In a world where markets feel more connected than ever, it’s a valid concern. The short answer is yes, diversification remains a critical strategy for long-term wealth management. But how we apply it has evolved. This article will explore why this timeless principle is being questioned, reaffirm its core logic, and show you how to build a modern, resilient portfolio that aligns with your goals.

TL;DR: Is Diversification Still Worth It?

- Yes, but it's evolved. While market concentration creates FOMO, diversification is a strategy for managing long-term risk, not chasing short-term highs.

- Its main goal is protection. Diversification aims to smooth out returns and protect against catastrophic losses in a single asset, not to beat the hottest stocks every year.

- Modern portfolios go beyond stocks and bonds. True diversification today often includes alternatives like real estate or commodities to reduce correlation.

- Rebalancing is non-negotiable. Systematically selling winners and buying losers keeps your portfolio aligned with your risk tolerance and goals.

Why Today’s Investors Question Portfolio Diversification

Recent market behavior has understandably made some investors skeptical about spreading their money around. The temptation to concentrate on what’s working is powerful, and several factors are fueling this doubt.

The Challenge of Market Concentration

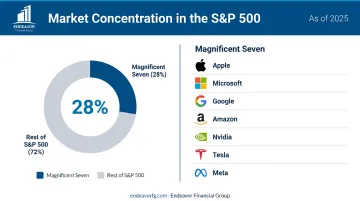

In 2023, the S&P 500's impressive gains were largely powered by a small group of mega-cap tech stocks. The "Magnificent Seven" returned a staggering 75.71%, while the rest of the index looked modest in comparison.

This concentration is significant. As of late 2023, these seven companies made up about 28% of the entire S&P 500, according to BNY Mellon. When such a small slice of the market generates so much of the return, diversified portfolios can feel like they’re underperforming.

Increased Global Correlation

In a globally connected economy, asset classes that once moved independently now sometimes move in lockstep, especially during a crisis. The correlation between U.S. and non-U.S. stocks has been rising for decades. Research from Vanguard shows that the 10-year correlation between them jumped from 0.51 in 1989 to 0.86 by late 2020. When all your assets fall at the same time, the immediate benefit of diversification feels diminished.

The 2022 Stock and Bond Anomaly

For generations, investors relied on high-quality bonds to act as a buffer when stocks fell. But in 2022, that relationship broke down. Both stocks and bonds fell significantly, shaking investor confidence in the traditional 60/40 portfolio. This rare event led many to ask if the old playbook was broken for good.

The Psychology of FOMO

Beyond the data, there's a powerful psychological force at play: the Fear Of Missing Out (FOMO). Seeing concentrated bets on tech stocks generate life-changing wealth on social media makes the slow-and-steady approach of diversification seem boring and ineffective.

This anxiety can push investors to abandon a sound long-term strategy in favor of chasing short-term trends—often at precisely the wrong time.

Although these concerns are valid, they focus on short-term market behavior. The fundamental logic of diversification remains a powerful tool for long-term investors, particularly for managing risk rather than just chasing returns.

The Enduring Logic of Diversification: Managing Risk, Not Chasing Returns

The core idea of diversification is timeless: don't put all your eggs in one basket. It’s not about picking the single best-performing asset each year. It's about spreading your investments across various assets that are unlikely to move in perfect sync, creating a smoother ride over the long term.

The goal is to improve your risk-adjusted returns. This means you’re not just trying to get the highest possible return; you’re trying to get the best possible return for the amount of risk you’re comfortable taking.

How Correlation Works for You

Imagine a simple portfolio. When economic optimism is high, stocks might be soaring (they zig). But if a recession hits, those same stocks may fall. During that fear-driven downturn, investors often flock to the perceived safety of high-quality government bonds, causing their value to rise (they zag).

By owning both, the loss in one part of your portfolio is cushioned by the gain in another.

This is the defensive power of diversification. It’s designed to protect you from catastrophic losses in any single area of the market. No one can consistently predict which asset class will be the top performer. A quick look at a Callan Periodic Table of Investment Returns shows how leadership rotates unpredictably year after year. What wins one year is often in the middle of the pack—or at the bottom—the next.

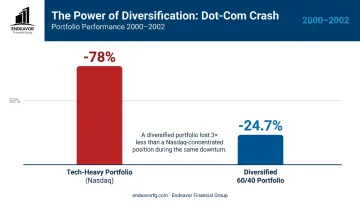

A historical example makes this crystal clear. During the dot-com bubble of the late 1990s, tech stocks seemed invincible. An investor concentrated in the Nasdaq would have felt like a genius. But when the bubble burst, the Nasdaq Composite index fell more than 78% from its peak.

In contrast, a traditional 60/40 balanced portfolio declined by a much more manageable 24.7% during that same period, according to Morningstar. The diversified investor may not have captured the dizzying highs, but they were certainly protected from the devastating lows.

Building a Modern Diversified Portfolio for Your Goals

A modern diversified portfolio today goes beyond a simple mix of U.S. stocks and bonds. It’s about building a sophisticated allocation tailored to your specific goals, timeline, and risk tolerance.

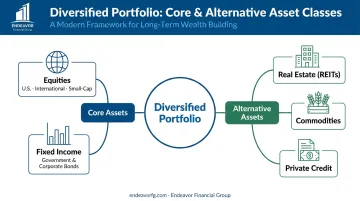

Start with the Core Asset Classes

Every portfolio needs a solid foundation built on traditional assets, each playing a distinct role.

- Equities (Stocks): These are your engine for long-term growth. True stock diversification means looking beyond just the S&P 500. It involves owning a mix of companies based on:

- Geography: U.S., developed international, and emerging markets.

- Company Size: Large-cap, mid-cap, and small-cap companies.

- Style: Growth stocks (focused on future potential) and value stocks (potentially undervalued).

- Fixed Income (Bonds): Bonds provide stability, income, and a buffer against stock market volatility. Diversification here means including:

- Type: Government bonds, corporate bonds, and municipal bonds.

- Duration: A mix of short-term, intermediate-term, and long-term bonds to manage interest rate risk.

Incorporate Modern Diversifiers

To build more resilience, many modern portfolios include "alternative investments." These assets often have a low correlation to public stocks and bonds, meaning they may perform well when traditional markets are struggling.

Examples include:

- Real Estate: Often accessed through Real Estate Investment Trusts (REITs).

- Commodities: Such as gold or oil, which can act as an inflation hedge.

- Private Credit: Loans made directly to companies, offering a different risk-return profile.

The right mix, however, is deeply personal. A pre-retiree focused on capital preservation and income might lean more heavily on bonds and dividend-paying stocks.

In contrast, a business owner with wealth concentrated in their company needs a portfolio that zags when their business zigs, de-risking their overall financial picture.

Designing this kind of sophisticated allocation is where comprehensive financial planning becomes critical. At Endeavor Financial Group, we build strategies that align with your entire financial life—not just the parts a simple asset manager might see.

The Non-Negotiable Step: Consistent Portfolio Rebalancing

Diversification isn't a "set it and forget it" strategy. To maintain its effectiveness, you must practice consistent portfolio rebalancing.

In simple terms, rebalancing is the process of buying or selling assets to bring your portfolio back to its original target allocation.

Let's say you started with a target of 60% stocks and 40% bonds. After a strong year for stocks, your portfolio might drift to 70% stocks and 30% bonds, making it riskier than you originally intended.

Rebalancing forces you to systematically "sell high" by trimming appreciated stocks and "buy low" by using the proceeds to purchase more of the underperforming asset class.

This disciplined process removes emotion from your investment decisions and prevents your portfolio's risk level from creeping up over time. According to guidance from FINRA, there are two common approaches:

- Calendar-based rebalancing involves reviewing your portfolio on a set schedule, such as every six or 12 months.

- Threshold-based rebalancing occurs whenever an asset class drifts from its target by a predetermined amount, like 5% or 10%.

Achieve True Diversification with a Comprehensive Plan

Market trends can make even the most disciplined investors question their strategy. However, diversification remains the most reliable foundation for managing risk and achieving long-term financial goals. It’s not about hitting home runs every year; it’s about consistently getting on base and avoiding strikeouts that take you out of the game.

True diversification is an ongoing process that requires careful planning, thoughtful execution, and disciplined rebalancing. It’s about building a portfolio that reflects your unique life and goals.

At Endeavor Financial Group, we guide our clients through this journey with our five-step structured process. From initial discovery to ongoing monitoring, we design and manage a personalized, diversified portfolio aligned with your goals. Our process creates a clear roadmap, helping you navigate any market environment with clarity and purpose.

Frequently Asked Questions

How much do financial advisors charge to manage your portfolio?

Fee structures vary, but common models include a percentage of assets under management (AUM), often around 1%, or flat annual fees. At Endeavor Financial Group, we use a transparent, fee-only model, ensuring our advice is always in your best interest.

Is a 60/40 portfolio still a good diversification strategy?

The classic 60/40 portfolio's effectiveness varies with market conditions. A modern approach tailors allocations to your specific goals, often including other assets like real estate or alternatives for better resilience.

How many different stocks or funds do I need to be diversified?

There's no magic number. True diversification comes from owning assets with different risk drivers (e.g., sectors, geographies), which is often best achieved with broad-market ETFs or mutual funds instead of hundreds of individual stocks.

Does owning an S&P 500 index fund mean my portfolio is diversified?

An S&P 500 fund diversifies you across 500 large U.S. companies, but it's still just one asset class. A truly diversified portfolio also includes assets like international stocks, small-cap stocks, and bonds.

What is the difference between asset allocation and diversification?

Asset allocation is your high-level strategy for dividing money between categories like stocks and bonds. Diversification is the practice of spreading investments within each of those categories, such as buying different types of stocks.

Can a portfolio be too diversified?

Yes, owning too many overlapping investments can lead to "diworsification." This adds complexity and fees for average, index-like returns without meaningfully reducing your risk.