In fact, for most entrepreneurs, 80% to 90% of their net worth is tied up in the value of their business, according to the Exit Planning Institute. This makes asset management for you fundamentally different from traditional financial planning. It’s not just about picking stocks; it’s about creating a fortress around what you’ve built while systematically creating wealth outside of it.

This guide covers the complete playbook for business owner asset management, from initial protection and strategic growth to long-term preservation and your ultimate exit.

TL;DR: Asset Management for Business Owners

- Protect First: Use legal structures (like an LLC) and insurance as your first line of defense.

- Separate Everything: Keep business and personal finances strictly separate to maintain liability protection.

- Build Wealth Outside: Systematically move money out of the business into diversified personal investments.

- Plan Your Exit Early: Your exit strategy is the final step in converting business value into liquid wealth.

- Get a Quarterback: A holistic plan requires coordinating legal, tax, and financial strategies.

What is Asset Management for Business Owners (And Why It’s Different)

For business owners, asset management is a strategy to protect, grow, and manage all assets—both business and personal—in an integrated way. It’s not just about managing an investment portfolio; it’s about managing your entire balance sheet.

This approach differs from the financial planning a typical W-2 employee needs, primarily due to three core challenges you face.

The Three Core Challenges

- Concentration Risk: This is the classic "all your eggs in one basket" problem. With most of your wealth tied to your business, your financial well-being depends on its performance. A market downturn, new competitor, or internal crisis could put your entire net worth at risk.

- Intertwined Finances: Business decisions directly impact your personal wealth, and vice-versa. A business loan might require a personal guarantee that puts your home on the line, while a personal event like a divorce can have serious implications for the business.

- Unique Liabilities: As an owner, you're exposed to risks most people aren't, including lawsuits, business debts, and creditor claims. Without proper protective structures, a company legal issue could threaten your personal savings, investments, and property.

While traditional asset management focuses on diversifying liquid investments, your primary goal is different. You must first protect your concentrated, illiquid asset (the business) and then use its success to build diversified wealth outside of it.

Foundational Pillars of Asset Protection

Before you can focus on growth, you have to build a financial fortress. These are the non-negotiable first steps every business owner must take to shield their personal assets from business liabilities.

Choose the Right Business Structure

Your legal entity is your first and most important line of defense. It creates a legal separation between you and your business.

- Sole proprietorships offer no liability protection, meaning your personal assets are at risk if the business is sued, as the U.S. Small Business Administration (SBA) notes.

- LLCs or S-Corporations create a separate legal entity, shielding your personal assets (home, car, savings) from most business debts and lawsuits.

The choice impacts both liability and taxes. A financial advisor can help you coordinate with legal professionals to determine the best fit for your specific situation.

Maintain a Strict Separation of Finances

Forming an LLC isn't enough. You must operate the business as a separate entity. If you co-mingle funds, a court could "pierce the corporate veil," making you personally liable despite having an LLC.

Take these critical steps:

- Open separate business bank accounts and credit cards.

- Keep meticulous accounting records for the business.

- Never use business accounts for personal expenses (like groceries or vacations).

- Pay yourself a formal salary or owner's draw instead of just taking cash from the business.

Leverage Insurance as Your Primary Shield

Insurance is a tool for transferring risk. Instead of bearing the full financial cost of a disaster, you pay a premium to an insurance company to take on that risk for you.

Every business owner should consider these key policies:

- General Liability Insurance: Your frontline defense against claims of bodily injury or property damage.

- Professional Liability (E&O) Insurance: Crucial for service-based businesses, this covers claims of negligence, errors, or malpractice.

- Commercial Umbrella Policy: An inexpensive extra layer of liability protection that kicks in after your other policy limits are exhausted.

Strategic Growth: Building Wealth Beyond Your Business

True financial freedom comes when your lifestyle is no longer 100% dependent on the success of your business. This requires a disciplined strategy for moving capital from the business into personal assets that can grow independently.

Systematically De-Risking Your Personal Balance Sheet

It’s tempting to reinvest every dollar of profit back into the company to fuel growth. While important, it’s also crucial to "pay yourself first" by systematically allocating a percentage of profits to external investments.

The goal is to build a nest egg that can support you and your family, regardless of what happens to the business. This personal portfolio becomes your safety net, your source of liquidity, and your ticket to an eventual work-optional lifestyle.

Supercharge Your Retirement Savings

Business owners have access to powerful retirement plans with high contribution limits, allowing you to build a tax-advantaged asset pool that is completely separate from your business.

- SEP IRA: Lets you make significant, tax-deductible contributions for yourself and your employees. For 2024, you can contribute up to 25% of compensation, not to exceed $69,000.

- Solo 401(k): Ideal for self-employed owners with no employees (besides a spouse). For 2024, contribute as an "employee" (up to $23,000) and "employer," with a combined limit of $69,000 per IRS guidelines.

Using these tools not only builds your personal wealth but also reduces your current taxable income, offering a powerful one-two punch.

Diversifying into Non-Business Assets

Once you are funding your retirement accounts, you can look to other asset classes to build a well-rounded personal portfolio. This could include:

- Publicly traded stocks and bonds

- Real estate (such as a rental property)

- Alternative investments

The specific mix should be tailored to your risk tolerance and time horizon. The principle remains the same: create multiple streams of wealth so your financial security doesn't rise and fall with one company. A financial advisor who specializes in working with business owners can help you design and manage this strategy.

Advanced Strategies for Long-Term Wealth Preservation

For established business owners, the goal shifts from wealth creation to wealth preservation. Advanced strategies are needed to protect your assets, minimize taxes, and ensure a smooth transition to the next generation.

Utilizing Trusts for Enhanced Protection and Control

A trust is a legal arrangement that holds assets on your behalf. Placing personal assets like your home or investment portfolio into an irrevocable trust offers a powerful layer of protection. Since you no longer legally own these assets, they are often shielded from business creditors or lawsuits, effectively separating your personal wealth from company liabilities.

Beyond protecting personal assets, a long-term plan must also address the future of the business itself.

Planning for Business Succession and Estate Continuity

What happens to your business if you suddenly pass away or become disabled? Without a plan, your family could be forced into a fire sale, destroying much of the value you worked so hard to create.

A buy-sell agreement is a legally binding contract that prevents this scenario. It dictates who can buy your share of the business, at what price, and under what conditions.

This proactive planning preserves the business's value and ensures it transfers according to your wishes, providing security for both your family and the company. Navigating trusts and buy-sell agreements involves complex legal and financial decisions, and partnering with a financial advisor ensures these strategies align with your overall wealth management goals.

Planning Your Ultimate Exit: Securing Your Legacy and Wealth

Your exit strategy is the final act of your asset management journey, converting the illiquid value of your business into liquid personal wealth. A successful exit doesn't just happen—it's the result of careful planning that begins years in advance.

Building a Business That's Ready to Sell

Potential buyers look for specific characteristics that make a business valuable and easy to take over. Focusing on these value drivers long before you plan to sell can dramatically increase the final purchase price.

- A strong management team that allows the business to run without your daily involvement.

- Recurring revenue streams that provide predictable and repeatable sales.

- Clean, organized financial records that give buyers a clear and accurate picture of business health.

- A diverse customer base to avoid the risk of relying on one or two major clients.

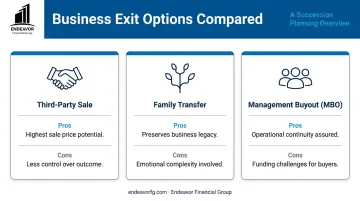

Understanding Your Exit Options

There are several paths to a successful exit, each with different financial and personal implications:

- Selling to a third party: Often yields the highest price but may mean less control over the company's future.

- Transferring to family: A common goal, but one that requires careful planning around fairness, taxes, and leadership transition.

- Management Buyout (MBO): Selling the business to your existing management team can ensure continuity.

Structuring the Deal for Tax-Efficiency

How you sell your business is just as important as the price. The structure of the deal—such as an asset sale versus a stock sale—can have massive tax consequences. An asset sale may result in more of the proceeds being taxed at higher ordinary income rates.

In contrast, a stock sale often leads to more favorable capital gains treatment. Working with experienced financial and tax advisors to structure the deal correctly is essential to maximize your net take-home amount.

The Endeavor Advantage: A Holistic Approach to Your Financial Future

Managing your assets as a business owner is complex. All the pieces—business structure, insurance, retirement savings, succession planning, and tax strategy—are interconnected. Handling them in silos is a recipe for missed opportunities and unnecessary risk.

This is where a comprehensive financial planner serves as your financial quarterback. Instead of you trying to coordinate between your CPA, attorney, and investment manager, a dedicated expert can see the whole field and ensure every part of your financial strategy is working together.

At Endeavor Financial Group, we create a holistic plan that integrates your personal and professional financial life through a structured five-step process:

- We get to know you during an introductory meeting to identify your goals and establish expectations.

- We analyze your situation by conducting a thorough review of your unique business and personal finances.

- We deliver a clear roadmap that addresses everything from succession planning to tax optimization.

- We put the plan into action, coordinating with your other professionals to ensure seamless implementation.

- We provide ongoing support, adapting your plan as your life and business evolve to keep it aligned with your goals.

By coordinating all aspects of your financial life, we help you make clearer, more confident decisions so you can focus on what you do best: running your business.

Frequently Asked Questions

What is business asset management?

It's the integrated strategy for managing and protecting both your company and personal assets. The goal is to grow long-term wealth while shielding it from the unique risks that business owners face.

How do you protect your assets as a business owner?

The foundational steps are forming a separate legal entity (like an LLC or S-Corp), keeping business and personal finances strictly separate, and securing the right types of business insurance.

Is business ownership considered an asset?

Yes, it is often a business owner's largest but most illiquid asset. The primary goal of asset management is to protect its value and eventually convert that value into liquid wealth for retirement.

What is the first step I should take in asset protection?

The absolute first step is to form a separate legal entity for your business, such as an LLC or S-Corporation. This creates a crucial liability shield between your business and personal assets.

How is wealth management different from asset management for a business owner?

Asset management is one piece of the puzzle. Wealth management is the broader strategy for a business owner, combining asset management with financial planning, tax and estate strategy, and exit planning.

Can I use a trust to protect my business assets?

Trusts are excellent for protecting your personal assets (like your home) from business liabilities. The business itself, however, is typically protected by its corporate structure (the LLC or corporation).