $250+ | Written acknowledgment from the charity |

| Total noncash deductions over $500 | IRS Form 8283 required |

| Non-publicly-traded stock over $5,000 | Qualified appraisal required |

| Publicly traded securities | No appraisal needed—readily available price quotations suffice |

The 2026 Deduction Floor

Under recent tax legislation, itemizers will only be able to deduct charitable gifts that exceed 0.5% of AGI starting in 2026—meaning a donor with $300,000 AGI would face a $1,500 floor before the deduction begins. This provision appears in DAF provider guidance and H.R. 1 (119th Congress), but verify the final enacted language with your tax advisor before year-end 2025 planning.

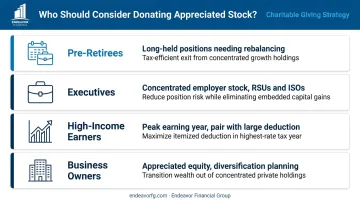

When This Strategy Makes the Most Sense (and When It Doesn't)

Who Benefits Most

- Pre-retirees with long-held positions who need to rebalance before retirement without triggering a large tax bill

- Executives with concentrated employer stock—RSUs, ISOs, and NSOs that have appreciated significantly and created outsized single-stock risk

- High-income earners in a peak earning year who can pair a large deduction with a year of elevated income

- Business owners with appreciated equity planning to diversify regardless

For clients in these situations, Endeavor Financial Group integrates appreciated stock decisions into the full financial plan—alongside equity compensation timing, retirement income sequencing, and estate planning—because each decision affects the others.

When to Skip This Strategy

- Loss positions: If the stock has declined in value, sell it to capture the capital loss deduction, then donate cash instead

- Short-term holdings: Held under one year, the deduction reverts to cost basis—significantly less valuable

- Master limited partnerships (MLPs) and publicly traded partnerships (PTPs): These involve special rules that can reduce the charitable deduction due to ordinary income elements. Consult a tax advisor before donating these

Timing

Donations must be fully completed—shares received by the charity—before December 31 to count in the current tax year. According to Schwab Charitable's year-end guidance, stock transfers from other financial institutions typically take 2 to 6 weeks. Initiating a transfer is not the same as completing it. Donors with large positions should plan well before the December rush.

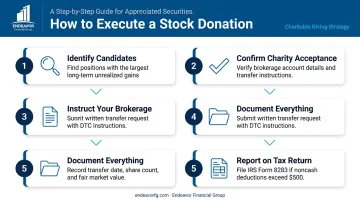

How to Execute a Stock Donation Step by Step

Identify candidates — Look for positions with the largest unrealized gains that have been held more than one year. These are your best candidates for donation versus outright sale.

Confirm the charity can accept securities — Contact the receiving charity or DAF to get their transfer instructions and verify they have a brokerage account set up to receive shares.

Instruct your brokerage in writing — Submit a written transfer request specifying the number of shares, the receiving account, and DTC transfer instructions provided by the charity.

Document everything — Record the transfer date, number of shares transferred, and the fair market value (average of high/low prices on the transfer date) for your tax records.

Report on your tax return — If total noncash deductions exceed $500, file IRS Form 8283 with your return.

The Donor-Advised Fund Route

A DAF is often the most practical option for donors who want flexibility. You transfer appreciated stock to the DAF, claim the full deduction immediately, and then recommend grants to specific charities on your own timeline—no deadline pressure. Most major custodians offer DAF programs.

A DAF is especially useful if you haven't settled on specific organizations yet, or want to spread giving across multiple causes and tax years.

Working With a Financial Advisor

The mechanics of a stock transfer are straightforward. The harder work is identifying which positions to donate, timing the gift against your income, and fitting it into a broader rebalancing or estate plan. Endeavor Financial Group coordinates that process alongside your CPA, connecting the dots across retirement, tax, and estate planning so nothing falls through the cracks.

Frequently Asked Questions

Can I donate appreciated stock that I've held for less than a year?

For stocks held under one year, the deduction is limited to your cost basis—not fair market value—and the gain would be taxed as ordinary income if sold. The tax benefit is substantially smaller. Hold for more than one year to capture the full advantage.

What is the AGI deduction limit for donating appreciated stock?

Appreciated stock donated to a public charity or DAF is deductible up to 30% of AGI in the year of the gift. Any excess carries forward for up to five additional tax years.

Can I donate appreciated stock to a donor-advised fund instead of directly to a charity?

Yes. Contributing appreciated stock to a DAF qualifies for the same benefits—no capital gains tax and a full fair market value deduction—while giving you the flexibility to recommend grants to specific charities at a later date.

Do I owe capital gains tax if I donate appreciated stock instead of selling it?

No capital gains tax is owed when appreciated stock is donated directly to a qualified 501(c)(3). The tax only applies if you sell the shares first, making direct donation the more efficient path for both your deduction and the charity's benefit.

What types of stock can I donate to charity?

Publicly traded stocks, ETFs, bonds, and mutual funds are the most commonly accepted and easiest to transfer. Private company stock, restricted shares, and partnership interests involve additional rules, may require appraisals, and should be reviewed with an advisor before donating.

Can I repurchase the same stock after donating it to charity?

After donating appreciated shares, you can repurchase the same security at the current market price, resetting your cost basis higher and reducing future capital gains exposure. Because a charitable gift isn't a loss sale, wash-sale rules don't apply here. Confirm the specifics with your tax advisor before acting.