Ignoring how your retirement accounts are taxed can lead to a nasty surprise down the road. An unexpected tax bill can significantly reduce your income right when you need it most, undermining decades of diligent saving.

This guide will demystify retirement taxation. We'll break down the core principles, explain how taxes apply at each stage of your savings journey, and compare the most common account types so you can build a more tax-efficient future.

TL;DR: Key Points on Retirement Taxation

- Retirement accounts are taxed in one of two ways: Traditional (pre-tax contributions, taxed on withdrawal) or Roth (post-tax contributions, tax-free withdrawals).

- Growth within these accounts is either tax-deferred (Traditional) or tax-free (Roth), allowing your money to compound more powerfully.

- Withdrawals from Traditional accounts are taxed as ordinary income, while qualified Roth withdrawals are completely tax-free.

- The IRS sets rules like Required Minimum Distributions (RMDs) and early withdrawal penalties to govern how and when you access your funds.

The Two Pillars of Retirement Taxation: Pre-Tax vs. Post-Tax (Roth)

Nearly every retirement account falls into one of two categories based on one fundamental question: do you want to pay taxes now or later? Your answer determines whether you use a Traditional or Roth account.

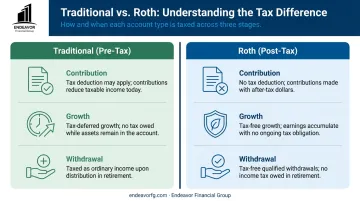

The Traditional (Pre-Tax) Approach

Traditional contributions are made with pre-tax dollars. This means your contribution can lower your taxable income in the year you make it, giving you an immediate tax break.

For example, if you earn $60,000 and contribute $5,000 to a Traditional 401(k), you are only taxed on $55,000 of income for that year. The trade-off for this upfront benefit is that all withdrawals in retirement—both your contributions and the investment earnings—will be taxed as ordinary income.

The Roth (Post-Tax) Approach

In contrast, Roth contributions are made with after-tax dollars, meaning you don't receive an immediate tax deduction.

Using the same scenario, if you earn $60,000 and contribute $5,000 to a Roth 401(k), you are still taxed on the full $60,000. The powerful benefit comes later: all qualified withdrawals in retirement, including decades of investment earnings, are 100% tax-free. This provides valuable tax and planning certainty for your future.

The Three Phases of Retirement Taxation: A Lifecycle View

Taxes don't just affect your money when you retire. They are a factor at three distinct stages: when you contribute, while your money grows, and when you finally withdraw it.

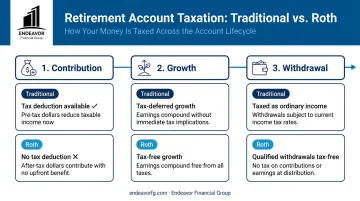

Phase 1: The Contribution Stage

This is where the Traditional vs. Roth choice has its first impact.

- Traditional Contributions: These are often tax-deductible, reducing your current-year tax bill.

- Roth Contributions: These provide no upfront tax deduction.

The IRS also sets annual limits on how much you can contribute. For 2024, the primary contribution limits are:

- 401(k)s, 403(b)s, and most 457 plans: $23,000

- Traditional and Roth IRAs: $7,000

If you're age 50 or over, you can make additional "catch-up" contributions. For 2024, the catch-up amount is $7,500 for 401(k)s and $1,000 for IRAs, according to the IRS.

Phase 2: The Growth Stage

During this stage, compounding growth accelerates your savings, and the tax treatment is critical.

With a Traditional account, your investments experience tax-deferred growth. You don't pay any taxes on dividends, interest, or capital gains as they are earned each year. This allows your entire balance to grow without being reduced by taxes each year.

With a Roth account, your investments experience tax-free growth. Similar to the tax-deferred approach, you don't pay taxes year after year. But the key difference is that this growth will never be taxed, as long as you follow the withdrawal rules.

Phase 3: The Withdrawal Stage

When you retire and start using your savings, the tax consequences of your earlier choices take effect.

Withdrawals and Taxes

Withdrawals from Traditional accounts are taxed as ordinary income. A $50,000 withdrawal is treated the same as $50,000 in salary, which can affect your tax bracket and how much of your Social Security benefits are taxed.

Qualified withdrawals from Roth accounts are completely tax-free. To be qualified, you must typically be at least 59 ½ years old and have had the account open for at least five years.

Required Minimum Distributions (RMDs)

The government doesn't let you keep money in Traditional retirement accounts forever. The IRS requires you to start taking withdrawals, known as RMDs, from accounts like Traditional IRAs and 401(k)s. Based on current IRS rules, you must generally take your first RMD for the year you reach age 73. A key benefit of Roth IRAs is that they are exempt from RMDs for the original owner.

Early Withdrawal Penalties

If you take money out of a retirement account before age 59 ½, you will typically face a 10% penalty on top of the regular income tax. However, the IRS allows for some exceptions, including:

- Total and permanent disability

- A qualified first-time home purchase (from an IRA, up to $10,000)

- Unreimbursed medical expenses exceeding 7.5% of your adjusted gross income

How Major Retirement Accounts Are Taxed: A Comparative Guide

The principles of Traditional and Roth taxation apply across different types of accounts, but each has its own unique rules.

Employer-Sponsored Plans (401(k), 403(b), 457)

These workplace plans are the bedrock of retirement savings for many. Most employers now offer both a Traditional (pre-tax) and a Roth (post-tax) option for employee contributions, letting you choose your preferred tax treatment.

One crucial detail is that any employer matching contributions are always made on a pre-tax basis.

This means that even if you contribute exclusively to a Roth 401(k), the matching funds from your company go into a separate pre-tax account. Those funds will be taxable when you withdraw them in retirement.

Individual Retirement Accounts (IRAs)

IRAs are accounts you open on your own, separate from an employer.

- Traditional IRA: Contributions may be tax-deductible. Your ability to deduct depends on your income and whether you are covered by a retirement plan at work.

- Roth IRA: Contributions are never tax-deductible. Your ability to contribute is also limited by your modified adjusted gross income (MAGI). These income thresholds change annually, so it's important to check the current year's limits with the IRS.

Accounts for Self-Employed and Small Business Owners

If you work for yourself, you have several options, including a SEP IRA or a SIMPLE IRA. These plans generally allow you to contribute much more than a Traditional IRA. They are typically funded with pre-tax contributions and follow the same tax rules as Traditional IRAs for growth and withdrawals.

A Note on State Taxes

Don't forget about state taxes. While this article focuses on federal rules, most states tax retirement income, but the rules vary significantly.

- Some states, like Florida, have no state income tax, so your retirement withdrawals aren't taxed at the state level.

- Others, like California, don't tax Social Security but do tax most other forms of retirement income.

- And some, like New York, offer specific exclusions, allowing eligible retirees to exclude up to $20,000 of pension and annuity income from state taxes.

Strategic Tax Planning to Maximize Your Retirement Income

Understanding the rules is the first step. Applying them strategically is how you build and preserve wealth for the long term.

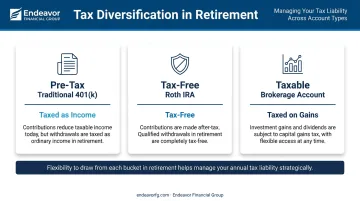

The Power of Tax Diversification

The smartest approach often isn't choosing just one type of account but building tax diversification. This means holding a mix of Traditional (pre-tax), Roth (post-tax), and standard taxable brokerage accounts.

This strategy gives you ultimate flexibility in retirement. In a year where you have high medical bills or other large expenses, you could pull extra funds from your Roth account to cover them without pushing yourself into a higher tax bracket.

Considering a Roth Conversion

A Roth conversion is a strategy where you move funds from a Traditional retirement account to a Roth account. The catch is that you must pay ordinary income tax on the entire converted amount in the year you do it.

A conversion can make sense if you believe your tax rate will be higher in retirement than it is today. By paying the taxes now, you secure tax-free growth and withdrawals for the future.

This can be a powerful tool, especially during a low-income year—for example, in the gap between retiring and starting Social Security.

Building Your Personalized Roadmap

Answering key questions is the first step:

- Should you contribute to a Roth or Traditional 401(k)?

- Does a Roth conversion make sense this year?

- How should you draw down your accounts to minimize taxes in retirement?

The right mix of accounts and strategies depends entirely on your personal situation, including your current and expected future income, your age, and your long-term goals.

Creating a clear, tax-efficient roadmap can be complex, especially for those navigating the transition to retirement or managing the unique tax burdens of a business.

The team at Endeavor Financial Group specializes in comprehensive wealth planning for pre-retirees and business owners. As a fee-only fiduciary, we're committed to providing unbiased advice that helps you navigate these decisions with confidence and build a strategy tailored to your unique financial goals.

Frequently Asked Questions

What is the main difference between a Traditional and a Roth retirement account?

The key difference is when you pay taxes. With a Traditional account, you get a potential tax break on contributions today, but you pay taxes on withdrawals in retirement. With a Roth, you pay taxes today, and your qualified withdrawals in retirement are tax-free.

How is a retirement plan taxed?

It depends entirely on the account type. Traditional plans (like a Traditional 401(k) or IRA) are taxed when you withdraw money in retirement. Roth plans are taxed upfront on your contributions, allowing for tax-free withdrawals later.

When does it make more sense to use a Roth account over a Traditional one?

A Roth is often favored if you expect to be in a higher tax bracket in the future, as you pay taxes now while your income is lower. A Traditional account may be better if you're in your peak earning years and want to lower your taxable income today.

What are Required Minimum Distributions (RMDs)?

RMDs are IRS-required annual withdrawals from pre-tax retirement accounts, like Traditional IRAs and 401(k)s, that must start once you reach age 73. Roth IRAs are exempt from RMDs for the original owner.

What are the penalties for withdrawing money from a retirement account early?

Taking funds out before age 59 ½ usually results in a 10% penalty on top of ordinary income taxes. The IRS does allow exceptions for specific situations, like a disability or a first-time home purchase.

Are Social Security benefits taxable?

Yes, a portion of your benefits may be taxable. The Social Security Administration states that up to 85% of benefits can be taxed if your "combined income" exceeds certain thresholds (e.g., $25,000 for an individual).